Prices

February 23, 2023

HRC Futures Rocket Higher on Record-Setting Volume

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

Apparently, the cat is out of the bag in regards to the sneaky tight fundamentals. How many times have you said or heard someone say “this is crazy” this week? This is not crazy; this is hot-rolled steel! However, it is intense. Here where today’s CME Midwest HRC and busheling markets stood at 2:00 pm CST!

Trading of HRC futures is now considered to be an extreme sport. Don’t be surprised if Red Bull starts advertising in Steel Market Update. So what is going on? Is this another short squeeze? Did the vampire squids wake up? How much further can this go? All I can say is keep an open mind about prices. January’s flat-rolled data (shipments, inventory, etc.) recently released showed little has changed with respect to the stats. That is, this market is among the tighter markets seen over the past decade. If some kind of unplanned outage occurs to boot, then watch out!

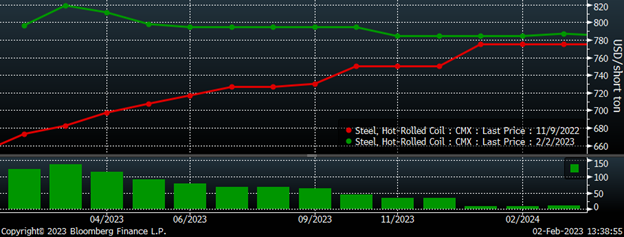

My last article written on Groundhog Day discussed how the HRC futures curve had shifted from contango (upward sloping) to a flat curve over the course of almost three months.

CME Hot Rolled Coil Futures Curve $/st

From Ernest Hemingway’s The Sun Also Rises:

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

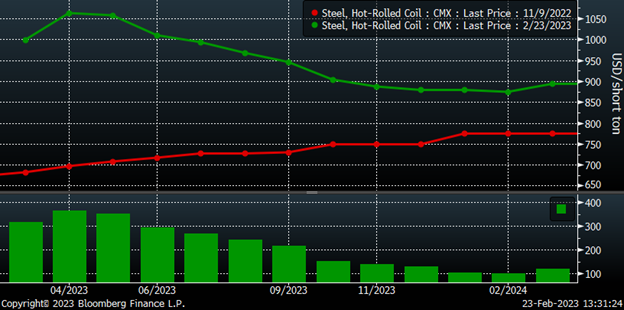

From Nov. 9 through Feb. 2, the April HRC future gained $118. Over the past three weeks, the April future has gained another $248, with $158 of the $248 gain in the past three trading sessions. The months of March, April, and May have gained between $300-350 off their respective bottoms.

CME Hot Rolled Coil Futures Curve $/st

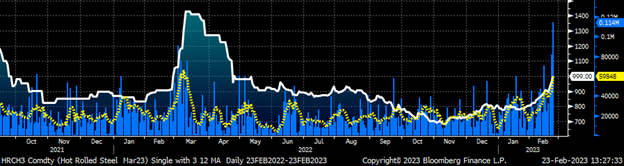

What’s more, the rally has been on record-setting volume, with over 125k tons traded today. That is a new all-time record, beating last year’s record of 91k tons set on March 3. With yesterday’s volume of 82k tons, the HRC futures market saw its first ever two-day volume exceeding 200k tons.

March CME HRC Future $/st w/ Aggregate Curve Volume & 5-Day Avg.

The rally in HRC futures has pulled the busheling futures into the fray as well with busheling futures quickly lifting off toward $600. As shown above, busheling futures are also in rally mode with the May and June futures trading up to a new recent high of $570 today.

CME Busheling Futures Curve $/lt

Is this a short squeeze? Are some market participants getting liquidated? Or is this simply the tail wagging the dog? That is that the physical market tightness is real and about to get even tighter. With physical availability starting to come into play, watch lead times closely. If lead times get extended, watch for some buyers to be put in a position where they could run out of material. But how could this be happening—again?

The broadly accepted assumption in the residential mortgage-backed securities market (RMBS) in the mid-2000s was that home prices in different cities, states, regions, etc. weren’t correlated. With the realization that this assumption was incorrect, the banks housing the bulk of the RMBS market had to collectively and simultaneously deleverage their holdings. With everyone trying to sell at once, the market became totally imbalanced and crashed. This led to the collapse of Bear Stearns, Lehman Brothers and, eventually, the global financial crisis. I bring this up as an analogy to help explain what could be currently happening in steel.

Consider the destocking and weak demand for flat rolled seen in the back half of last year, fears of an imminent economic recession and, most of all, increase in domestic flat-rolled production capacity that had come on in 2022 and continues to ramp up in 2023. Did these factors lead to a broadly accepted assumption that steel would be readily available in the spot market in 2023? If so, did that lead to a material reduction in contract tons for 2023 and a general supply chain strategy of holding low levels of inventory expecting steel to be readily available for purchase in the spot market?

If the answer is yes to those two questions, is what we are witnessing the collective realization that those assumptions were flawed? Is this the stampede of buyers moving away from that flawed buying strategy toward one with much longer lead times, and where spot availability is tight? I need to know the answer to this! I need to know if this rally is going to be like the extended rally of 2021 or the breakneck, but short-lived, rally of 2022. For if I knew that, then I could manage accordingly. I’m trying to pitch a perfect game here and we’re still in the early innings, so if you have the answer, please call me immediately. If not, then keep that chinstrap buckled.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

By David Feldstein, Rock Trading Advisors