Market Data

September 9, 2025

SMU Price Ranges: Some predict bottom is near as big discounts dry up

Written by Brett Linton & Michael Cowden

Sheet prices were mixed this week as some mills continued to offer significant discounts to larger buyers while others have shifted toward being more disciplined, market participants said.

A word on price ranges

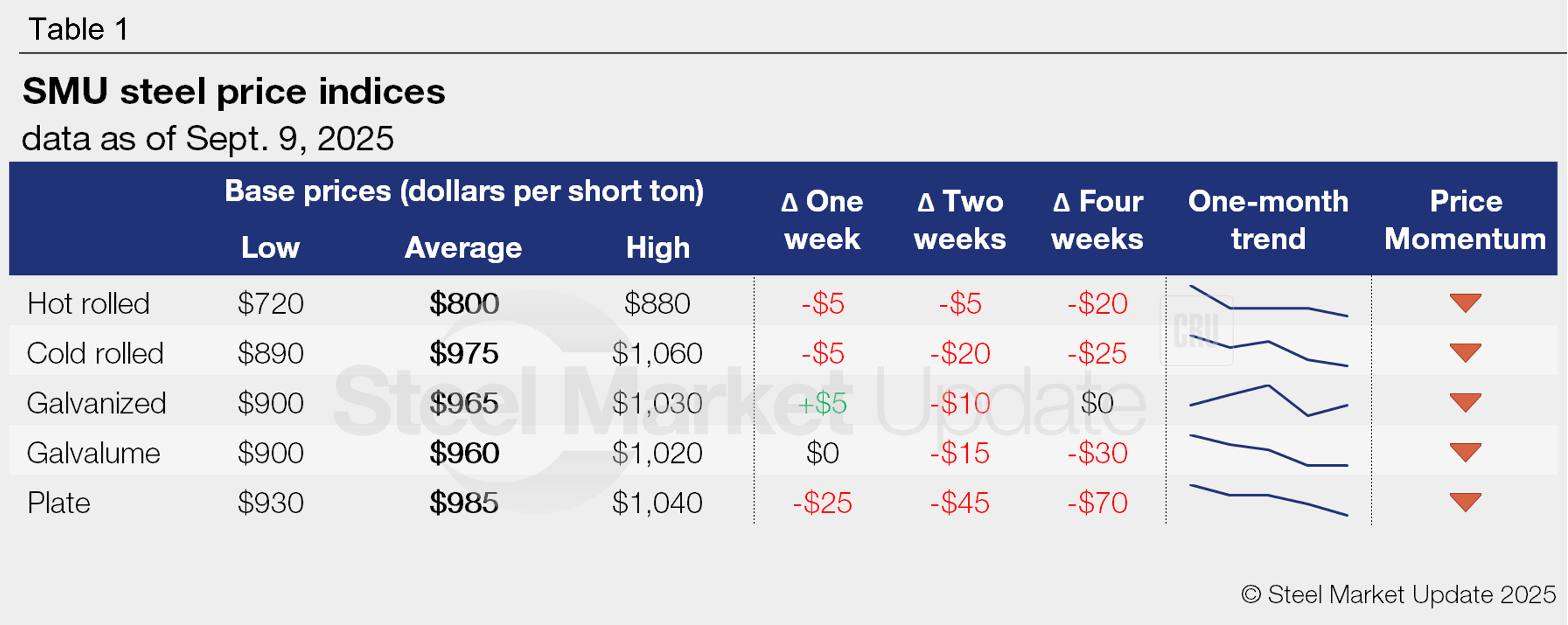

The low ends of our sheet price ranges were flat or lower, and the high ends of our ranges were flat or higher. That meant that prices were little changed on average, even as our price ranges expanded.

A wide spread between highs and lows can indicate a market at or near an inflection point. In the current cycle, some mills had to discount to get enough volume to push lead times into September – and some are still doing so. But now that lead times are into October, others should have a stronger hand to at least hold the line on prices – and maybe even to increase them, sources said.

The case of HR

Case in point: SMU’s hot-rolled (HR) coil price stands at $800 per short ton (st) on average, down $5/st from last week.

The low end of our range dropped to $720/st as certain US mills continued to match deep discounting from Canadian mills, some of which are distressed in the face of the 50% Section 232 tariff on imported steel.

But market participants noted that other mills, which had previously been in the low $700s/st, have more recently been refusing to match Canadian prices and are now unwilling to go below $740-750/st – even for larger buyers.

The high end of our range reflects Nucor’s list price for spot tonnage. But sources noted comparatively few transactions at that level. Most transactions, even for smaller tonnage, are in the low- to mid-$800s, they said.

Cold-rolled, coated, and plate prices

A similar trend played out across other products. Our cold-rolled coil price stands at $975/st on average, down $5/st from a week ago – but that relative stability came as both the low and high end of our ranges expanded. Galvanized prices were at $965/st on average, up $5/st from last week. And Galvalume prices were unchanged at $960/st on average.

Plate bucked the trend of relative stability in sheet. Our plate price fell to $985/st on average, down $25/st from a week ago on more pronounced concerns about demand in that sector.

