Analysis

August 7, 2022

Final Thoughts

Written by Michael Cowden

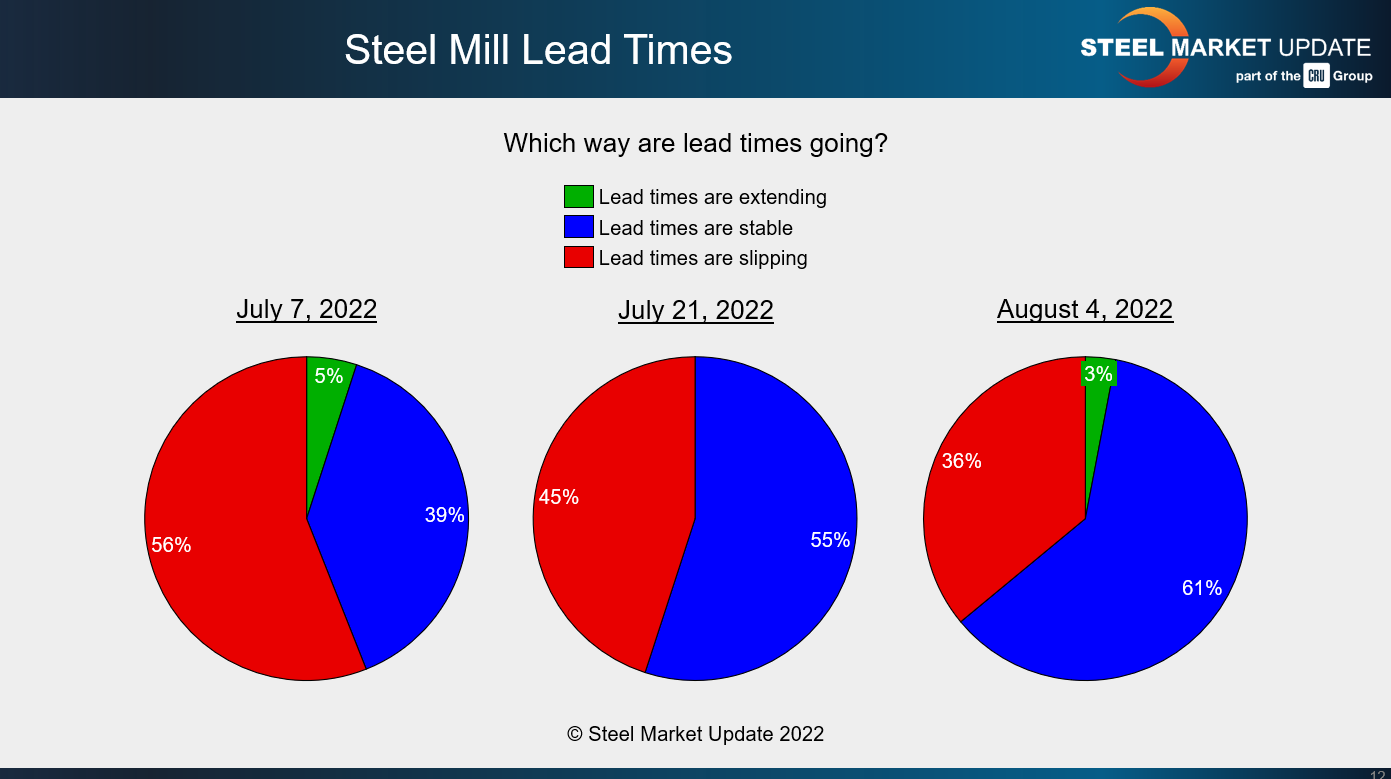

I mentioned in my last Final Thoughts that I’d been surprised to see hot-rolled coil lead times inch up, even if only modestly so. I cautioned at the time not to make too much of just one data point or to call a trend based on just one survey.

That big caveat aside, as we compiled full survey results, I was surprised to see more data points pointing toward potentially better days ahead. Don’t get me wrong. The results are by no means bullish. But they’re less bearish than in prior weeks.

