Overseas

February 11, 2022

CRU: Global Sheet Prices Dragged Down by Collapse in U.S. Market

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor, Feb. 9

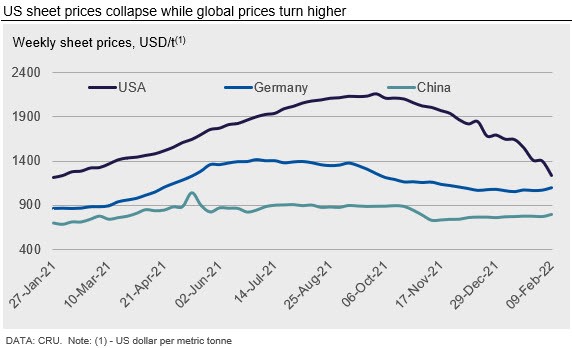

The global sheet market often exhibits price trends that vary by region. Occasionally, prices do move in the same direction, though on these occasions, prices typically reflect a unified trend of global costs or inventory change.

In the current sheet market, key steelmaking raw material costs have increased, namely iron ore and coking coal. Each of these received a boost after the end of China’s Spring Festival and each are well above their 52-week low.

Stronger costs have provided some support to global sheet prices, primarily in the Asian markets. India has been a prime example of this trend, where higher raw materials prices, rather than demand, led to a mill price increase. Indian mills have been successful at realizing higher prices for exports and due to this, domestic prices have followed. In Southeast Asia, sheet prices have also increased though demand has been limited. These gains came about due to low inventories, rising costs and expectations of higher demand.

In Europe, mill increases alongside some production outages and an unplanned BF outage at SSAB have sufficiently tightened the market enough for monthly prices to rise for the first time since July 2021.

However, not all sheet prices increased from our Jan. 12 price assessment. In the North American market, sheet prices have continued to collapse from highs reached in 2021 H2. Today, HR coil in the U.S. market has fallen by $835 /s.ton since the peak less than five months ago. While this price fall is larger than the full peak to trough decline of 2008-09, HR coil prices today continue to remain at a wide premium over both costs as well as global prices.

Overall, this decline in North America overwhelmed increases elsewhere and drove CRU’s Global Flat Products Steel Price Indicator (CRUspi flats) down by 4.5% m/m. The CRUspi flats is now down to its lowest level since March 2021.

USA Continues to Ease Section 232 Tariffs

Earlier this week, the USA alongside Japan announced an agreement to eliminate the S232 tariffs on steel. The agreement allows up to 1.25 Mt/y of steel imports from Japan without the 25% tariff. In addition to this, there is approximately 0.55 Mt of imports that are allowed in due to an approved exclusion. Sheet imports to the USA are less needed in today’s market due to rising domestic capacity. However, this agreement will re-establish trade partnerships and help steel consumers to realize more competitive prices.

Outlook: Costs, Covid-19, and China to Determine Near-Term View

Our near-term view is heavily dependent on the three C’s: Costs, Covid-19 and China. Outside North America, sheet prices have found support from the rebound of iron ore and the record high cost of coking coal. We expect that Chinese steel production and demand have peaked and as such, these costs probably have room to fall. But until they do, sheet prices may find further support. Covid-19 remains a constraint, especially as the latest variant has slowed economic, industrial and logistic activity due to a temporary absence of workers. Lastly, we are closely watching China and its return from holiday. We expect demand from the construction sector will slow and demand from manufacturing has been limited due to component shortages and supply chain disruptions, but any variance to this can support sheet prices.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com