Logistics

June 23, 2024

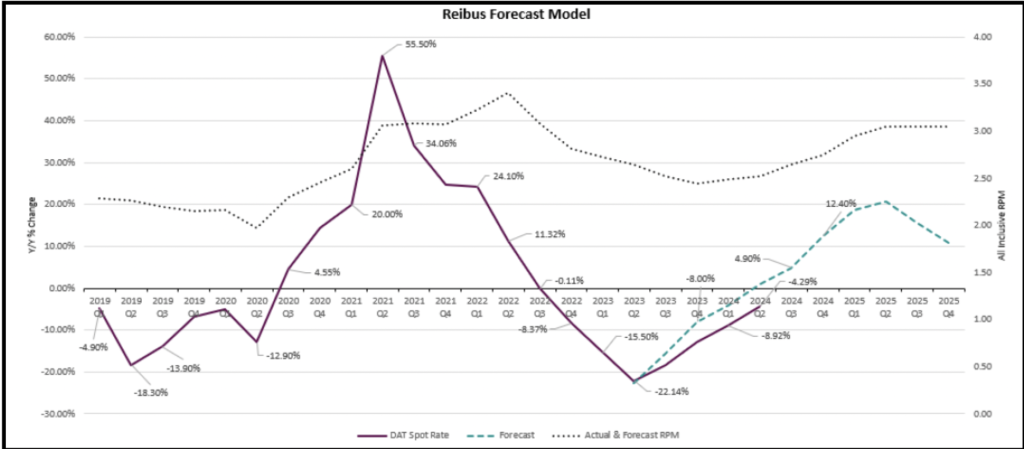

Reibus: Could seasonal shipping peaks drive up spot market rates?

Written by Robert Martin

Flatbed rates remain roughly 20% higher than dry van but have stayed relatively calm for the first half of 2024. They have risen just 5% in the first half of the year and have remained negative on a year-over-year (y/y) basis.

With two weeks remaining in the quarter, it looks like Q2 flatbed spot rates will close -4% y/y, about 5% below our forecast. The flatbed market is seeing a seasonal uptick in certain markets as expected but, overall, supply and demand remain relatively balanced.

After nine quarters of tough sledding, the question remains, will supply continue to hang on and slowly exit the marketplace, thus keeping rates rather tame? Or will enough carriers get fed up and throw in the towel to have a marked impact on the rate environment?

We continue to see small month-over-month (m/m) increases at a national level, but they have gone relatively unnoticed to this point. Both third parties and asset-based providers continue to plod along as contract rates continue to reset lower (following spot rates) and a tough spot market remains below the average operating costs for most providers on a per mile basis. Looking ahead, we expect rates to continue to rise but it will be a slow burn upward.

That said, this isn’t the first time we’ve seen this pattern. So maybe we shouldn’t be so surprised to see the last leg taking this long to resolve itself. Historically, things do get darkest before the dawn for transportation market cycles. Carriers are pushed to the brink and either exit all together, consolidate, or pull capacity offline. We saw similar conditions dating back to 2016 when we witnessed what appeared to be a bonus quarter of deflationary market conditions and then another. Although that was brought on by a Black Swan event, in Q1 2020, to close out the subsequent market cycle. In each of the previous two cycles, the inflationary legs that came next felt both dramatic and unexpected prior to them taking place.

Moving into the back half of 2024, driven by cost-cutting finance and executive teams looking to save wherever possible, it is reasonable to expect the three- and six-month bids that have been prominent over the past couple of years begin to transform back into one- and two-year commitments. Thus, this perpetuates the market conditions that create the boom-and-bust cycles. For carriers, the impending upswing in the market will certainly be welcomed and procurement teams should prepare and have an agile plan to adjust when the market does eventually start to shift.

Produce season has had a rather muted impact on rates. But as has been noted in the past, during the y/y deflationary phases of the TL market cycle seasonal dislocations like produce, Christmas trees, and holiday retail sales tend to have a muted impact on spot rates. This is given the surplus supply that exists in the market that acts as a sponge soaking up excess and unplanned shipment volume.

As the market moves back in the direction of relative supply scarcity, those volatile volumes can have a much larger impact on rates, especially in volatile markets. So as the market continues to approach equilibrium after the last nine quarters of y/y spot rate deflation, we could see seasonal shipping peaks in Q3 and Q4 drive spot market rates out of the South, Southeast, and West Coast up materially in a way that the market hasn’t experienced since 2021.

On the supply side, class 8 truck orders continue to trend a bit below replacement rates, signaling carriers are not buying as many new trucks. They are keeping current equipment longer, and not replacing equipment as fast once it has run outlived its useful life.

On the demand side, consumption remains healthy at +2.4% y/y and industrial production remains positive y/y at +0.3%. That being said, shipment volumes, according both Cass and the ATA, are both down on a y/y basis at -9.5% and -5.2%, respectively. These two indicators typically lag the market and are reported by a mix of carriers and shippers. A divergence in these readings is not atypical for this period in the market cycle. Overall, rates remain balanced but market conditions tend to shift quickly at this point in the cycle.

Editor’s note: This column appeared first in Recycled Metals Update (RMU), SMU’s new sister publication. RMU is devoted entirely to the ferrous and nonferrous recycled metals markets. If you’d like to learn more, visit RMU’s homepage and take out a free, 30-day trial.