Long Products

December 2, 2021

CRU: U.S. Long Product Prices Rise Following Big Scrap Price Hike

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Long Products Monitor, Dec. 1

Long product prices again moved higher in the USA m/m following a larger-than-expected scrap price increase and unseasonably strong demand. Mill-announced price increases for wire rod were the largest at $80 /s.ton m/m, while merchant bar and beam prices were also raised by $50 /s.ton. There was another increase of $30 /s.ton for rebar announced, but it was not clear at the time of our publication if it had yet been accepted by the market. Given strong backlogs and general market tightness, it appears upward price momentum for most products will carry into early 2022 before cooling.

![]()

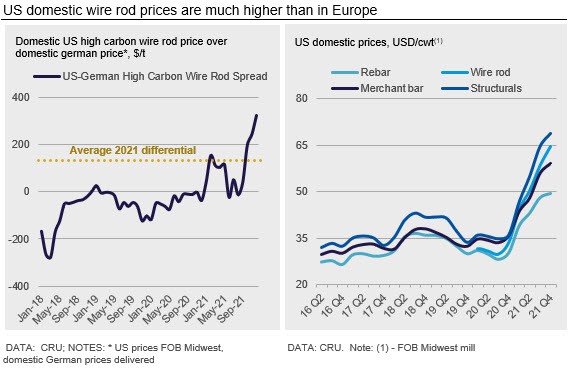

The wire rod market has been tighter than usual as backlogs have prevented a seasonal lull in demand while mill maintenance outages have lasted longer than planned. While not officially being put on allocation, buyers report that mills have been strict on how much material they were willing to offer given the ongoing supply/demand imbalance in the market. At the same time, mill costs rose by more than was expected as scrap price increases in November topped $80 /l.ton or more for certain grades, which prompted wire rod mills to increase prices by roughly this amount to match. According to our market contacts, there has been no real push back on this relatively large price increase.

However, this price increase for wire rod is making imports increasingly more attractive for domestic consumers. For example, the gap between U.S. and German domestic prices is far above average levels even by 2021 standards, and now exceeds $300 /t (see chart). Given the removal of Section 232 tariffs on Europe and better availability, we expect imports to play a bigger role in loosening the U.S. market in early 2022. For now, Census Bureau license data for November show a relatively low import total of ~61,000t, although we do expect that this will be revised higher like in prior months. So far, the majority of the volumes are from Canada and Brazil.

We also expect rebar arrival total license data to be higher than current readings. Totals now show that 77,400t of rebar arrived in November, with Mexico again sending more material than Turkey. Egypt, Algeria, and Spain also sent in notable volumes. For Turkey, a collapse in the lira against the U.S. dollar in late November has made rebar from there more competitive internationally but has also increased raw material costs.

Outlook: Markets to Begin Cooling in Early 2022

As the gap between U.S. domestic and international longs prices expands, we expect to see imports play a bigger role in cooling markets. While raw material costs in the U.S. have risen, and will likely do so again in January, mills will have to contend with supply-chain stabilization and the removal of Section 232 tariffs on European countries (and probably for Japan as well). As such, we believe prices will still face upside price pressure in January before stabilizing and then facing downside price pressures later in the year.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com