Prices

January 21, 2022

Hot Rolled Futures: 2021, a Very Active Year for HR Trading

Written by Jack Marshall

The following article on the hot rolled coil (HRC), scrap and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Hot Rolled

For obvious reasons 2021 was a very active year for HR futures – the runaway rise in prices helped bring the benefit of HR futures into focus.

The COMEX reported almost a doubling of participants trading HR futures from the prior year with open interest reaching an all-time high above $1.4 billion notional at year-end. 2022 will be an interesting follow-up. With a new price trend lower in HR gaining momentum, we will be watching with interest how the futures participants navigate the next 6-12 months.

The market appears to have priced in another $500/ST drop between now and year end as forecasts point to lower global prices for HR, increased imports as tariffs give way to quotas, impending rate hikes by the Fed, moderating demand and additional new domestic supply, political gridlock on spending, and an improving COVID scenario. In short, more supply and less demand – the exact opposite of 2021.

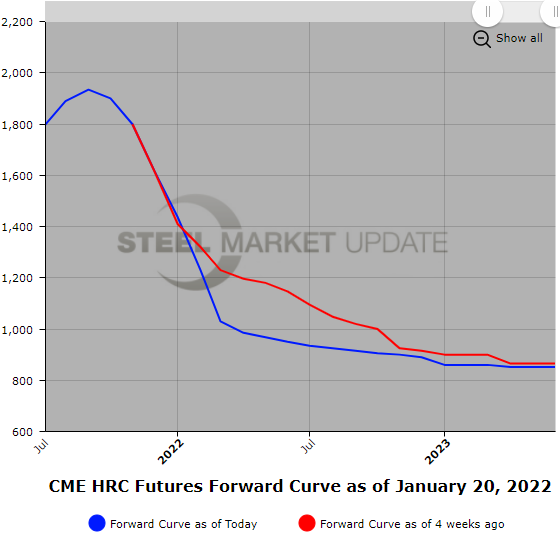

This month the HR futures curve has shifted lower from the end of December as spot HR hovers in the low $1,400/ST range as reflected by a number of the indexes. A straight up look at the change in average prices per quarter since 12/31/21 settlements saw Q1’22 drop from $1,338/ST to just under $1,236/ST, a decline of over $102/ST; Q2’22 drop from just under $1,152/ST to just over $972/ST, a decline of over $179/ST; Q3’22 drop from $985/ST to just under $927/ST, a decline of over $58/ST; and Q4’22 drop from $900/ST to just over $898/ST, a decline of just under $2/ST.

Over this period the Jan versus Dec’22 differential compressed by $12/ST and the Jul’22 through Dec’22 compressed by $85/ST. The nearby futures month had a significant drop while the latter half of the year dropped by roughly $30/ST. The curve for 2H’22 HR also flattened out just above $910/ST.

With regard to current futures prices and the potential for price moves from here, let’s review some historical price points for reference:

- 2018 HR futures average price for the year was $830/ST, the low month settled at $677/ST and the high month settled at $915/ST ($238/ST hilo spread)

- 2019 HR futures average price for the year was $601/ST, the low month settled at $493/ST and the high month settled at $714/ST ($221/ST hilo spread)

- 2020 HR futures average price for the year was $606/ST, the low month settled at $451/ST and the high month settled at $1,057/ST ( $606/ST hilo spread)

- 2021 HR futures average price for the year was $1627/ST, the low month settled at $1,162/ST and the high month settled at $1,934/ST ( $772/ST hilo spread)

The change in the settlement price from Nov’21 to Dec’21 was a drop of $183/ST, almost as wide as the 2019 hilo spread. There is a lot of potential implied volatility when you consider that the 10-year average HR price was about $630/ST as compared to a 2021 HR average price of $1,627/ST. The question is, how long will this market take to return to the mean?

Trading/hedging with HR futures has been growing steadily, especially in light of the increased volatility. December HR trading volumes were close to 20,000 contracts or almost 400,000 ST per side. January is likely to match or exceed that volume.

Below is a graph showing the history of the CME Group hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

Editor’s note: Want to learn more about steel futures? Registration is still open for SMU’s Introduction to Steel Hedging: Managing Price Risk Workshop to be held Feb. 14-15. You can get more information by clicking here.

Scrap

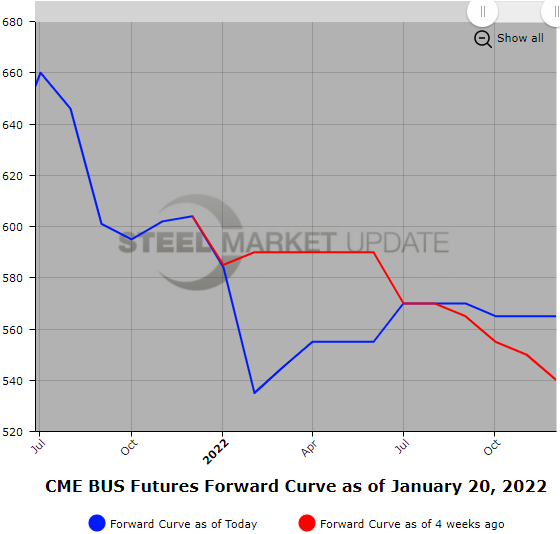

January BUS settlement just above $540/GT was a surprise development as numerous sources were anticipating only a $20/GT drop initially from the Dec’21 $604/GT level. Already over 62,000 GT of BUS futures have traded in January, a nice volume pickup from December. The BUS futures curve has declined roughly $40/GT ($582/GT to $542/GT) on an average weighted basis in the Q1’22 quarter, and $30/GT ($585/GT to $555/GT) in the Q2’22 quarter since the Dec. 31 settlement. The latter half of 2022 is flat to rising slightly. Soft to nonexistent offshore 80/20 demand has helped to keep the shred alternative supplies relatively healthy. Concern that automotive and construction sector inventories have been reported to be growing likely saw mill demand abate somewhat. COVID still seems to be gumming up some producer/manufacturing supply-demand equilibriums. Recent nearby futures activity suggests February might also be soft.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here.