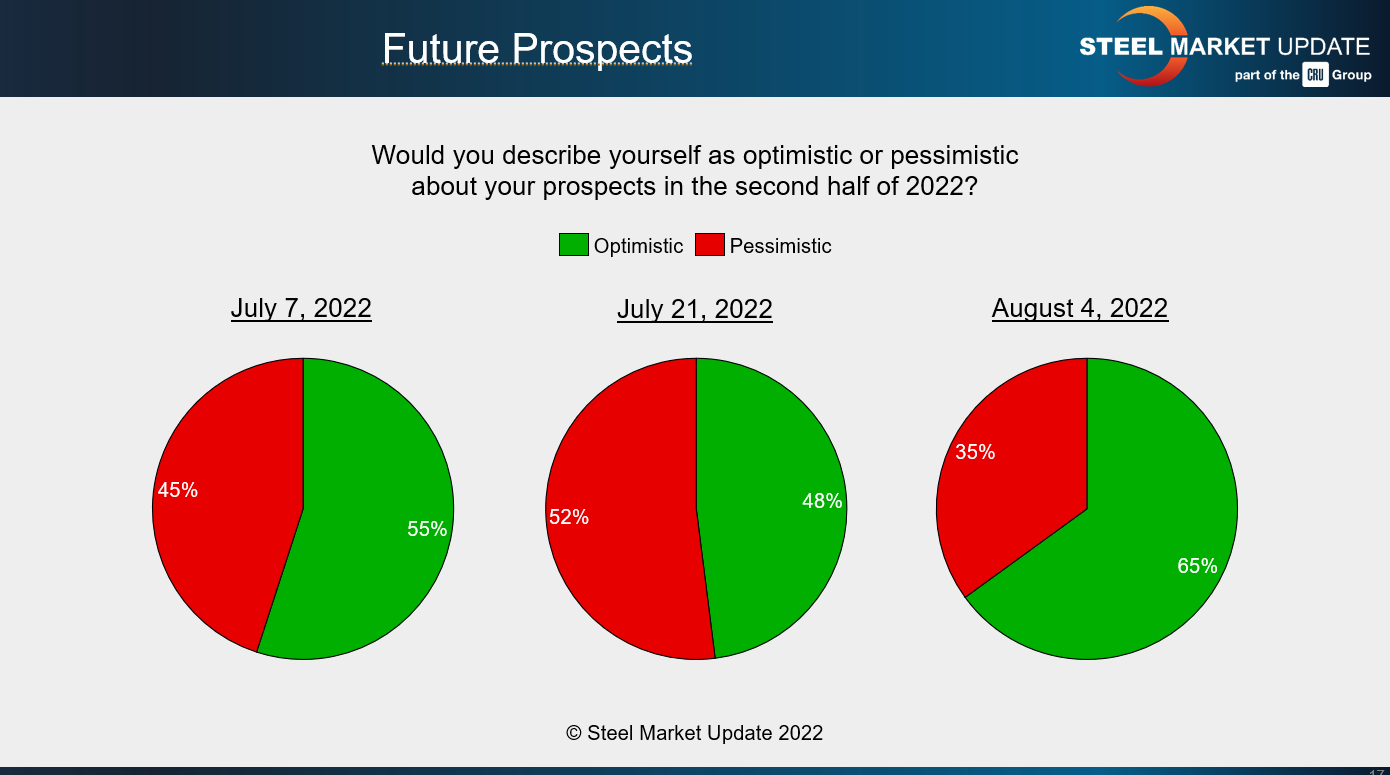

Here are just a few examples. For starters, more people are optimistic about the second half than was the case a just a few weeks ago.

And while almost all survey respondents report that mills are willing to negotiate lower sheet prices, more are reporting that lead times are stable – another big change over just the last month.

It’s possible the result above is simply a reflection of the fact that lead times can’t physically get a lot shorter than they are now.

