SMU Price Ranges: Sheet and plate products inch higher

SMU's sheet and plate steel prices moved higher in unison this week.

SMU's sheet and plate steel prices moved higher in unison this week.

November ferrous scrap prices landed even with October as the market settled, sources told SMU.

Anyone standing near the Sheraton Grand at Wild Horse Pass in Phoenix, Az undoubtedly felt a kinetic charge this week. Professionals from coast-to-coast convened in the posh desert oasis for the Association of Women in the Metals Industry (AMWI) 2025 conference. Amidst the metals crowd were those leading teams and organizations through the heat of the 2025 moment.

SMU’s Current and Future Sentiment Indices for scrap decreased this month, based on the latest data from our ferrous scrap survey.

A sampling of SMU scrap survey respondent answers from November.

US steel mills have received a boost from lower import levels because of sweeping tariffs this year. However, demand remained moderate in most sectors, aside from data center construction, after the summer.

AMU's latest survey of aluminum market participants shows widening gaps in lead times, with extrusions lengthening dramatically.

SMU’s November ferrous scrap market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “ferrous scrap survey” results. Past scrap survey results are also available under that selection. If you need help accessing the survey […]

The market has entered into a bit of a quiet recalibration, the kind of pause that feels like a held breath. Prices have stopped falling. Lead times have stretched just enough to create firmer footing. The urgency of downside risk has faded, but maybe (not quite yet) moved on.

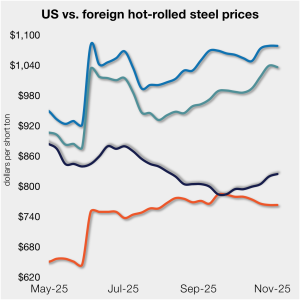

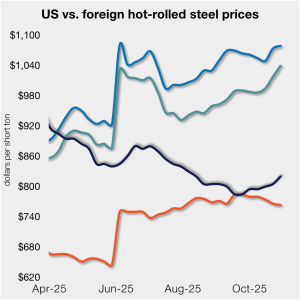

The gap between US hot band prices and imports narrowed slightly. But with the 50% Section 232 tariffs, most imports remain more expensive than domestic material.

The November scrap market in the US is appearing sideways across the board, according to several sources.

Could 2026 be the year when tariffs headwinds clear?

Most sheet prices inched up again this week following mill efforts to set a floor under tags and to increase them from there.

Most steel buyers think that steel prices will continue to rise into the 2026. But they don’t see the kinds of big gains that have characterized past market upturns, according to the results of SMU’s latest steel market survey.

The pig iron market in Brazil saw some activity last week that could present some additional options to producers there, but at lower price levels.

President Trump’s decision to suspend trade negotiations with Canada has crushed short-term expectations of any relief for Canadian producers or the US Midwest P1020 premium.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

CRU analysts break down their top takeaways from CRU's 31st Annual Ferroalloys Connections Summit, held Oct. 19-21 in Miami.

SMU’s Steel Demand Index remains in contraction, according to late October indicators. Though growth faded at a slower pace, it rebounded from one of the lowest readings year-to-date from earlier in the month.

SMU’s Steel Buyers’ Sentiment Indices both rose this week, with Current Sentiment rebounding 14 points.

Sometimes an entire news cycle happens in one week.

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet and plate products than they were in recent weeks.

Steel mill lead times marginally extended for both sheet and plate products this week, according to responses from SMU’s latest market survey.

North American auto assemblies declined in September, down 5.1% vs. August. And assemblies were also down 1% year on year.

In dollar-per-ton terms, US product is on average $141/st less than landed import prices (inclusive of the 50% tariff). That’s down from $148/st last week.

Participants in the domestic steel plate market said the plate market never accepted mill-issued spot price increases.

Angelo “Ange” Borzillo has passed away at the age of 92. He leaves behind a legacy that will endure as long as the steel he helped develop: Galvalume sheet steel.

Cliffs said it successfully completed a defect-free trial production of exposed steel parts using aluminum-forming equipment in collaboration with an unnamed OEM,

SMU’s hot-rolled coil price increased for a third consecutive week. And the gains were more pronounced this time following a price hike initiated on Friday by NLMK USA.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.