Market Data

June 24, 2025

SMU Price Ranges: Sheet slips despite tariff and Middle East shocks

Written by Brett Linton & Michael Cowden

Prices for steel sheet edged down this week despite Section 232 tariffs remaining at 50% and a US strike on nuclear facilities in Iran over the weekend.

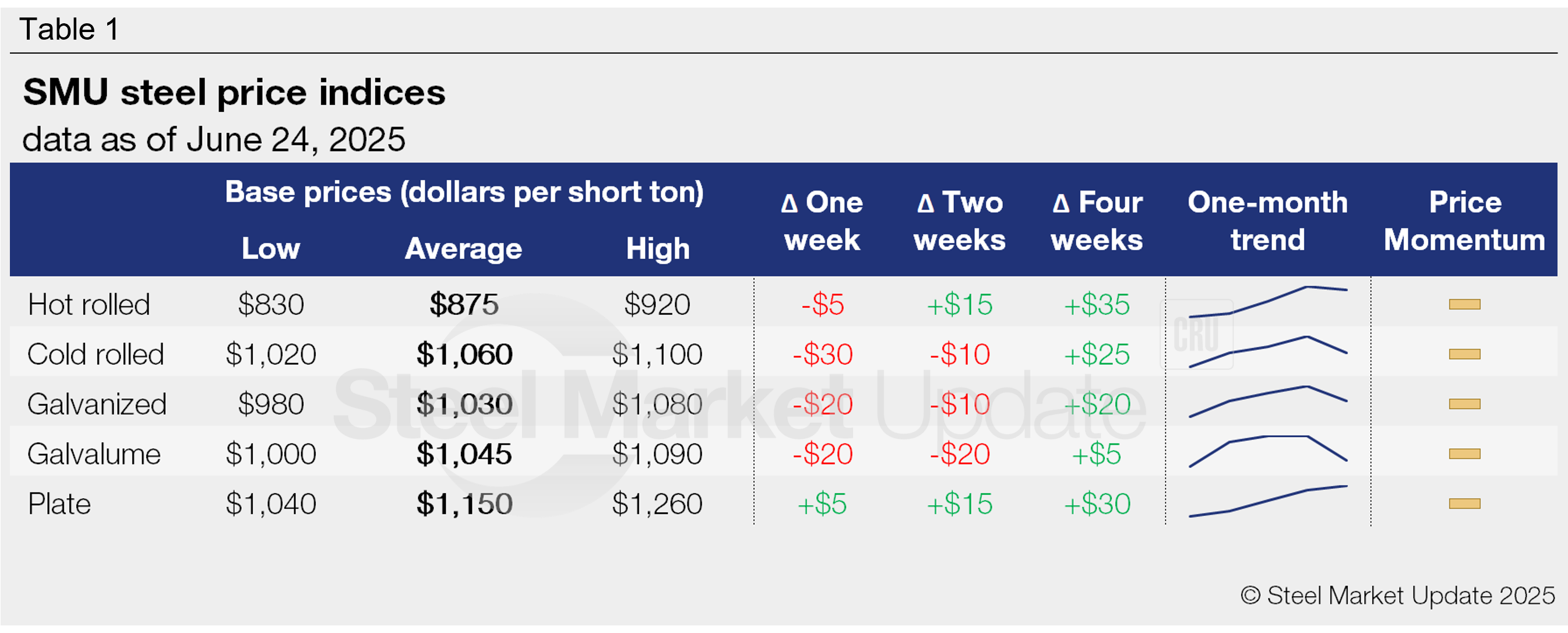

Case in point: SMU’s hot-rolled (HR) coil price stands at $875 per short ton (st) on average. That’s down $5/st from last week and marks the first decline since President Trump announced plans in late May to double S232 tariffs.

The declines reflect continued uncertainty about tariff policy and demand. Noting limited spot activity, several market participants said that tariff fatigue had been replaced by a more broad-based fatigue. And while inventories have declined, lead times haven’t significantly extended – meaning buyers don’t feel much urgency to buy now.

In the past, for example, a massive increase in tariffs combined with a conflict in the Middle East would have sent oil prices soaring – and steel prices along with them. But market participants said such shocks have become normalized to the point that they have lost their ability to shock markets.

But not everyone took that view. Some sources predicted that uncertainty around demand would keep buyers cautious – something that could lead to higher prices in late Q3 or Q4, especially should imports remain low and should buyers continue to reduce inventories.

They also noted that current pricing, while not as high as some had predicted initially after the 50% tariffs were announced, was still strong by historical standards. At current levels, they noted, mills remained profitable. And there is no need for producers to chase HR toward $1,000/st, a number which might only serve to make imports attractive again.

In light of this, SMU’s price momentum indicator has been adjusted from higher to neutral for all sheet and plate products, signaling that we see no clear direction for prices over the next 30 days.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $830-920/st, averaging $875/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for hot-rolled steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.7 weeks as of our June 12 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil

The SMU price range is $1,020–1,100/st, averaging $1,060/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is down $40/st. Our overall average is down $30/st w/w. Our price momentum indicator for cold-rolled has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-9 weeks, averaging 6.8 weeks through our latest survey.