That said, I think it’s worth framing the feedback on lead times in the broader context not just of sentiment but also of demand:

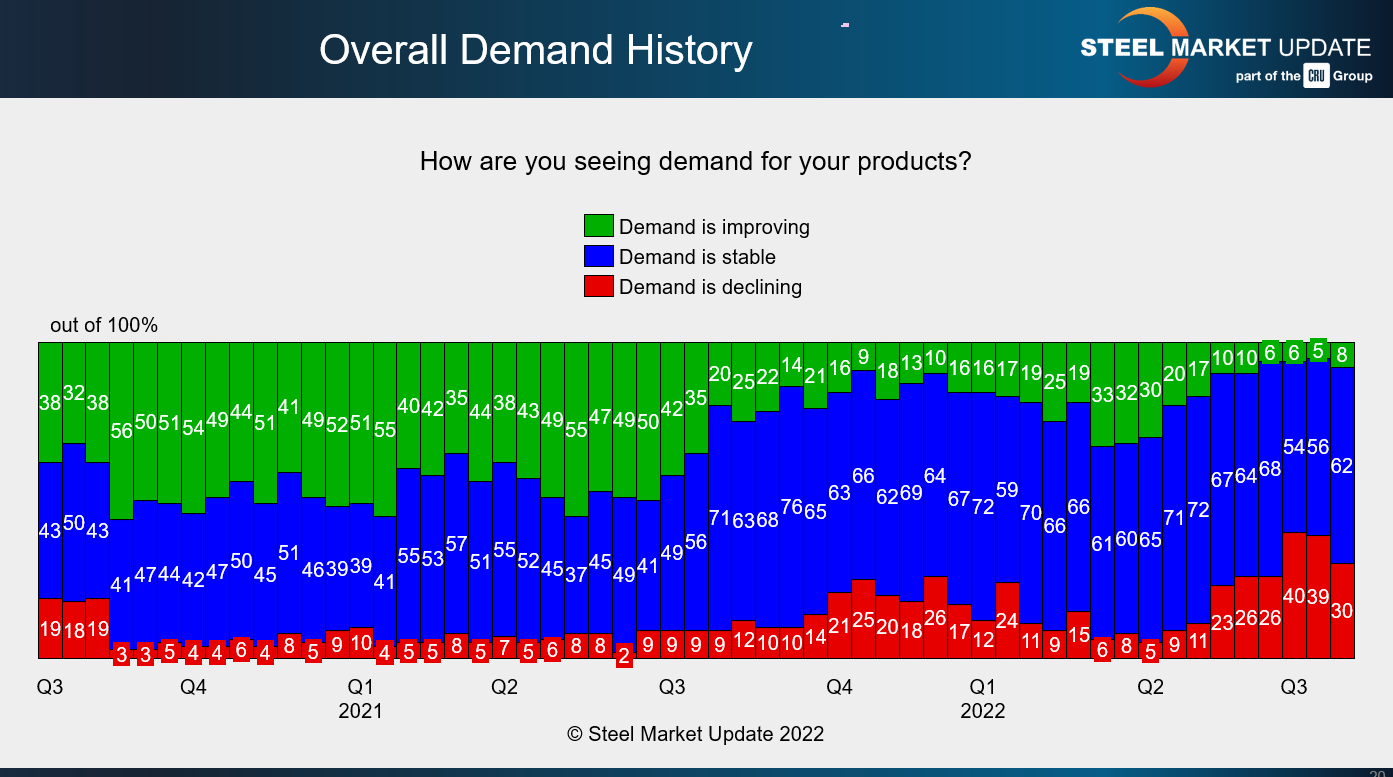

Approximately 30% of respondents reporting declining demand. That is by no means a good thing. But it is a better reading than we saw over the prior two surveys – when we were seeing the highest number of people reporting declining demand since the early days of the pandemic.

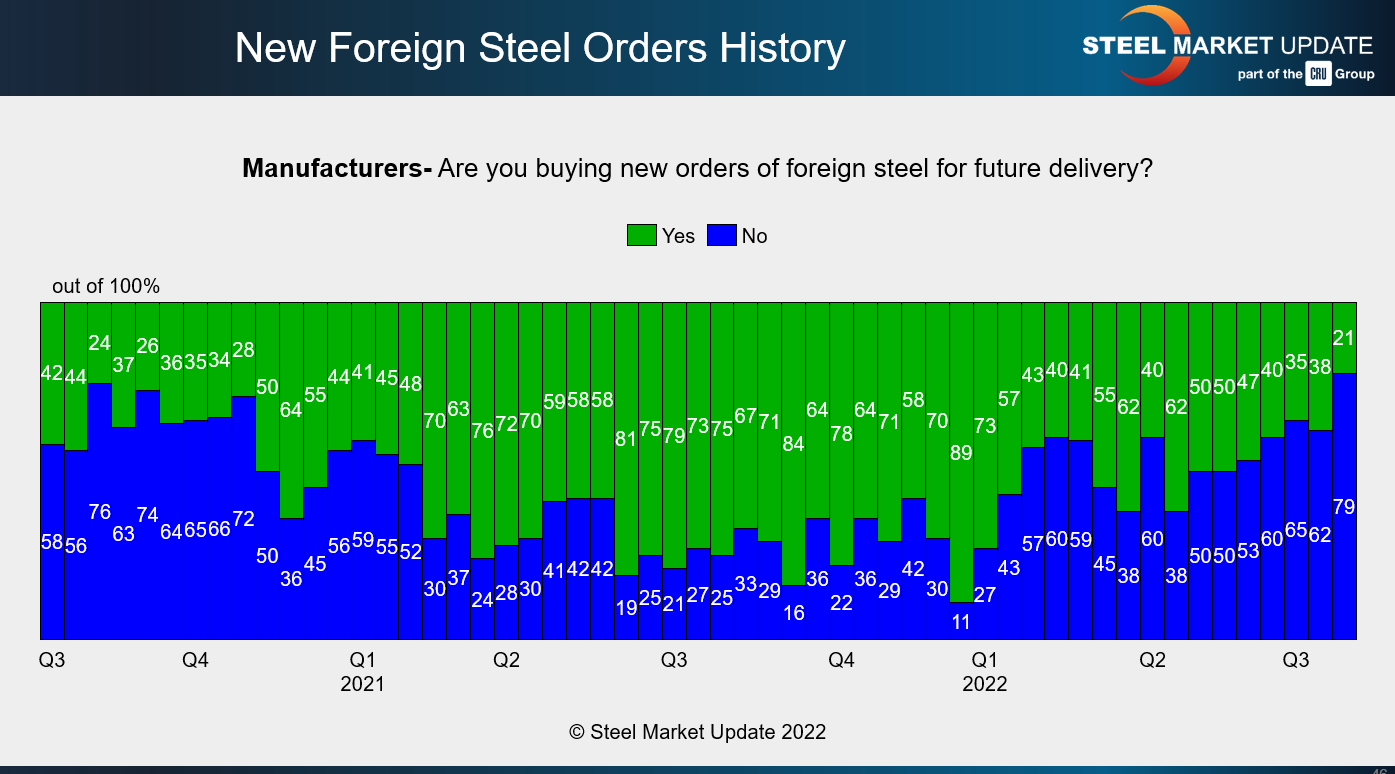

Another notable trend is that fewer manufacturers are buying imports.

Only 21% of manufacturer respondents said were buying imports in our last survey, the lowest reading we’ve seen since at least Q3 2020.

That shouldn’t come as a surprise to those of you who have been following our coverage of the rapidly declining spread between US prices and the landed price of imports.

Good news, right?

Perhaps. But imports are sometimes mistakenly associated with bad times for steel. Look back to last year: imports were running high even as US prices were hitting their highest levels ever.

In short, steel imports can be a sign of strong industrial activity. And the lack of them – following the outbreak of the pandemic, for example – can be a sign of poor demand.

