February service center shipments and inventories report

US service centers’ flat-rolled steel supply declined for a second consecutive month in February, with shipping days of supply slipping to 52.2 on an adjusted basis, according to SMU data.

US service centers’ flat-rolled steel supply declined for a second consecutive month in February, with shipping days of supply slipping to 52.2 on an adjusted basis, according to SMU data.

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

While decarbonization has fallen out of the headlines a bit, that doesn't mean it's gone away. Tariffs, geopolitical instability, outright war... there has been a lot to write about in the last year.

Heating and cooling equipment shipments declined in January to the second-lowest rate recorded over the past nine years.

The weather is still influencing the recycled metals market as we head into spring, sources say.

US steel exports jumped 33% in January but remain historically low, according to recently released US Department of Commerce data.

The US steel market is already characterized by high prices and tight supplies, and I wouldn't be surprised if prices move higher and supplies get even tighter – at least in the short term.

SA Recycling's CEO George Adams couldn't be more upbeat about American industry.

Steel imports remained close to multi-year lows in January and February, according to US Commerce Department data released this week.

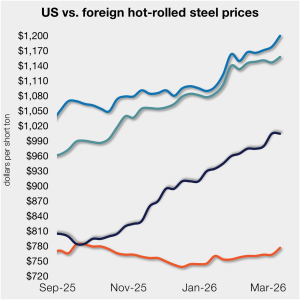

This week sources said spot prices on hot-rolled coils increased modestly.

Chinese steel export prices and Turkish longs export prices increased this week due to higher energy and raw material costs. In India, HR coil exports remained paused amid the Middle East crisis.

The market has been naturally fixated on the disruption of aluminum exports from the Persian Gulf. However, there is another shipping problem that also may have repercussions on the movement of manufactured goods originating in the Pacific. That is extreme congestion at the Panama Canal.

The latest tally of active oil and gas rigs increased in the US this week but declined in Canada, according to figures recently released from Baker Hughes.

It's been just two weeks since the US and Israel launched a joint attack on Iran. And markets are still in flux as we wade through conflicting messages from the administration on what the goals are when it could be over.

A month ago, the steel market was defined by stability. Prices had firmed and held, and the HRC futures curve appeared to be absorbing strength and follow-through rather than rejecting it. Since then, that stability has evolved into something more meaningful, repricing.

The price gap between US hot-rolled coil (HR) and landed offshore product widened this week, as stateside tags were little changed.

Domestic plate market participants expressed confidence in the overall improvement of market conditions this week.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The pig iron market in the Brazil-to-US trade flow is showing strength as supply concerns and increased logistical costs impact recent sales negotiations.

The spread between domestic hot-rolled coil and prime scrap prices widened in March, marking a six-month trend.

Sometimes it feels like current events are like a fireworks show that got set off all at once by mistake. In all the commotion, it's hard to know where to look... or where to run.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

This CRU insight demonstrates how the conflict in Middle East supports metallurgical coal prices and iron ore will be impacted by a potential decline in demand from China and rising costs, while the pellet market will be severely disrupted.

Raw production has trended upwards since the start of the year, reaching a four-year high in February.

Prices are moving up and lead times moving. And most people expect them to continue to do so for a little while longer, according to our latest survey results. But there is one big wildcard: the Iran war.

Plate sources say they’re welcoming imports as domestic mill delivery delays, extended lead times, and climbing prices make fully adopting US-produced plate products unrealistic.

Pace Industries plans to close two Muskegon die-casting plants following news of the planned shutdown of its Arkansas facility.

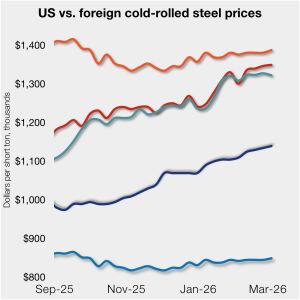

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in most offshore markets as well.

Market participant comments from this month's SMU Ferrous Scrap Survey.

Oregon Steel Mills and SSAB Americas announced higher plate prices to close out the week.