Analysis

May 14, 2023

Final Thoughts

Written by Michael Cowden

The drop in sheet prices we’ve seen at the mill level is now spreading downstream – an abrupt shift from just a few weeks ago, according to our latest survey data.

More and more service centers are cutting prices. I had expected to see an increase in the number of service centers reporting that they were lowering prices. I did not expect to see such a big jump so suddenly.

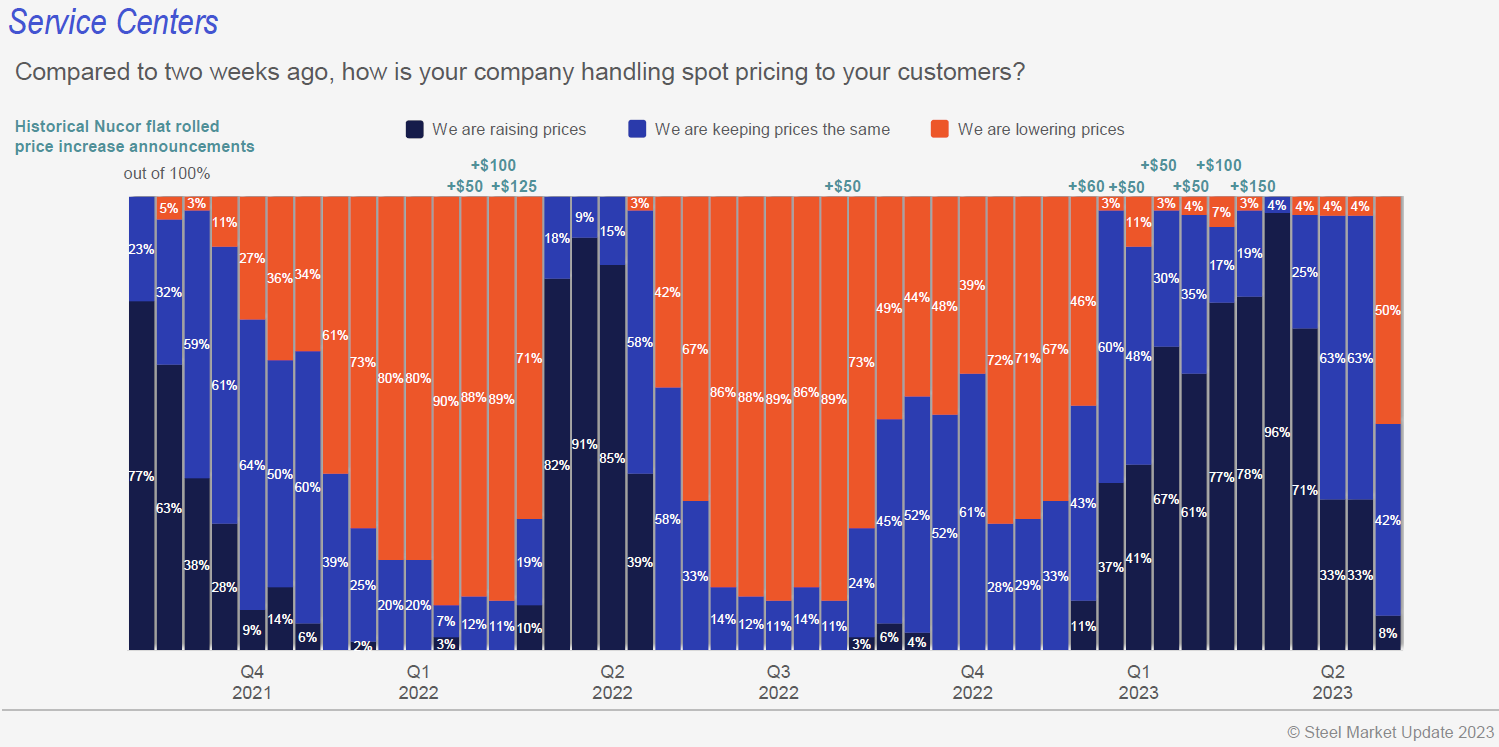

Check out the slide below:

Only 4% of service center respondents to our survey at the end of April said that they were lowering prices. The number has since skyrocketed to 50%.

Some context: We saw that number rise slowly in late 2021 as supply caught up in demand and then overshot it. What’s happening now more closely resembles what we saw after Russia’s invasion of Ukraine last year. A spike in service centers raising prices was followed by an equally sharp decline once the initial shock of the invasion passed.

The drivers are different this time. Prices surged in Q1’23 when expectations of an economic slowdown and a sheet supply glut didn’t materialize. We were instead greeted in early 2023 by a resilient economy and a supply deficit with imports low, AHMSA halting production, and new capacity slow to ramp.

Many of those factors have reversed. Fears of a recession have been kicked into H2. Certain new capacity continues to ramp up slowly. But some of you might be getting calls from mills you might not have heard from for a while who are looking to sell their increased capacity. Import prices for summer delivery to the US, meanwhile, remain sharply lower than current domestic prices.

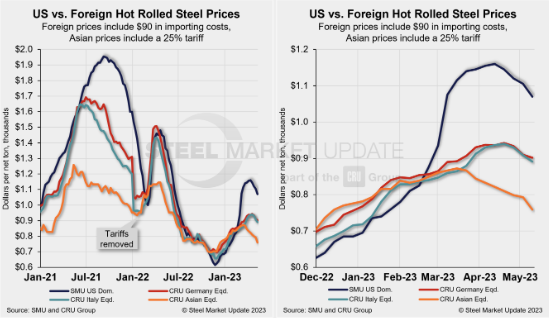

Here is a reminder of how big the gap is between US hot-rolled coil prices and those in the rest of the world. The dark blue line is the US:

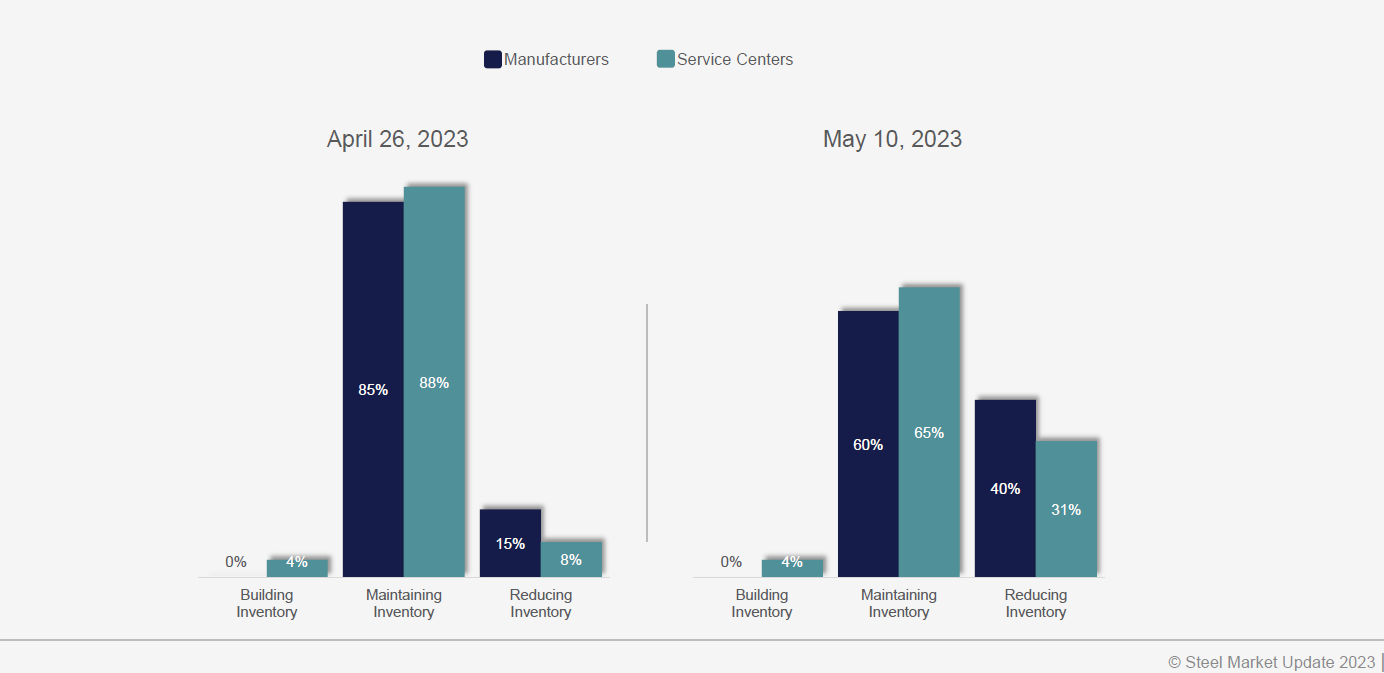

Another big change we picked up in our most recent survey is inventory management. Service centers and manufacturers in late April were mostly looking to maintain their inventories. Now, many looking to slash stocks:

In late April, only 15% of manufacturer respondents and 8% of service center respondents said they were reducing inventories. That figure has jumped to 40% and 31% respectively.

Why are so many steel consumers now cutting prices and looking to move inventory? Here’s what some of told us.

“We’re only buying when we absolutely need steel.”

“Only buying for contracted work. Holding off on stock inventory purchases.”

“Buying to demand and forecast – no speculation to speak of.”

“No reason to buy right now as the slide starts and picks up the pace.”

“We believe prices will drop over the next few months.”

“Everyone is waiting for prices to crash, so no reason to buy.”

“High inventory levels and lower demand than anticipated.”

“Only buying what is 100% necessary – expect some holes in the inventory.”

That’s a bit dark. I’ve been ending these columns as well as recent webinars and speaking engagements on an optimistic note.

