Fed Beige Book: Economy improves, but manufacturing weak

While general economic conditions across the US improved slightly over the last six weeks, activity in the manufacturing sector was weak, according to the Fed’s latest Beige Book report.

While general economic conditions across the US improved slightly over the last six weeks, activity in the manufacturing sector was weak, according to the Fed’s latest Beige Book report.

Prices of steelmaking raw materials have moved in different directions over the last 30 days, according to Steel Market Update’s latest analysis.

A lot of economists were predicting a recession last year. Ken Simonson, chief economist for The Associated General Contractors of America (AGC), wasn’t one of them.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

Following a strong February, US housing starts eased through March to a seven-month low, according to the most recent data from the US Census Bureau.

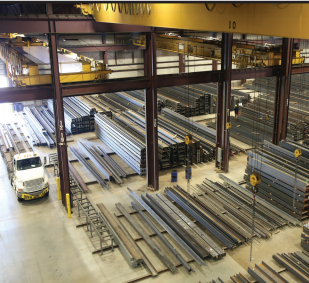

Flat Rolled = 58.3 shipping days of supply Plate = 60.6 shipping days of supply Flat Rolled US service center flat-rolled steel inventories edged up in March as shipments remained low. At the end of March, service centers carried 58.3 shipping days of supply on an adjusted basis, up from 56.6 shipping days in February. […]

New York state saw a continued decline in manufacturing activity in April, according to the latest Empire State Manufacturing Survey from the Federal Reserve Bank of New York

Last week was a newsy one for the US sheet market. Nucor’s announcement that it would publish a weekly HR spot price was the talk of the town – whether that was in chatter among colleagues, at the Boy Scouts of America Metals Industry dinner, or in SMU’s latest market survey. Some think that it could Nucor's spot HR price could bring stability to notoriously volatile US sheet prices, according to SMU's latest steel market survey. Others think it’s too early to gauge its impact. And still others said they were leery of any attempt by producers to control prices.

SMU’s Steel Buyers’ Sentiment Indices both rose this week.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Historical survey results are also available under that selection. If you need help accessing the survey results, or if […]

To ease trade tensions with the United States, the economy ministry in Mexico is preparing measures to strengthen definitions on steel being shipped into the country. Mexico has faced accusations it is being used as a route for steel and aluminum produced in Asia to be sent on to the US, so-called triangulation.

The market appears to be taking a pause after the heavy buying that occurred in March.

Steel buyers said mills are more willing to talk price on spot orders on all the products SMU covers, according to our most recent survey data.

Steel prices continued to ease lower in early March – a trend seen since mid-January – before showing signs of bottoming and inflecting up. The SMU Price Momentum Indicator for sheet products shifted from lower to neutral mid-way through the month after Nucor, Cleveland-Cliffs, and ArcelorMittal all targeted new base minimums between $825-840 per short […]

The spread between hot-rolled coil (HRC) and prime scrap prices has widened this month after narrowing for three months, according to SMU’s most recent pricing data.

The apparent supply of steel in the US fell 6% from January to February, according to data compiled from the Department of Commerce and the American Iron and Steel Institute (AISI).

Global steel demand will reach roughly 1.793 million metric tons (1.976 million short tons) this year, an increase of 1.7% over 2023, the World Steel Association (worldsteel) said in its updated Short Range Outlook report. The gain will come after a 0.5% contraction in steel demand in 2023. Demand is forecasted to increase another 1.2% […]

The Dodge Momentum Index (DMI) fell again in March, marking one of the lowest index readings of the past two years according to Dodge Construction Network data released Friday.

Directors of Swedish steelmaker SSAB have decided to replace blast furnace-based steelmaking at Lulea with a ‘green steel’ mini-mill process.

The US Department of Energy has finalized Congressionally mandated energy-efficiency standards for transformers.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

Sheet prices moved higher this week for the second consecutive week, while plate prices ticked lower, according to our latest canvas of the steel market.

US construction spending in February was mostly steady from January but showed significant gains from last year.

Following 16 months of contraction, US manufacturing activity expanded in March according to the latest report from the Institute for Supply Management (ISM).

The Chicago Business Barometer slipped to a 10-month low in March, according to Market News International (MNI) and the Institute for Supply Management (ISM). The March Purchasing Managers Index (PMI) reading eased 2.6 points to 41.4, marking the fourth consecutive month it has been in contracting territory.

After stabilizing in our last check of the market, production times for flat-rolled steel have begun to push out further, according to steel buyers responding to SMU's market survey this week.

Steel buyers report that mills are less willing to talk price on new sheet orders than they were in weeks past, according to our most recent survey data. In contrast, mills’ willingness to negotiate on plate products remains relatively high, now at the second-highest rate of the year.

SMU’s Current Steel Buyers’ Sentiment Index fell further week, now at the lowest reading recorded since October 2022

Steel companies in Mexico have lined up capex plans totaling $5.7 billion in the next three years. The focus is on replacing imports with domestic production, said David Gutierrez, outgoing president of sector association Canacero. “The investments are aimed at reducing imports, strengthening national production, and ensuring that the benefits stay in the country,” he was quoted as saying at Canacero’s annual congress by regional news service Business News Americas.

After reaching a seven-month high in January, steel imports fell back 3% in February, according to preliminary Census data released earlier this week.