CRU

January 5, 2024

CRU: Iron ore rises despite slow market

Written by Aaron Kearney-Keaveny

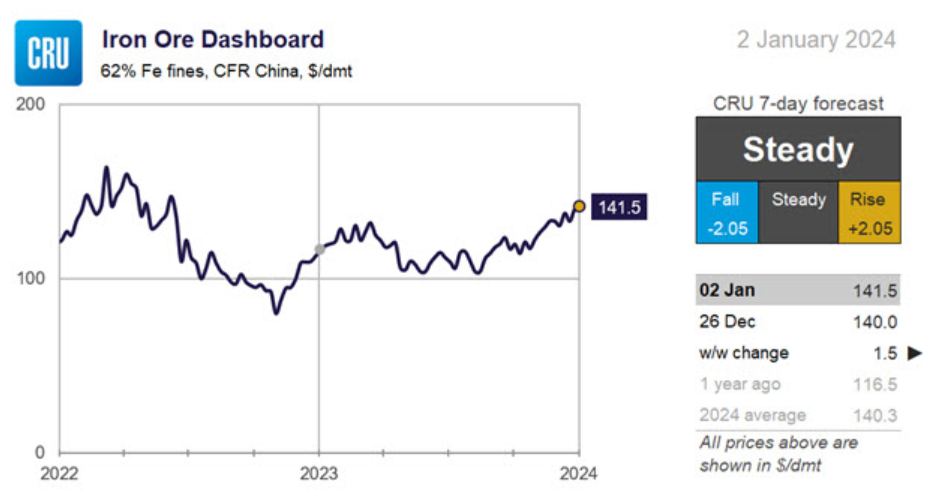

The iron ore price has edged up further from the already high level seen last week. The market is generally slow, meaning that the moderate price increase came from the bullish outlook from the market following last week’s stimulus announcements from China and expectations of restocking picking up.

