Market Data

April 11, 2024

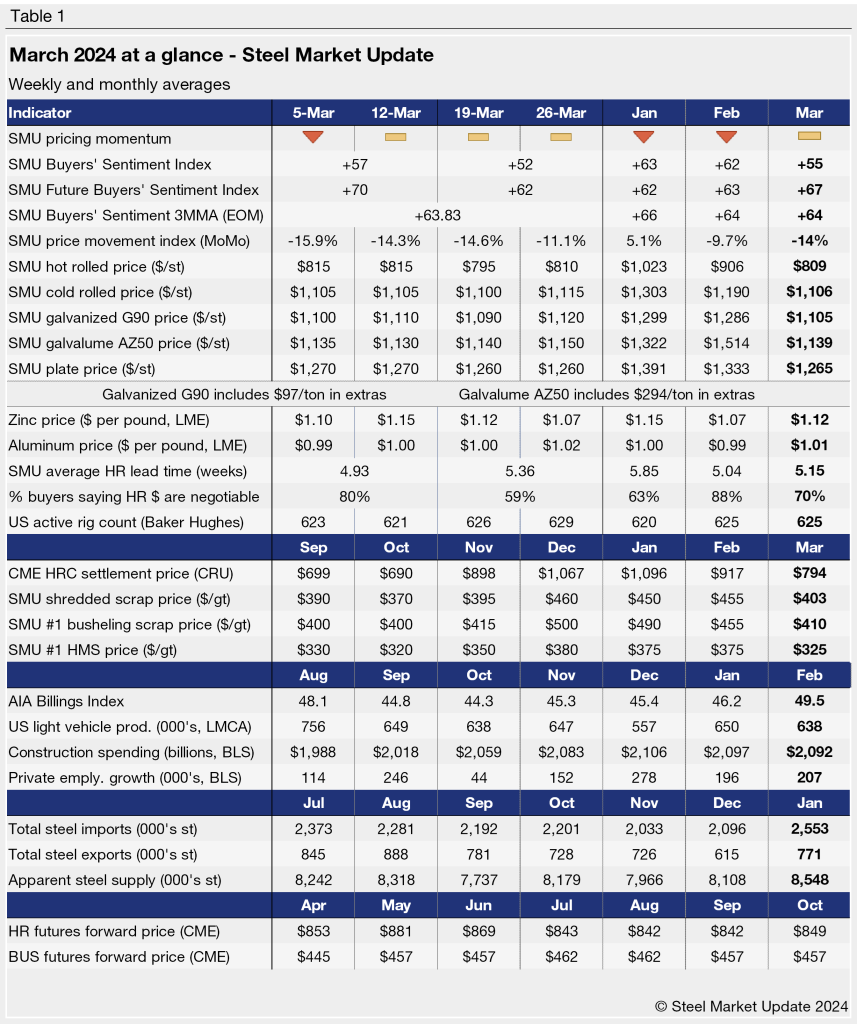

SMU's March at a glance

Written by David Schollaert

Steel prices continued to ease lower in early March – a trend seen since mid-January – before showing signs of bottoming and inflecting up.

The SMU Price Momentum Indicator for sheet products shifted from lower to neutral mid-way through the month after Nucor, Cleveland-Cliffs, and ArcelorMittal all targeted new base minimums between $825-840 per short ton (st) during the first week of March.

Like sheet, the Price Momentum Indicator on plate shifted from lower to neutral in March, though not until the last week of the month.

We saw hot-rolled coil (HRC) tags start the month around $815/st. They edged down $20/st by March 19 before moving back up to $810/st to close out the month. Tandem products saw similar dynamics play out during the month, while plate prices were largely stable, easing just $10/st over the second half of March.

Raw material prices were stable to down across the month. Busheling scrap prices declined for a third consecutive month, slipping $45/gross ton from February. Shredded and HMS scrap prices were also down similarly. You can read our recent outlook on the April scrap market here. LME zinc and aluminum spot prices were largely flat, edging up halfway through the month before ticking back down. You can view and chart multiple products in greater detail using our Interactive Pricing Tool.

The SMU Steel Buyers’ Sentiment Index remained positive but fell to a 17-month low at the end of the month. Future Buyers’ Sentiment followed the same trend, slipping back down after shooting up to a near-six-month high the month prior.

Hot rolled lead times averaged five weeks in March, ticking up slightly throughout the month. Lead times for each product we track neared lows last seen in September of last year before turning upward slightly to close out March. SMU expects lead times to remain largely in a holding pattern in April due to flat demand. A history of HRC lead times can be found in our Interactive Pricing Tool as well.

About 70% of HRC buyers reported that mills were willing to negotiate on prices through late March. Buyers have reported mills’ willingness to negotiate declined following new pricing targets by most mills.

Key indicators of steel demand continue to show some signs of weakness overall, with most nowhere near the bullish levels seen in recent years.

See the chart below for other key metrics for March: