Market Segment

August 24, 2023

HRC Futures: Decline Logged in Uncertain Physical Market

Written by Daniel Doderer & John Medich

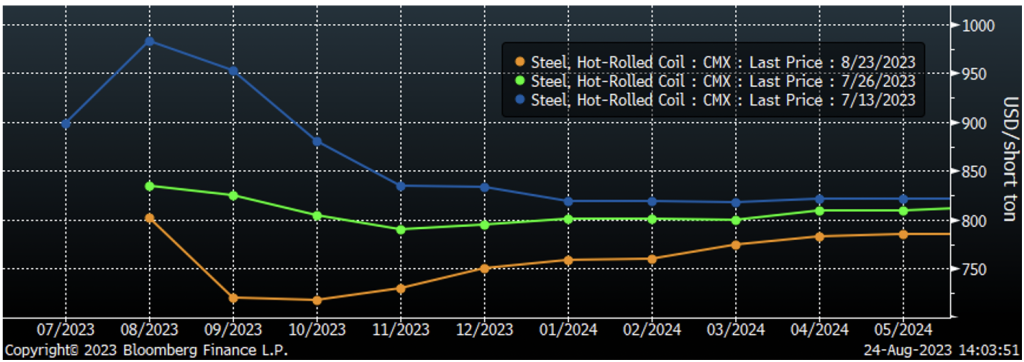

Over the first three months since Flack started contributing a futures column to SMU, the first sentence has started with some version of “What a month!” However, over the past month, the US HRC futures market has witnessed a clear and consistent trajectory. From July 13 to Aug. 3, the front of the HRC futures curve fell over 20%, a downward movement that has continued with momentum this week during the SMU Steel Summit conference in Atlanta.

This decline is primarily attributed to an uncertain physical market, with the market indicating expectations of further decreases into the fourth quarter of 2023. While volume and open interest have remained steady, aligning with levels seen throughout the latter part of 2022, the price trend reflects a gradual decline reminiscent of the previous year.

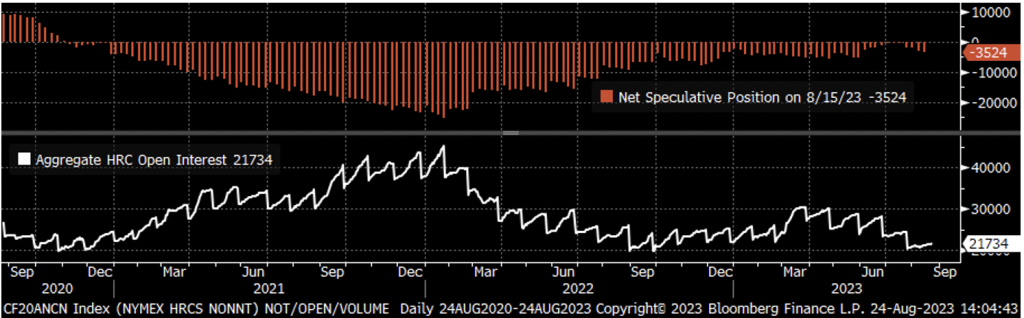

Open interest, while slightly depressed compared to recent highs, remains robust, and the five-year trend, a signal of increased activity, continues to reach higher highs – adding a layer of stability to the market despite the downward movement. Notably, recent CFTC filings reveal strategic shifts made by speculative money managers. Speculators have closed long positions and increased shorts over the past month, further contributing to the ongoing downward momentum.

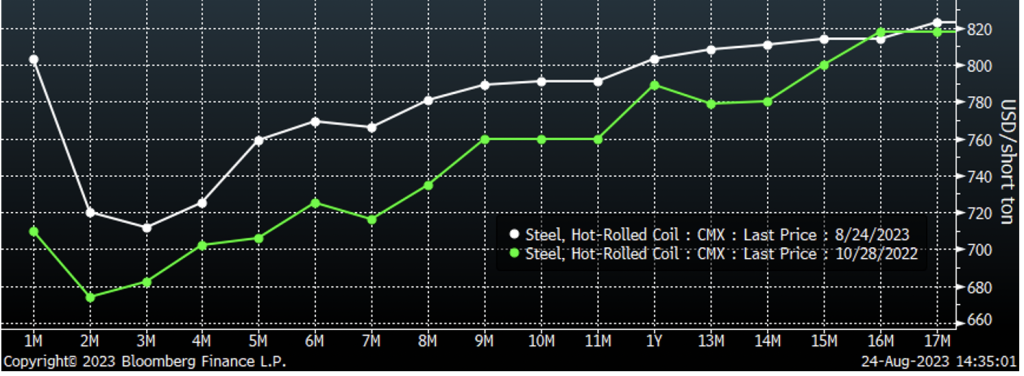

As we look at the calendar, it’s important to keep in mind that we’re approaching the contract season. During this time, many participants in the physical market, who use hedging to manage risk, will be locking in prices on the curve. This coincides with the signing of their supply agreements. With that in mind, it is interesting that despite the evident front-end price decline, futures prices for 2024 have demonstrated resilience, maintaining a tight range around $800. This has led the market into contango, remarkably like the curve at the end of 2022, where longer-term prices present a notable increase from the front of the futures curve. The chart below shows today’s settled curve vs. the curve on 10/28/22 in green.

