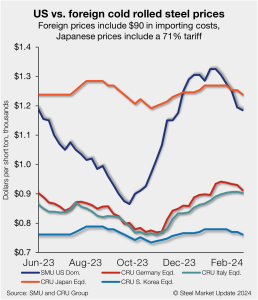

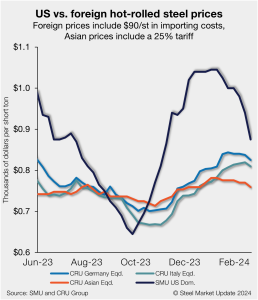

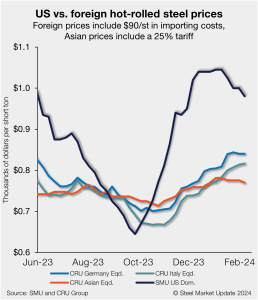

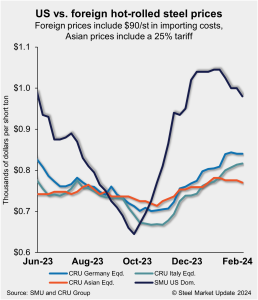

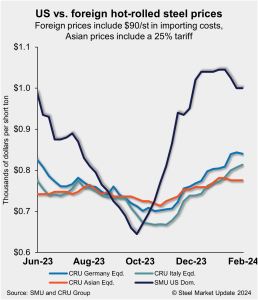

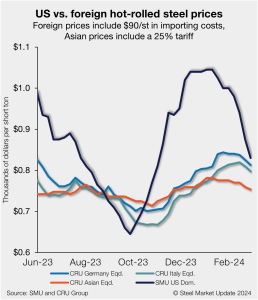

US HRC is just $42/st more expensive than imports

The premium US hot-rolled coil (HRC) held over offshore product for roughly five months has nearly vanished. Domestic hot band prices continue to run downhill at a high rate, erasing a $300/st gap they had over imported HRC just two months ago.