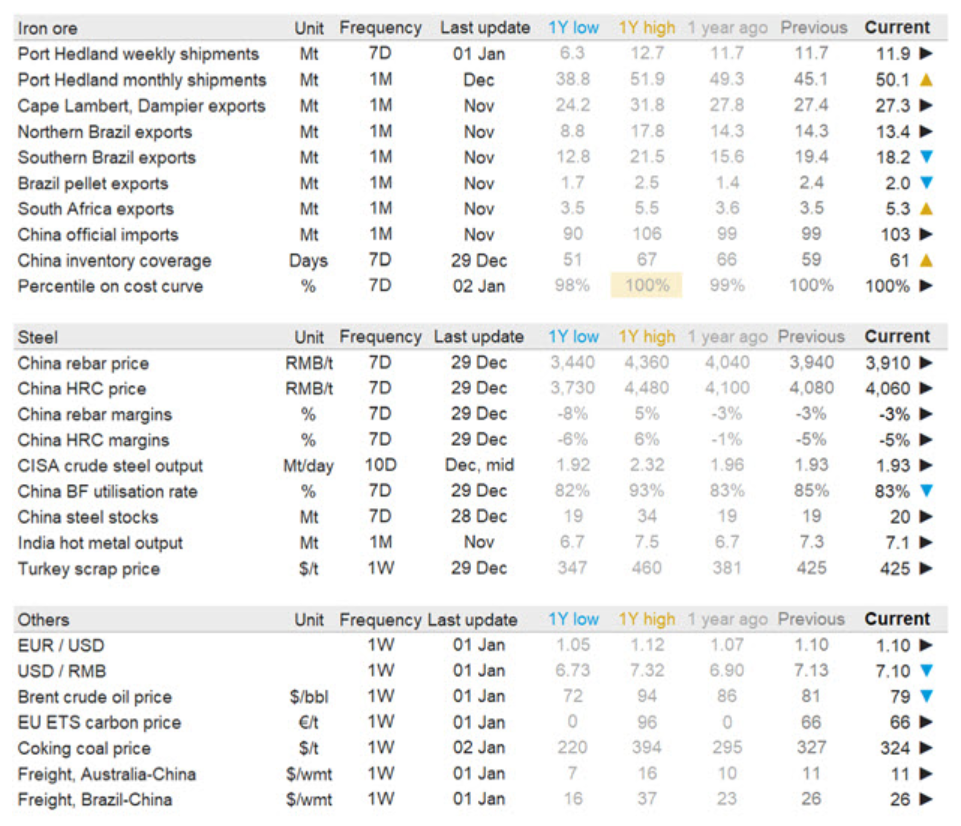

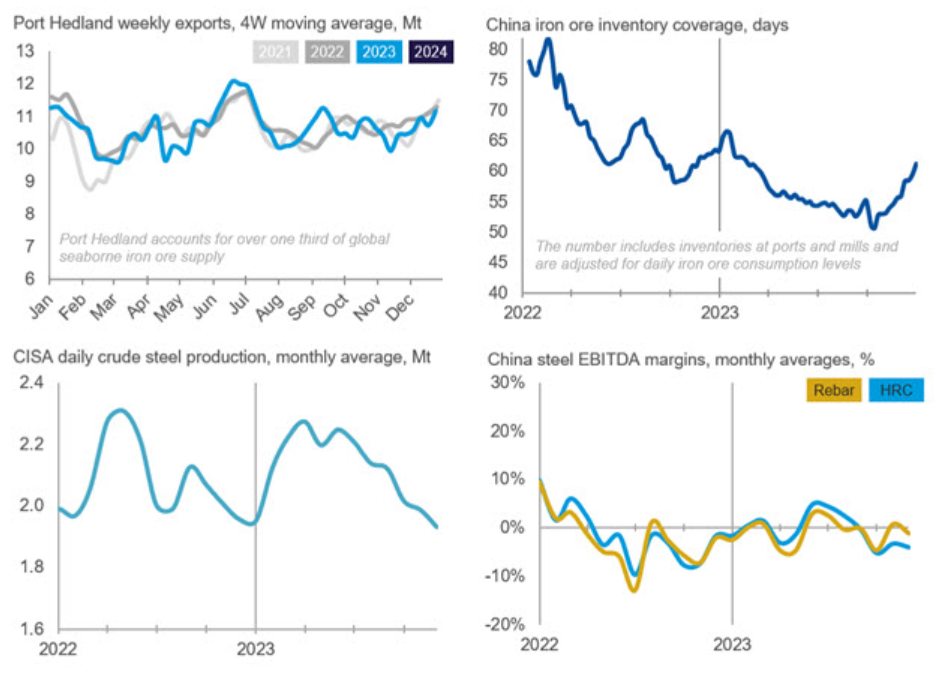

Supply fell w/w from both Australia and Brazil as operations slowed down over the Christmas holiday period. Port Hedland volumes edged up by 0.2 million metric tons to 11.9 million metric tons, outperforming last year’s volume by almost a full 1 million metric tons, but Rio Tinto’s volumes declined by much more. FMG announced that there was a train derailment close by the Cloudbreak mine on December 30, which is expected to be resolved by January 2. Shipments have held steady, though the drawdown in port stocks will affect future outflow. Mine stocks are generally low so production is likely to continue as normal. Shipments from northern Brazil held steady w/w while shipments from southern Brazil declined.

Elsewhere, Ukrainian shipments have continued throughout December, primarily from Yuzhney Port. The derailment in Sweden is now believed to be worse than previously expected, with the impacts expected to last for the entirety of Q1. Indian exports were at the highest level in December in two years, with the high international price and low-grade preference incentivizing exportation.

Chinese domestic steel prices fell slightly by $3–4 /metric tons through the week prior to the New Year holidays. Our assessed HRC and rebar price on the last working day in 2023 was ~$11 /metric tons and ~$21 /metric tons lower than that in the year-beginning respectively. In the last week of 2023, long products demand remained weak and, in fact, was weaker than that in 2022 when China was yet to recover from nationwide Covid-19 infections. In contrast, flat products demand was stable and stronger than in previous years based on sample data.

Lower steel margins resulted in more BF idlings, with the surveyed capacity utilization rate falling to 83%. Lossmaking steelmakers remained reluctant to massively restock. As a result, iron ore port inventories rose to 120 million metric tons. Operating restrictions were heard to have tightened in Hebei province, leading to increased demand for direct charge materials.

Future price increases will be limited as the price is already at a very high level and the supply disruptions will have limited effects on the market as a whole. However, restocking will pick up in China and Europe, preventing the price from falling down significantly, meaning that we expect further stability from here onwards.

This article was first published by CRU. Learn more about CRU’s services at www.crugroup.com/analysis.

Join us on Jan. 24, 2024 for a Community Chat with CRU principal analyst and iron ore expert Erik Hedborg. Click here to register.