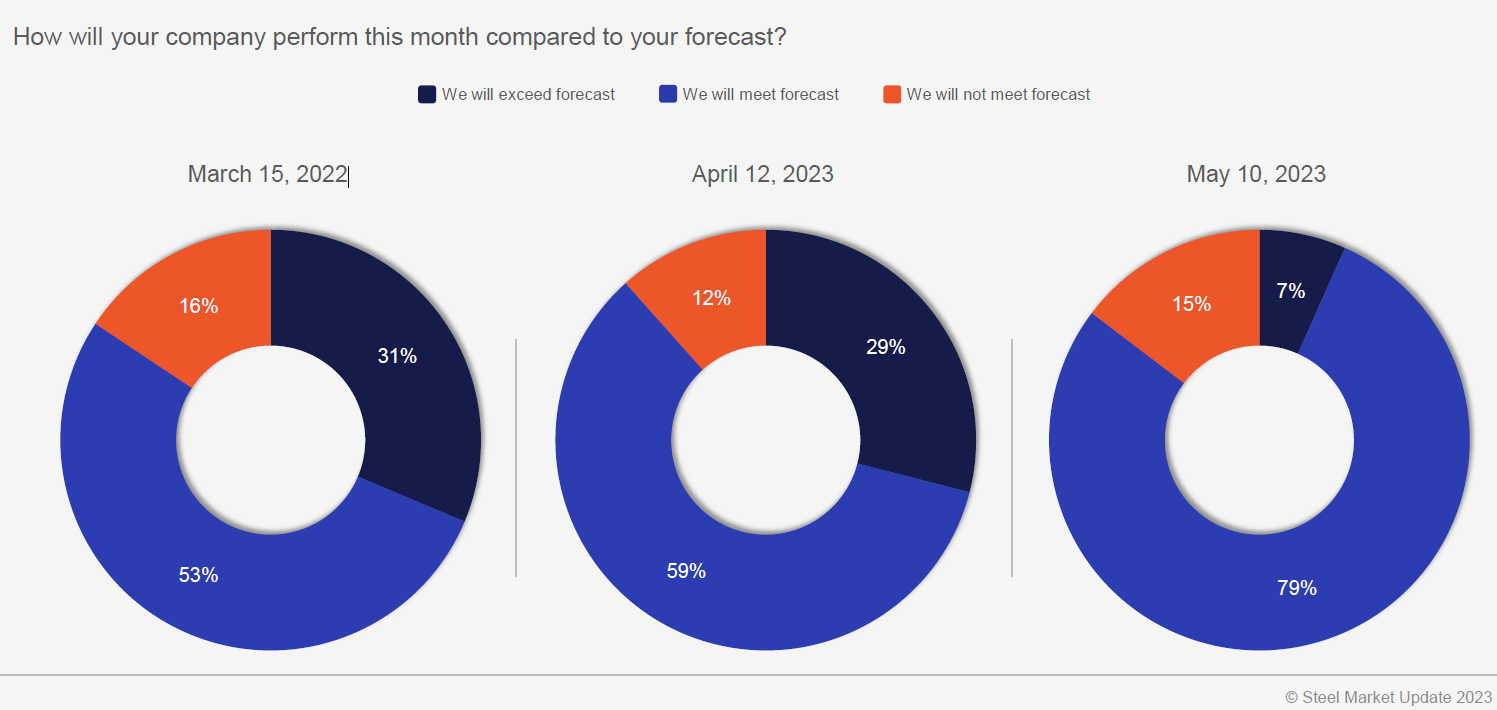

I’ll do that again today. Most respondents, 85%, continue to say that they will meet or exceed forecast:

We’ve seen that trend in place most of this last year. It remains there now despite what I outlined above and what we’ve noted in recent newsletters – lower mill shipments, shorter lead times (for galvanized in particular), and mills more willing to negotiate lower prices.

But there are clouds on the horizon this time. Only 7% say they will exceed forecast in May, down from ~30% in March and April. The music has definitely not stopped on demand. But it’s a little softer than it had been.

Is it just a case of the summer doldrums arriving a little earlier than usual? Or is it something more than that?

There are warning signs flashing now. Do they mean prices are about to crash? What if everyone draws down inventories in expectation of a correction, but then a slowdown in steel doesn’t actually happen? Could we see another repeat of late 2022 – where prices fall, perhaps significantly, as people move to the sidelines – and then shoot back up again just as quickly when everyone returns to the market at once?

Again, I’m not making any predictions here. I’m just running through some scenarios that I think are worth gaming out. In the meantime, thanks from all of us at SMU for your continued support.

SMU Steel Summit

It was great catching up with some of you at the Boy Scouts Metals Industry dinner last week on a beautiful day in Chicago.

A few of you mentioned that you’d already registered and booked travel for Steel Summit on Aug. 21-23 in Atlanta. Nearly 500 people have already done so, which means we’re running ahead of last year’s record attendance.

That means our significantly discounted room blocks are going quickly. Don’t wait until the last minute. Register and get yours now!

By Michael Cowden, michael@steelmarketupdate.com