Galvanized coil

The SMU price range is $980–1,080/st, averaging $1,030/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is down $40/st. Our overall average is down $20/st w/w. Our price momentum indicator for galvanized steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,058–1,158/st, averaging $1,108/st FOB mill, east of the Rockies.

Galvanized lead times range from 4-8 weeks, averaging 6.3 weeks through our latest survey.

Galvalume coil

The SMU price range is $1,000–1,090/st, averaging $1,045/st FOB mill, east of the Rockies. The lower end of our range is down $10/st w/w, while the top end is down $30/st. Our overall average is down $20/st w/w. Our price momentum indicator for Galvalume steel has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,268–1,358/st, averaging $1,313/st FOB mill, east of the Rockies.

Galvalume lead times range from 5-7 weeks, averaging 6.3 weeks through our latest survey.

Plate

The SMU price range is $1,040–1,260/st, averaging $1,150/st FOB mill. The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w. Our price momentum indicator for plate has been adjusted to neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 4-8 weeks, averaging 5.6 weeks through our latest survey.

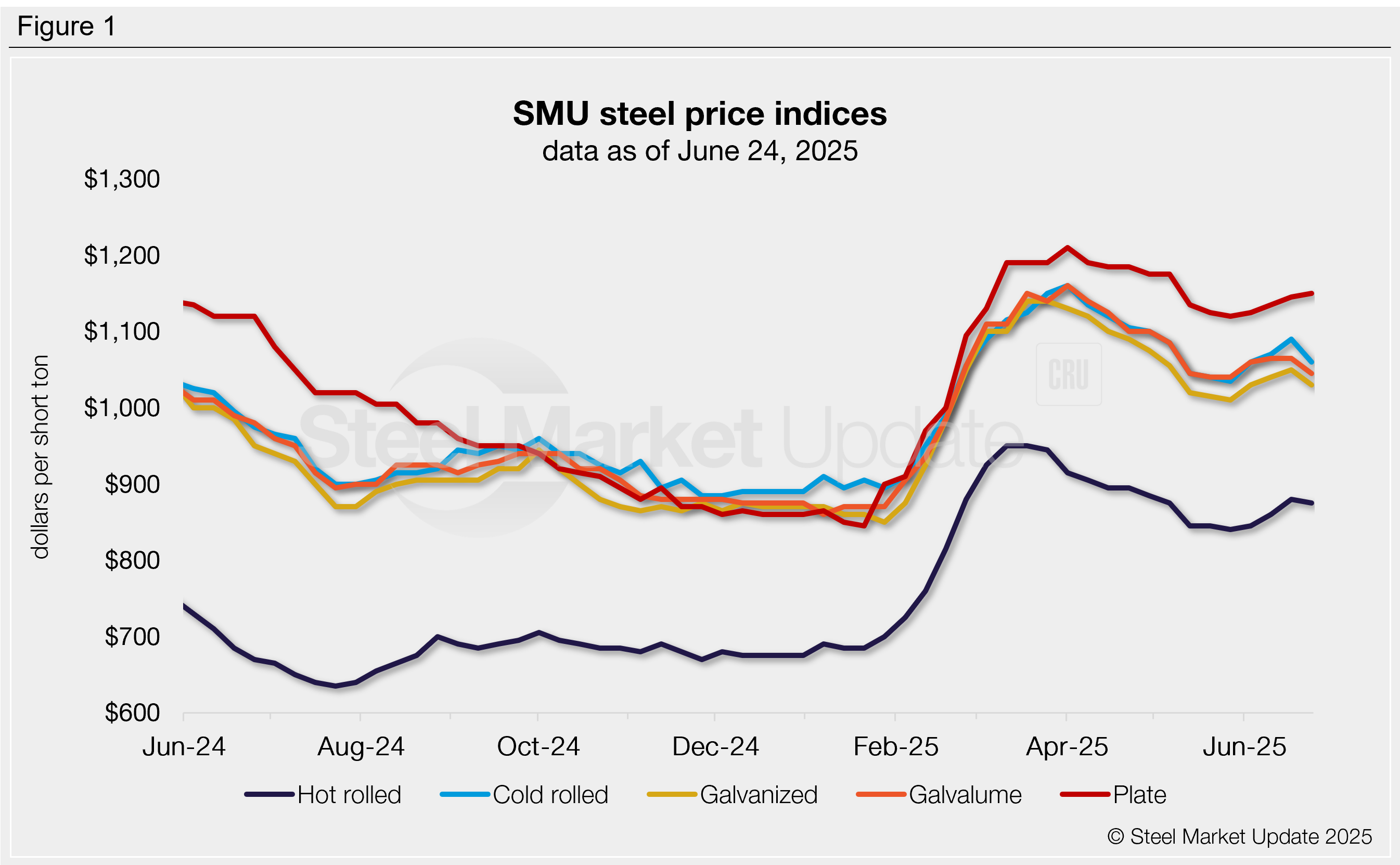

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton