CRU

April 4, 2025

CRU: Trump’s sweeping tariffs could derail the US met coal industry

Written by Banmeet Khurmi

The US government’s ‘Liberation Day tariffs’ intend to reshore industrial production and rebalance lopsided trade balances. This could lead to US metallurgical coal exporters (many already high-cost swing producers) being priced out of the market.

Most US coal production and employment occurs within Donald Trump’s political heartlands. Any short-term upside to domestic steel production from tariffs cannot match the sheer scale of US metallurgical coal that could become unprofitable to export.

Moreover, any reshoring of steel production will take years, not months or quarters to achieve. This lossmaking US metallurgical coal supply would likely exit the seaborne market if retaliatory tariffs were to target metallurgical coal from the USA.

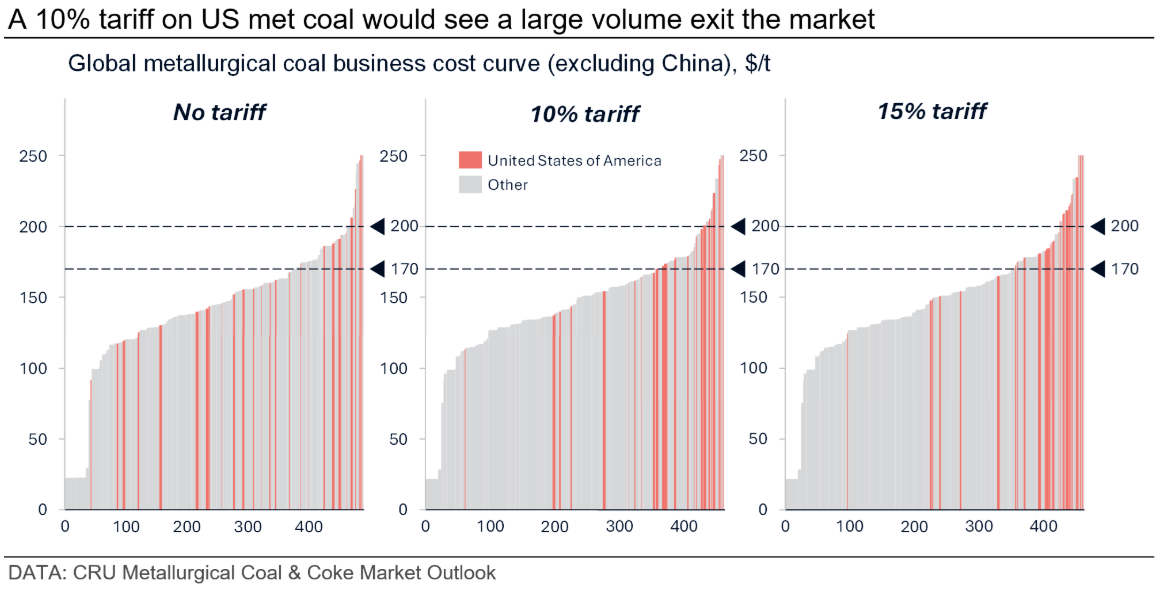

Tariffs will make large volume of US supply unprofitable

CRU’s Metallurgical Coal Business Cost curves below demonstrate the impact of retaliatory tariffs on US met. coal cost competitiveness, should key trading partners in the EU and Asia apply tariffs that would target this industry.

As the trade war is still in its early days, it is unclear if retaliatory tariffs will be applied, and how broadly this policy will be adopted. CRU has assessed the potential impact of a 10% and 15% tariff on the competitiveness of US met. coal in the traded metallurgical coal market.

At a price of $200 /ton for premium HCC (FOB Queensland basis), around 14% or ~9 metric tons (Mt) of US met. coal production is unprofitable prior to any tariff consideration. Under a 10% tariff scenario, 30% (~19 Mt) become unprofitable. A steeper 15% tariff scenario would see 38% (~24 Mt) turn loss-making.

