Plate

May 12, 2022

March Import Share of US Sheet and Plate Markets

Written by David Schollaert

Imports of less expensive sheet and plate products continue to arrive at US ports, and at a faster pace in March. Following lighter volumes in February, overall flat product imports accelerated in March and took a larger share of the domestic steel market, according to Commerce Department data.

Imports’ share of US sheet and plate markets peaked in December, reaching their highest levels in the past 4.5 years. The trend was driven by the need for buyers to find relief from inflated steel prices in the US. As the market slowed at year-end, so did imports. That trend reversed in March.

Imports’ share of total sheet shipments into the US was 18.6% in March, up from 14.6% month-on-month (MoM) but below a peak of 19.5% in January. Though domestic shipments were up 5%, the increase was driven by a 41.1% surge in foreign sheet. The market share of plate product imports also rose in March to 22.5% from 20.3% the month prior.

March’s sheet imports totaled 954,134 tons, up from the 676,425 tons in February, and one of the highest totals over the past 12 months.

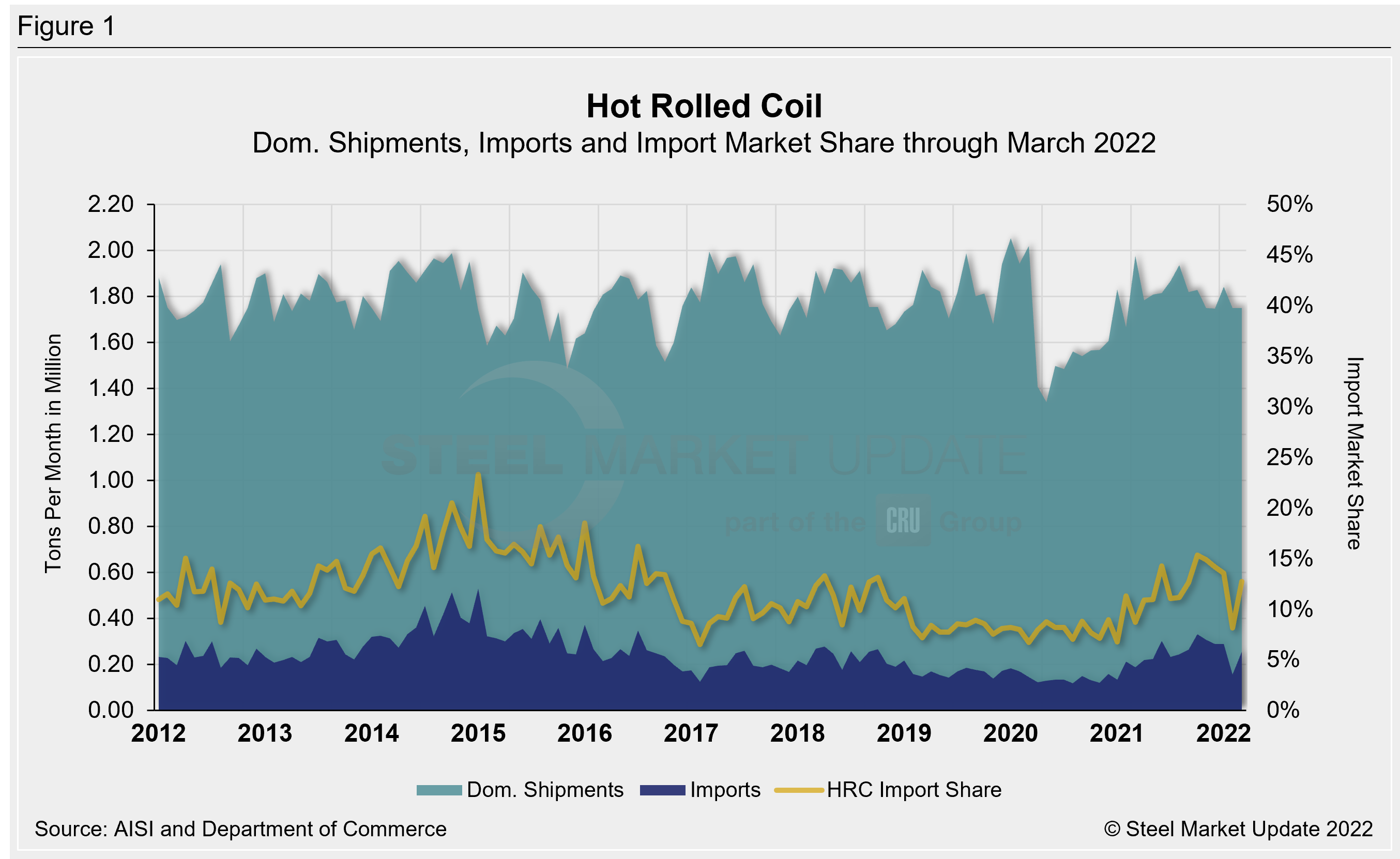

Overall sheet product shipments (domestic shipments plus imports) were up 10.2% in March versus February. They totaled 5.123 million tons, and that higher figure was driven by a 277,710-ton increase in foreign shipments. Hot-rolled coil (HRC) imports totaled 255,430 tons in March, up a whopping 65.4% versus the month prior. The details are below in Figure 1.