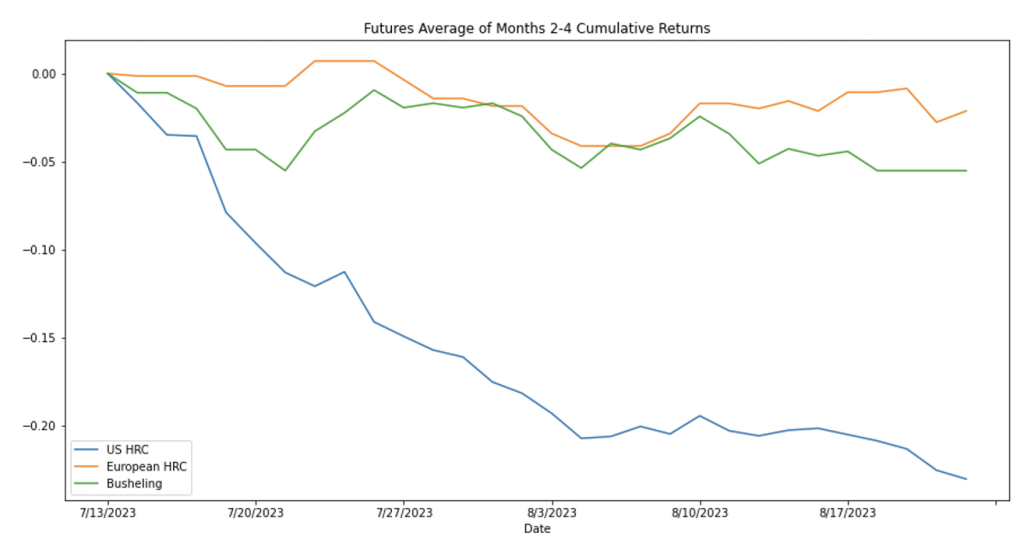

This is largely influenced by higher interest rates driving higher costs to carry inventory. However, it should also be noted that upside risks in related markets are starting to emerge. Examining historical trends, the ferrous complex typically exhibits interconnected dynamics. An intriguing deviation has emerged between HRC futures prices and closely associated European HRC and US Busheling Scrap futures (below).

The decline in US HRC prices highlights the significant impact of fundamental factors, notably the looming threat of auto strikes and the ongoing contraction in manufacturing demand. Looking ahead, a pivotal question arises: What does the near-term of the forward curve already reflect in terms of market expectations, and what are the potential risks on both sides?

Following participation in discussions at the SMU Steel Summit, a prevailing consensus among analysts and attendees suggests that spot prices are likely to continue slipping and could possibly maintain a tight range in the foreseeable future. However, it’s important to exercise caution when considering this as the baseline scenario, given the price volatility over the past three years.

As it currently stands, lead times continue to exhibit unexpected stability despite the rapid decline in prices. This observation strongly implies that buyers lack the necessary inventories to effectively wait out the impending maintenance outages, which are set to diminish available supply until the start of November. Regardless of whether UAW strikes, not all mills are going to be impacted in the same way and today’s spot pricing is already bumping up against some cost support levels.

Furthermore, it’s worth noting that although preliminary, positive signs are emerging in the manufacturing sector. The standout indicator is the Philly Fed Manufacturing Index, historically closely aligned with the ISM Manufacturing PMI. This index has exceeded expectations, solidly marking expansion for the first time since September of last year.

Finally, it’s crucial to acknowledge the presence of downside risks. The unexpected and remarkable economic growth observed in the US, reflected by Quarterly GDP figures of 2% in Q1 and 2.4% in Q2, has been primarily driven by service-side consumption, not manufacturing.

Considering that manufacturing has been undergoing contraction, the potential impact of higher interest rates should not be overlooked. Additional hikes by the Federal Reserve can introduce more restrictive economic conditions, which may further challenge the manufacturing sector. This, in turn, can impose a considerable headwind on steel consumption, potentially imposing a ceiling on any market rally.

Given the confluence of these risks, we strongly recommend implementing hedging strategies to navigate the complexities ahead.

About Flack Global Metals

In 2010, Flack Global Metals (FGM) was founded with the mission to reinvent how metal is bought and sold. Over 13 years later, the company has evolved into a hybrid organization combining an innovative domestic flat-rolled metals distributor and supply chain manager, a hedging and risk management group supported by the most sophisticated ferrous trading desk in the industry known as Flack Metal Bank (FMB), and an investment platform focused on steel-consuming OEMs called Flack Manufacturing Investments (FMI). Together, these entities deliver certainty and provide optionality to control commodity price risk in the volatile steel industry.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Metal Bank should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

Daniel Doderer

Read more from Daniel Doderer