We have used $200 /t as the benchmark price even though the hard coking coal price is currently assessed at $170 /t. At current prices, about 40 Mt or two-thirds of US met. coal supply would be unprofitable. However, we expect market balances to tighten and prices to rise if a significant volume of lossmaking US met. coal leaves the market. Hence, $200 /t would a more realistic benchmark.

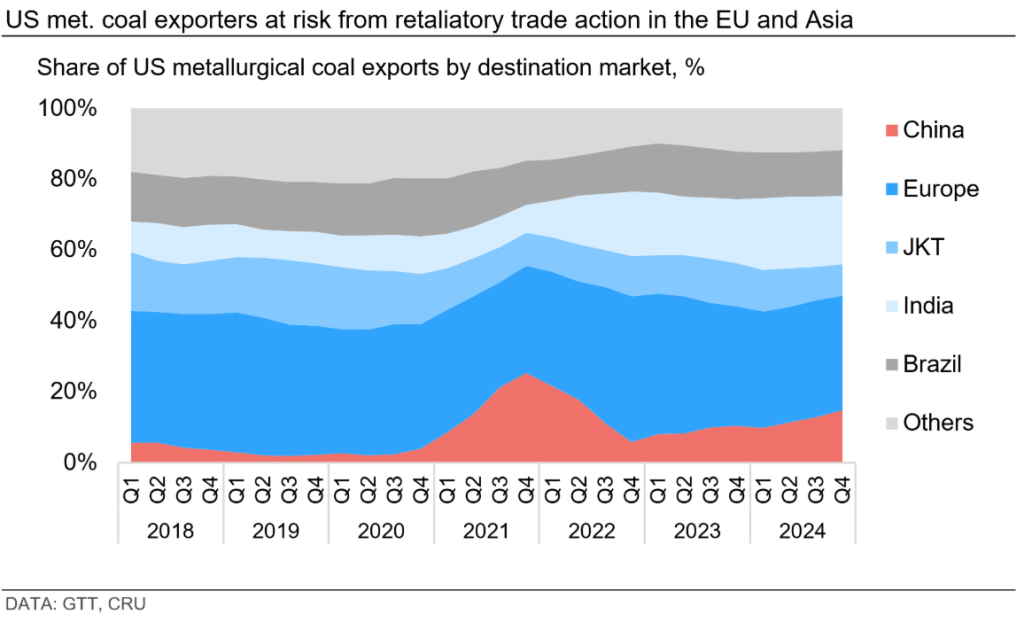

US producers brace for impact of EU and JKT reactions

Europe is the natural market for US met. coal, importing a third of US exports or 16 Mt in 2024. India imported 10 Mt in 2024, while the JKT region has imported ~6 Mt/y in recent years. China already applied counter tariffs in February, leading to a sudden decline in US coal flows to China. Retaliation from India appears less likely, given the following reasons:

1. Positive foundations of the Modi-Trump relationship, and ongoing bilateral trade negotiations;

2. India’s steel sector is lobbying for increased met. coal availability and control of inflation;

3. India’s recent track record of leveraging bilateral relationships (e.g. discounted access to Iranian/Venezuelan/Russian oil and Russian coal)

Nonetheless, Indian buyers will seek a discount from US sellers, who will also need to factor higher freight costs to access the Indian market. This will have similar impacts to tariffs on US met. coal producers, leading to lower netback prices.

Expect higher met. coal prices and more volatility

US met. coal producers, which exported 50 Mt or 75% of their production in 2024, face a significant risk from retaliatory trade actions in key destination markets such as the EU, China and the JKT region.

A moderate tariff rate of 10% would make nearly a third of US production (or ~20 Mt) unprofitable at $200 /t. The trade war will put upward pressure on global metallurgical coal prices, and lead to a significant volume of high-cost US met. coal production exiting the market.

This article was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.