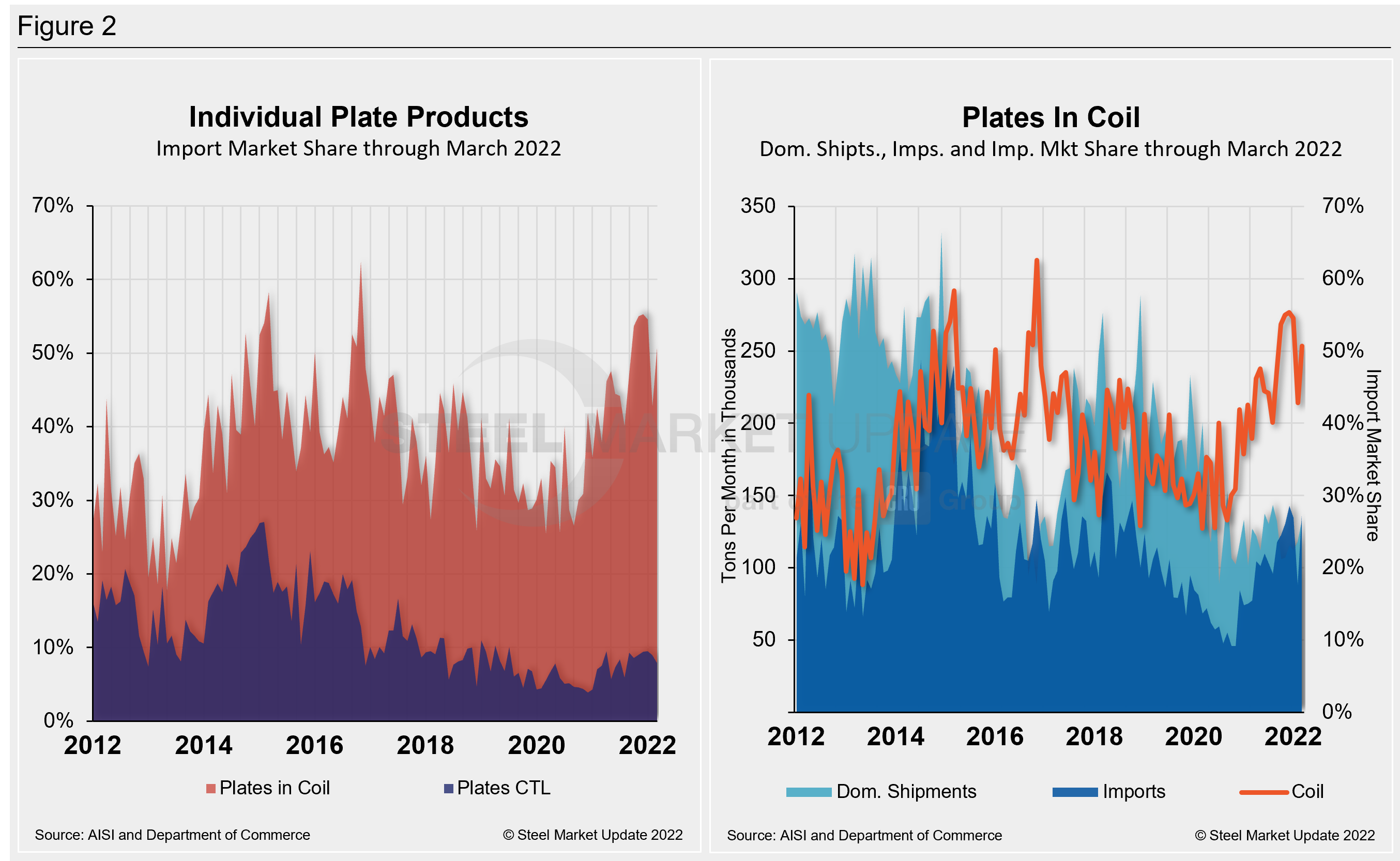

Plate products in March saw an overall increase in shipments as apparent supply grew by 28.1% MoM. The gain was driven by an increase of 42% in imports and a 24.5% rise in domestic plate shipments. March plate imports of 176,890 tons were the second-highest total in more than a year. Foreign supply rebounded after almost falling to its lowest pandemic-era mark the month prior. All told, total plate shipments, including foreign and domestic, were 784,536 tons in March, up from 612,655 tons the month prior and the highest sum in nearly a year.

The import share of HRC rose 4.6 percentage points to 12.7% in March, a strong recovery after seeing its lowest mark in nearly a year in February. The increase in share was driven by a 65.4% gain in foreign material, while domestic shipments were largely unchanged MoM. HRC apparent supply totaled 2.005 million tons in March, up from 1.904 million tons the month prior.

Imports of cold-rolled coil (CRC), galvanized (hot dipped and electrolytic), and other metallic coat (OMC) were all up in March. Galvanized saw the biggest increase, up 37.1% MoM, followed by CRC (+29.4%), and OMC (+28.6%).

The import market share for plates in coil grew to 50.7% in March, a 7.9 percentage point increase MoM. The increase was driven by a 54.1% increase in total imports in March, while domestic shipments rose 12.1% over the same period. Total imports of plates in coil were 136,365 tons in March, up from February’s 88,468 tons.

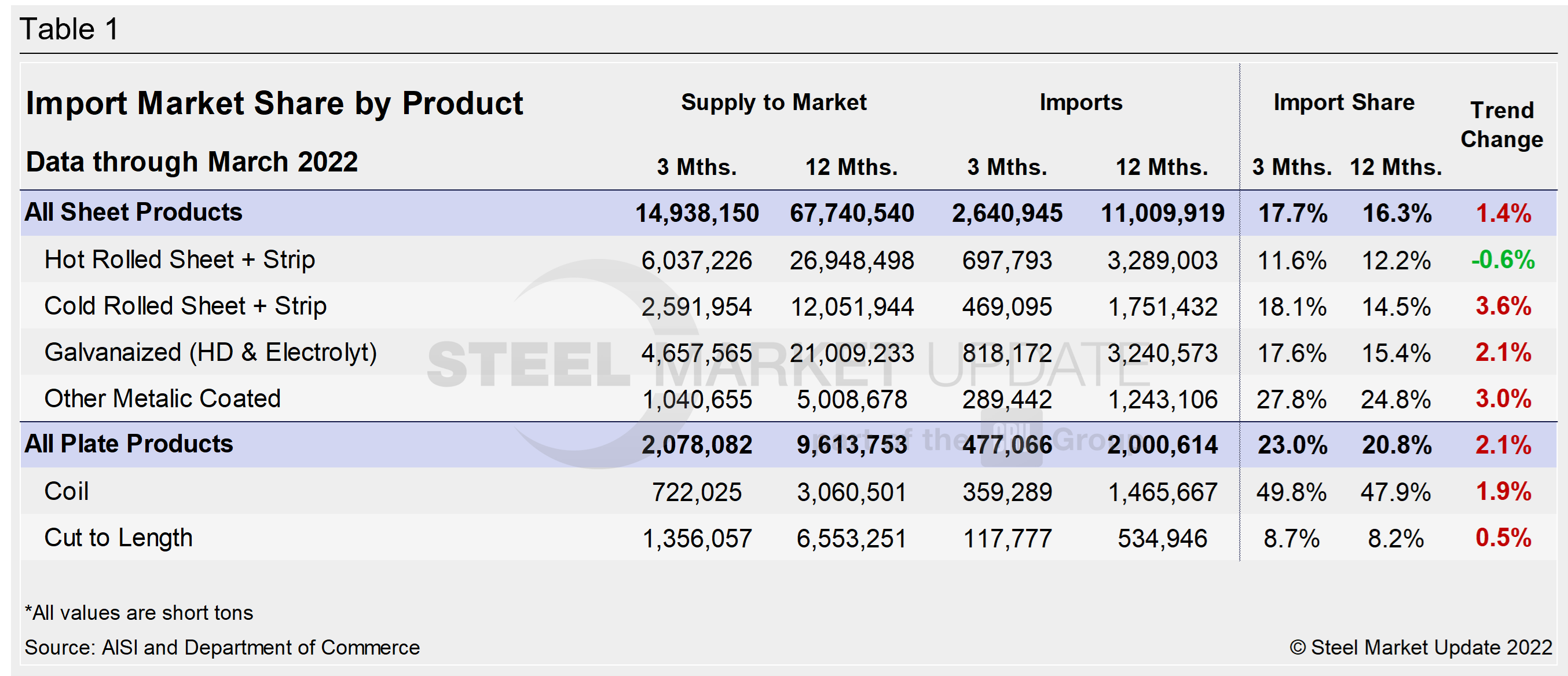

The table below displays the total supply to the market in three months and 12 months through March 2022 for sheet and plate products and six subcategories. Supply to the market is the total of domestic mill shipments plus imports. It shows imports on the same three- and 12-month basis and then calculates import market share for the two time periods for six products. Finally, it subtracts the 12-month share from the three-month share and color codes the resulting green or red according to gains or losses. If the result is positive, it means that the import share is increasing, and the code is red.

