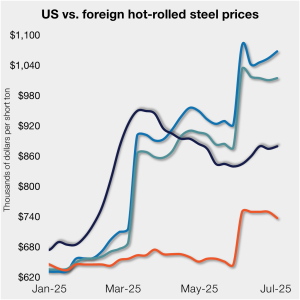

Trump increases Brazil tariff to 50%, sparking questions about pig iron prices

President Donald Trump on Wednesday said he would increase the “reciprocal” tariff on imports from Brazil to 50% effective Aug. 1. That could have big implications for pig iron.