Prices

August 8, 2024

HR futures: Forward premiums remain substantial. Are they substantial enough?

Written by Spencer Johnson

Another month for hot-rolled (HR) coil, and another disappointing one for the bulls. They are still holding onto hope that the bottom is here and still pointing to an imminent uptick in HR prices.

As the saying goes, even a broken clock is right twice a day. So the truth is that if the market kept pricing in a premium long enough, eventually it would be right – and we would indeed see a spot price uptick. So far however, the upside momentum has been extremely muted.

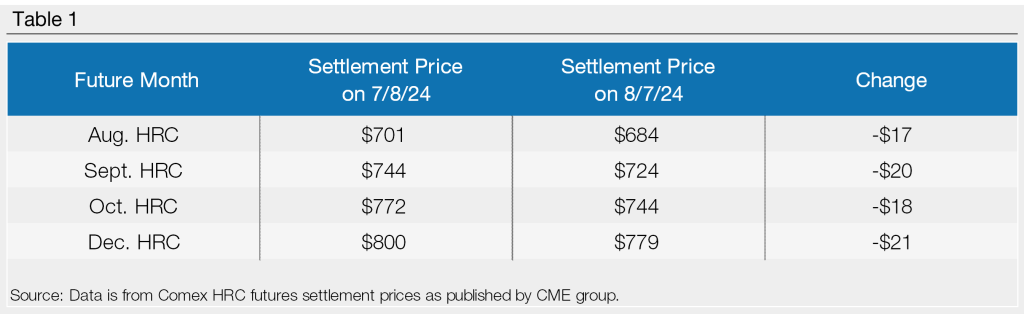

It’s been more of a stop to the bleeding rather than a reversal for now on the index. But since our last report, weakness in futures is pretty modest. Month over month it looks like this:

While we had hit lower lows than the above in the interim (October actually got as low as $723/ton on July 23rd), it has hardly been a brutal rout of the bulls here. Spot prices are down about the same amount as the futures above. And while this is usually a momentum market, we still see September and beyond pricing in nearly a $100/ton premium to most spot offers available (or more depending on the particulars). This in turn prompts a lot of questions yet again about how much premium needs to be baked into the forward price in order to get physical inventory holders to sell futures.

All eyes on interest rates

The answer is more art than science, and there are a number of obvious moving pieces (liquidity, access to credit and cost of credit, storage costs, etc.). Some of them can vary substantially from one entity to the next. But we still think the relevance of interest rates here is high. An imminent rate cut would likely be positive for underlying fundamentals. It would also the ease the financing costs and make a higher premium less necessary for carry traders.

Little has changed in those carries as the number is in line with where it was a month ago. The market is paying about $150/ton to hold HR until December. As far as how attractive that level has been to sellers, naturally the interest varies. But the relatively low exchange volumes might be implying that the number of “risk off” pessimists carrying inventory in HRC is not a tremendously high number – or we might expect to see more volume at these levels. Certainly, the continued optimism about trade protectionism, especially in an election year, is a factor.

Higher interest rates are a factor. And yet it’s hard to shake the feeling that part of the contango in this market is simply based on the assumption that we do not have a lot of downside room here in the spot price unless there is significant economic contraction imminent.

Disclaimer

This material should be construed as the solicitation of an account, order, and/or services provided by the FCM Division of StoneX Financial Inc. (“SFI”) (NFA ID: 0476094) or StoneX Markets LLC (“SXM”) (NFA ID: 0449652) and represents the opinions and viewpoints of the individual authors or presenters. It does not constitute an individualized recommendation or take into account the particular trading objectives, financial situations, or needs of individual customers. Additionally, this material should not be construed as research material. The trading of derivatives such as futures, options, and over-the-counter (OTC) products or “swaps” may not be suitable for all investors. Derivatives trading involves substantial risk of loss, and you should fully understand the risks prior to trading. Past results are not necessarily indicative of future results.

All references to and discussion of OTC products or swaps are made solely on behalf of SXM. All references to futures and options on futures trading are made solely on behalf of SFI. SXM products are intended to be traded only by individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM.

SFI and SXM are not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Contact designated personnel from SFI or SXM for specific trading advice to meet your trading preferences.

Reproduction or use in any format without authorization is forbidden. Copyright 2024. All rights reserved.