Plate

November 9, 2021

SMU Price Ranges & Indices: More Declines for Sheet, Plate

Written by Brett Linton

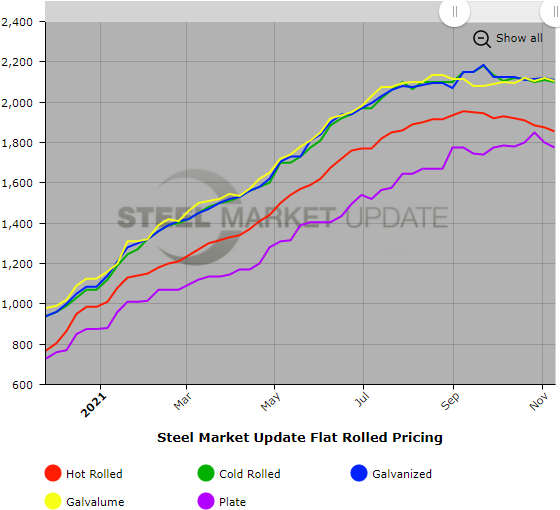

Steel Market Update’s check of the market this week shows both flat rolled and plate prices declining by another $10-25 per ton. The declines were not unexpected and are in line with the downtrend that has materialized in the last two months as seasonal dips in demand and competition from imports put pressure on domestic prices. The benchmark price for hot rolled now averages $1,855 per ton, down $20 in the past week and a $100 decline from the peak of the market in early September. Prices for cold rolled and coated products are down $10-15 per ton, while plate saw a slightly bigger dip at down $25 despite price hikes announced by mills in recent weeks. SMU’s Price Momentum Indicator is pointing Down for hot rolled, but remains Neutral for other products until their trend is more firmly established.

Hot Rolled Coil: SMU price range is $1,775-$1,935 per net ton ($88.75-$96.75/cwt) with an average of $1,855 per ton ($92.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $70 per ton compared to last week, while the upper end increased $30. Our overall average is down $20 per ton from one week ago. Our price momentum on hot rolled steel is Lower, meaning we expect prices to decrease over the next 30 days.

Hot Rolled Lead Times: 5-12 weeks

Cold Rolled Coil: SMU price range is $2,000-$2,200 per net ton ($100.00-$110.00/cwt) with an average of $2,100 per ton ($105.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $45 per ton compared to one week ago, while the upper end increased $25. Our overall average is down $10 per ton from last week. Our price momentum on cold rolled steel will remain Neutral until the market establishes a clear direction.

Cold Rolled Lead Times: 7-13 weeks

Galvanized Coil: SMU price range is $1,970-$2,250 per net ton ($98.50-$112.50/cwt) with an average of $2,110 per ton ($105.50/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $70 per ton compared to last week, while the upper end increased $50. Our overall average is down $10 per ton from one week ago. Our price momentum on galvanized steel will remain Neutral until the market establishes a clear direction.

Galvanized .060” G90 Benchmark: SMU price range is $2,048-$2,328 per ton with an average of $2,188 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-14 weeks

Galvalume Coil: SMU price range is $2,030-$2,180 per net ton ($101.50-$109.00/cwt) with an average of $2,105 per ton ($105.25/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $35 per ton compared to one week ago, while the upper end increased $5. Our overall average is down $15 per ton from last week. Our price momentum on Galvalume steel will remain Neutral until the market establishes a clear direction.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $2,321-$2,471 per ton with an average of $2,396 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 7-12 weeks

Plate: SMU price range is $1,715-$1,835 per net ton ($85.75-$91.75/cwt) with an average of $1,775 per ton ($88.75/cwt) FOB mill. The lower end of our range decreased $15 per ton compared to last week, while the upper end decreased $35. Our overall average is down $25 per ton from one week ago. Our price momentum on plate steel will remain Neutral until the market establishes a clear direction.

Plate Lead Times: 5-9 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.