Broader trends and momentum

That said, relatively few sources were bullish about sheet demand – at least in the short-term. They said that a potential bottom in prices might instead result from a reduction in supply.

That’s because flat-rolled steel imports continue to fall in the wake of the 50% tariff. Inventories are expected to continue to move lower with buyers cautious about restocking. And U.S. Steel’s decision to halt the hot-strip mill at its Granite City Works near St. Louis should, along with planned outages, reduce domestic supplies.

And some remained bullish on the demand outlook for the fourth quarter and into early 2026. They predicted that lower interest rates would provide a psychological boost to consumer markets as steel begins to see more activity from data centers, related energy infrastructure, and from Biden-era infrastructure initiatives.

Despite that, our momentum indicators continue to point lower with prime scrap settling down $20 per gross ton (gt) and with no immediate catalyst for higher prices.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $720–880/st, averaging $800/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is up $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for hot-rolled steel remains at lower, meaning we expect prices to decline over the next 30 days.

Lead times for HRC range from 3–6 weeks, averaging 4.5 weeks as of our September 4 market survey.

Cold-rolled coil

The SMU price range is $890–1,060/st, averaging $975/st FOB mill, east of the Rockies. The lower end of our range is down $30/st w/w, while the top end is up $20/st. Our overall average is down $5/st w/w. Our price momentum indicator for cold rolled remains lower, meaning we expect prices to decline over the next 30 days.

Lead times for CRC range from 4–8 weeks, averaging 6.0 weeks through our latest survey.

Galvanized coil

The SMU price range is $900–1,030/st, averaging $965/st FOB mill, east of the Rockies. The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w. Our price momentum indicator for galvanized steel remains lower, meaning we expect prices to decline over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $978–1,108/st, averaging $1,043/st FOB mill, east of the Rockies.

Galvanized lead times range from 4–8 weeks, averaging 6.1 weeks through our latest survey.

Galvalume coil

The SMU price range is $900–1,020/st, averaging $960/st FOB mill, east of the Rockies. Our entire range is unchanged w/w. Our price momentum indicator for Galvalume steel remains lower, meaning we expect prices to decline over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,168–1,288/st, averaging $1,228/st FOB mill, east of the Rockies.

Galvalume lead times range from 5–8 weeks, averaging 6.4 weeks through our latest survey.

Plate

The SMU price range is $930–1,040/st, averaging $985/st FOB mill. The lower end of our range is down $30/st w/w, while the top end is down $20/st. Our overall average is down $25/st w/w. Our price momentum indicator for plate remains lower, meaning we expect prices to decline over the next 30 days.

Plate lead times range from 3–7 weeks, averaging 5.3 weeks through our latest survey.

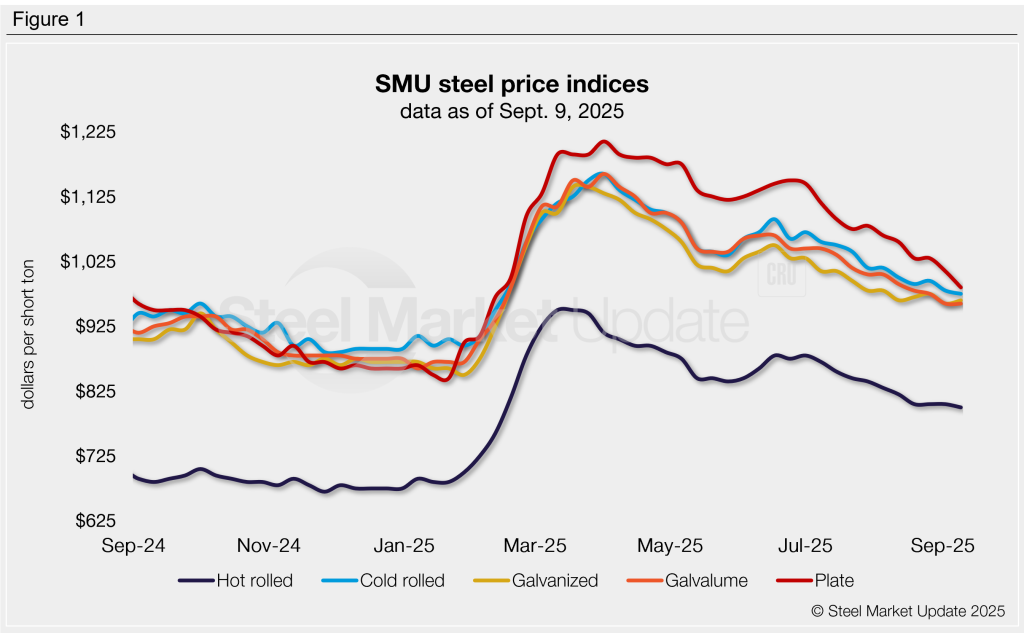

SMU note: The graphic above shows a history of our hot rolled, cold rolled, galvanized, Galvalume, and plate prices. This data is also available on our website with our interactive pricing tool. If you need help navigating the site or logging in, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton