Analysis

April 14, 2026

Final Thoughts: SMU Scrap Survey

Written by Ethan Bernard & Stephen Miller

The unpredictability of the scrap market may lead you to consult the tea leaves to get a jump on the next guy. Well, here at SMU, we have the next best thing: the SMU Scrap Survey.

Every month, SMU polls participants in the ferrous scrap market on a variety of topics. These include prices, business conditions, and tariffs, among others. Getting opinions from people all along the scrap value chain can give you insights into the market. And, often, our survey respondents’ intuitions turn out to be right.

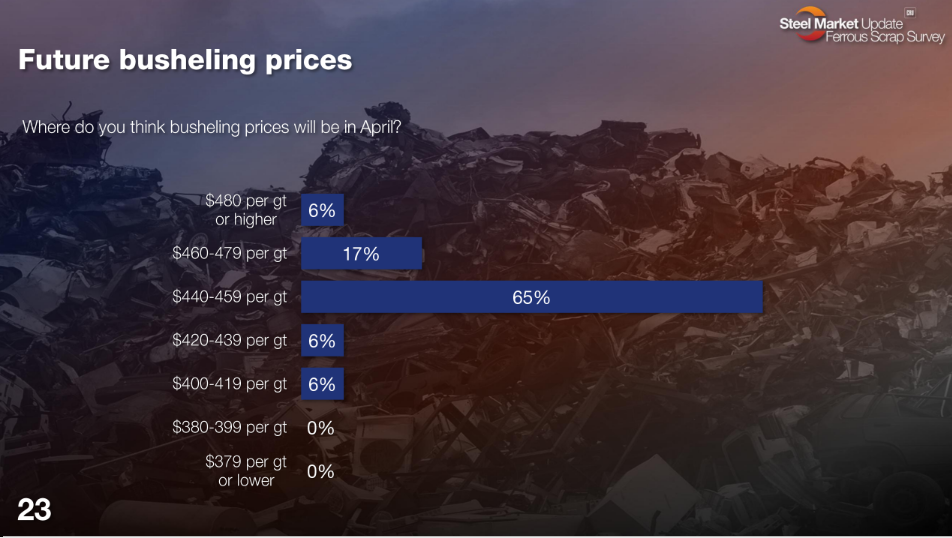

For example, this month’s survey arrived just as the April trade was settling. Last week, SMU reported US scrap tags in April were flat on busheling and down $20 per gross ton (gt) on HMS and shred. The vast majority of survey respondents were spot on, with 68% saying prime scrap prices would settle even with March. However, 21% predicted prices would be up, and 11% thought they would be down.

But what’s the pulse of the market right now? You have to look no further than our Current and Future Sentiment Indices, which are at all-time highs and have moved even with each other for the first time (usually Future Sentiment outpaces Current Sentiment).

From the improved melt rate at US steelmakers, rising steel and pig iron prices, to a recovering export market, the outlook for scrap tags is getting rosier.

However, will the continuing hostilities in the Middle East and increasing freight rates, coupled with lingering tariff uncertainty, derail the scrap rebound?

In the export trade, respondents reported increased export demand, with 67% saying it has increased. Over the last three months, this reading has been under 30%. Likewise, with export prices. In the survey, 39% said prices were improving vs. 23% in March.

Another reading of note is 67% of respondents signaled their belief that scrap supply vs. demand is now in balance. This is the highest reading since December.

Let’s take a look at what else these participants are seeing on demand, tariffs, and pricing. We’ll post the slides, followed by a selection of respondents’ comments.

Want to share your thoughts? Contact david.schollaert@crugroup.com to be included in future market questionnaires. (For Premium subscribers, the full results are available here.)

Comments for busheling, shred, and HMS on April pricing and market dynamics

First, let’s see what respondents said regarding the individual grades as the market was settling, and where they saw prices. (For a look at SMU’s April pricing article, click here.)

Busheling

“Logistics cost is increasing, and mills are pushing pricing up due to energy increases.”

“Good demand.”

“Logistics cost has increased, and demand is stable.”

“More mills have been buying prime with the compression in pricing with auto shred and prime.”

“March pricing.”

Shred

“Supply-driven and increased freight.”

“Logistics cost has increased, and demand is stable.”

“Flows into shredders have improved. Shredders will need to lower pricing to have mills start buying constantly again.”

“We are being told that there is a surplus of shred… not sure it is true.”

HMS

“Export is higher.”

“Logistics cost has increased, and demand is stable.”

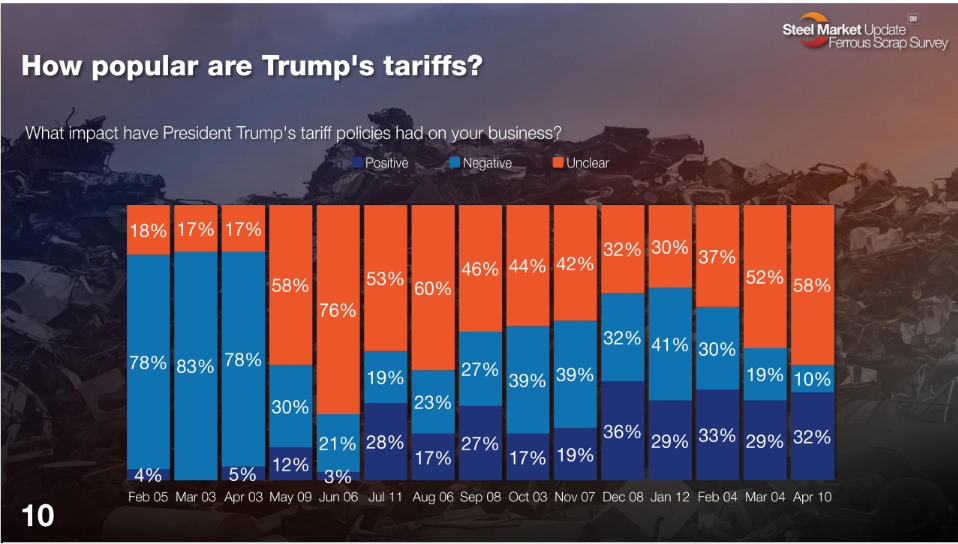

What impact have President Trump’s tariff policies had on your business?

“Pushing costs up due to quotas and tariffs.”

“I would have expected steel tariffs to help the domestic industry more than I have seen.”

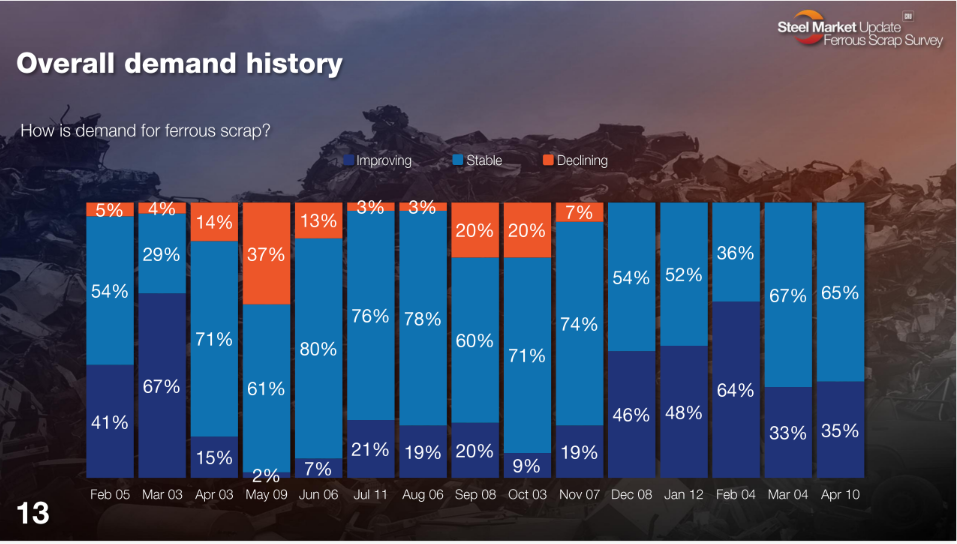

How is demand for ferrous scrap?

“Flat.”

“Stable to improving.”

“There might be some areas of declining demand, but overall, the steel industry is pretty stable.”

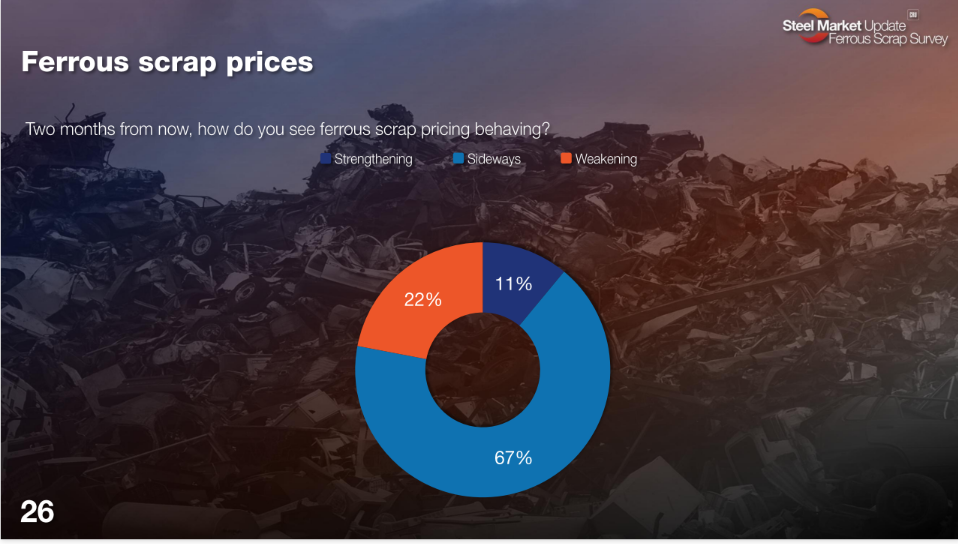

Two months from now, how do you see ferrous scrap pricing behaving?

“Delayed spring inflows.”

“Market demand will top out in May.”

“Sideways to stronger.”

“I really don’t think it is going to be healthy for the mills to push it down any further.”

Ethan Bernard

Read more from Ethan Bernard