And make no mistake, it’s not all roses. Some of the cross currents in of our data are hard to fit into a consistent narrative.

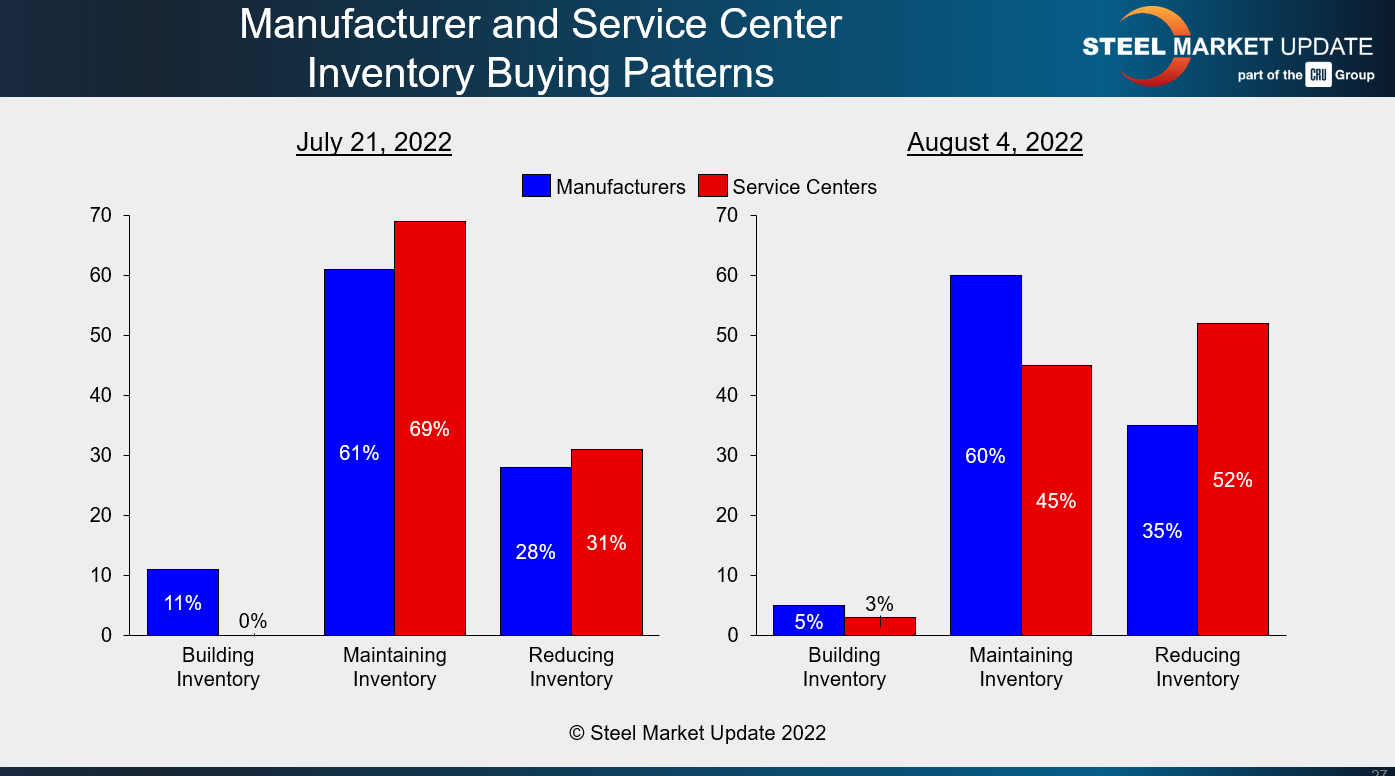

More respondents are reporting stable demand. And yet more also report that they are reducing inventories. Does that mean demand is stable at lower levels?

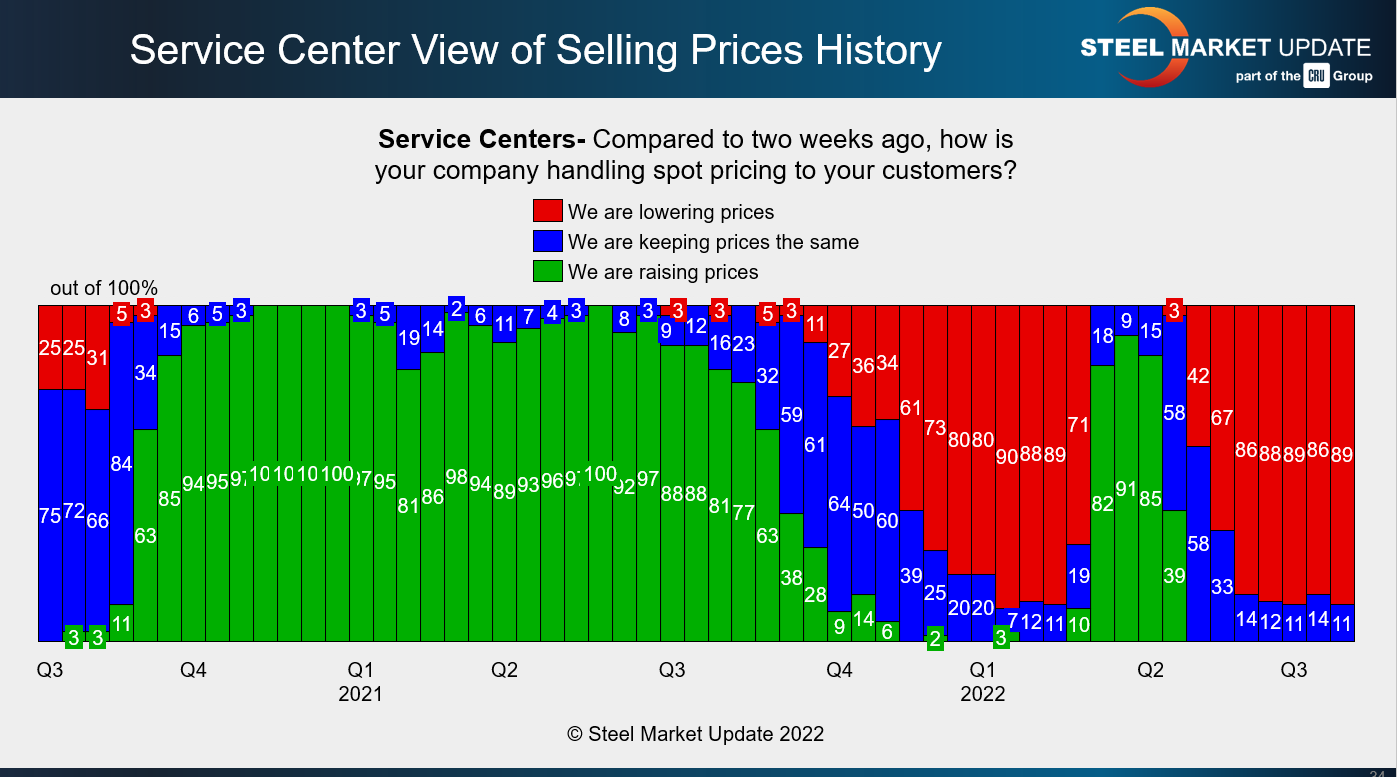

Also, nearly all service centers continue to lower spot prices to their customers, which might run contrary to the narrative at the mill level that prices are at or near a bottom.

So what do you think. Are buyers running inventories low amid stable demand, which means we could see the market snap back up on any sort of disruption – labor-related or otherwise? Or is this just a “dead cat bounce,” a modest uptick as lead times get into the seasonally busier fall months?

PS – Don’t just read our survey data. Make sure your company’s experience is reflected in it. Contact Brett Linton at Brett@SteelMarketUpdate.com to become a data provider. (Contrary to what you might have heard, our surveys only take a few minutes to complete.)

By Michael Cowden, Michael@SteelMarketUpdate.com