The big picture is that imports’ share of US sheet and plate sales recovered from a low February. The big second-half jump in total imports was the result of historically and disproportionately high domestic steel prices. The influx of foreign material had been declining, coinciding with lower domestic prices. The war in Ukraine shifted that dynamic. It is too soon to know whether higher import levels will continue, especially as the global market shifts its raw material sourcing due to sanctions in some jurisdictions on Russian material.

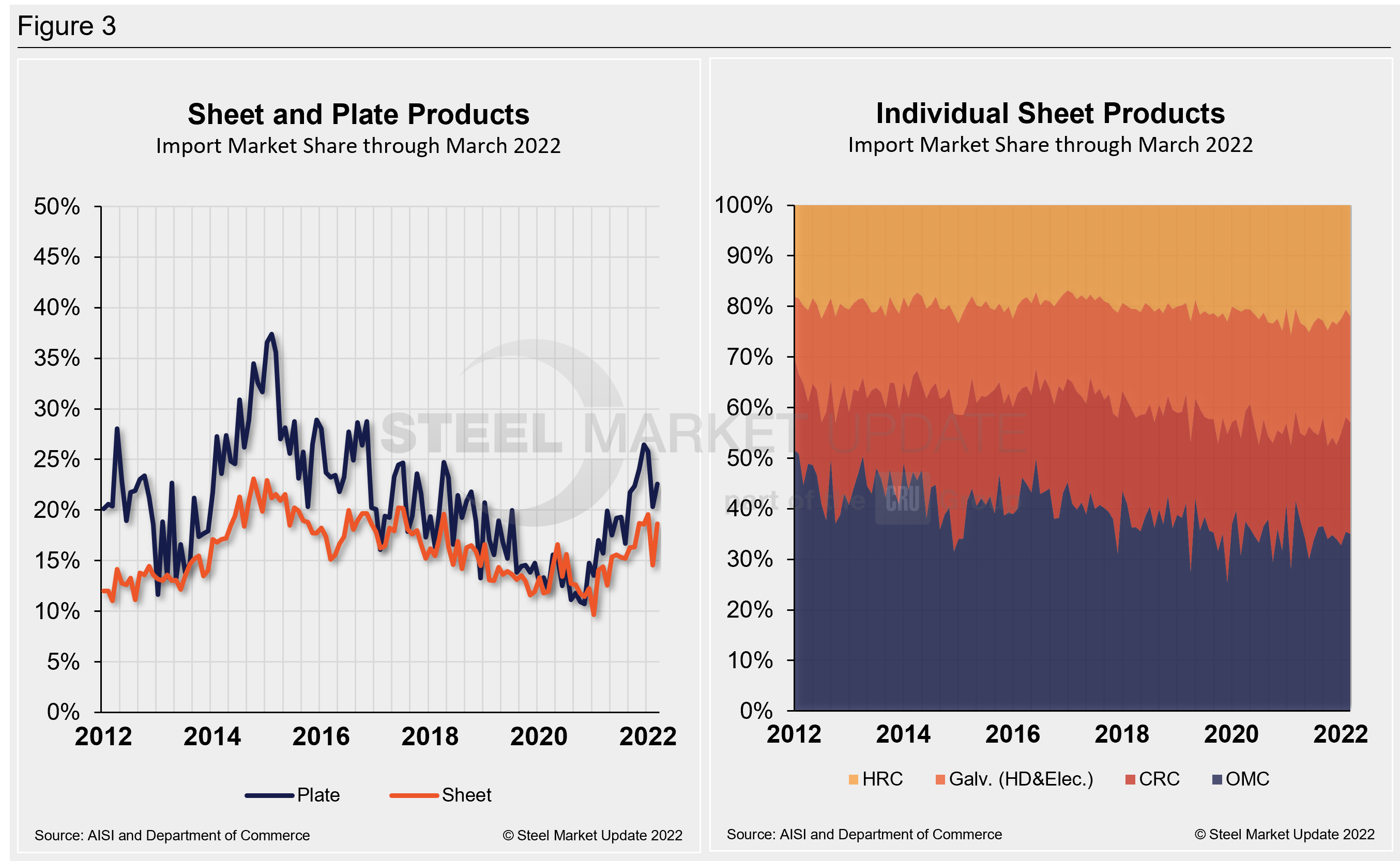

Hot-rolled and cold-rolled sheet and strip have seen a trend shift along with plate products, illustrating how import competition is impacting domestic products in three months compared to 12 months. The most notable of those subcategories is HRC, which saw a declining import market share through February.

The import market share of individual plate products as well as a breakdown of the market share for plates in coil are displayed together in Figure 2. The historical import market share of plate and sheet products, and the import market share of the four major sheet products, are shown side-by-side in Figure 3.

By David Schollaert, David@SteelMarketUpdate.com