Primetals to replace two EAFs at US mill

Primetals Technologies will be replacing two electric-arc furnaces at a steel mill in the US with one more energy-efficient furnace.

Primetals Technologies will be replacing two electric-arc furnaces at a steel mill in the US with one more energy-efficient furnace.

Following months of fluctuations, SMU’s Steel Buyers’ Sentiment Indices rebounded this week, now at multi-month highs. Both of our Indices remain in positive territory and indicate that steel buyers are optimistic about the success of their businesses.

It’s once again A Tale of Two Cities in the steel market. Some are almost euphoric about Trump’s victory. Others, some rather bearish, are more focused on the day-to-day market between now and Inauguration Day on Jan. 20.

After experiencing a rally ahead of the 2024 election, the nearby part of CME HRC futures complex has softened as we approach year-end. Meanwhile, the forward positions (second half of 2025) have remained supported and largely unchanged.

Steel buyers participating in our market survey this week reported stable mill lead times for both sheet and plate steel products.

Most steel buyers SMU polled this week reported that mills remain willing to negotiate new order pricing.

With climbing imports and falling consumption, the Latin American steel industry has had a challenging 2024, according to an Alacero report.

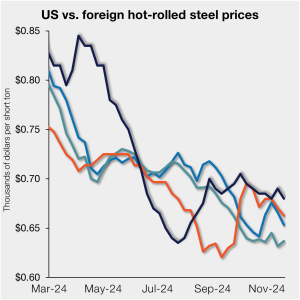

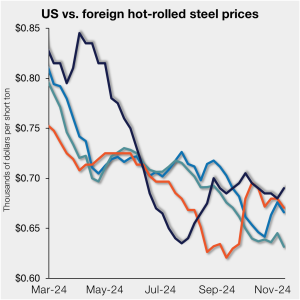

US hot-rolled (HR) coil prices slipped this week, while tags in offshore markets were also largely down. Thus, the price premium between stateside hot band and imports on a landed basis was relatively unchanged.

Architecture firms reported stable billings in October, according to the latest Architecture Billings Index (ABI) released by the American Institute of Architects (AIA) and Deltek. This follows 20 months of contracting business conditions.

Now that the dust has settled from the US election, as have the immediate reactions in the equity, bond, and commodity markets, this is a prime opportunity to look at how a second Trump presidency might affect the US steel market.

One of the perhaps unintentional perks of being a trade journalist is the opportunity to travel and cover an array of industry conferences and events. Some I've attended have been at fun locations, like Palm Springs and Tampa, Fla. Others have been in more practical locations, like SMU’s Steel Summit in Atlanta and American Iron and Steel Institute (AISI) and Steel Manufacturers Association (SMA) meetings in Washington, D.C.

SMU’s flat-rolled steel prices were mixed this week with slight declines across most products and a modest increase in prices for cold-rolled coil.

President-elect Donald Trump has named Wall Street veteran Howard Lutnick as the new US Secretary of Commerce.

Brazilian miner Vale SA has entered into a Memorandum of Understanding (MoU) with Australia-based Cyclone Metals Ltd. to develop the Iron Bear iron ore project in Eastern Canada.

China is one of the elephants in the room as the transition to Trump 2.0 continues. While the people and policies are still being formulated, it’s possible to detect a strategy for the new Trump administration. I think there are two imperative issues that the new administration needs to balance. The Trump strategy will, I believe, follow the following points. First, trade is one of the issues that got President Trump elected in 2016 and 2024—it nearly got him elected in 2020, save for the pandemic. If President Trump had won in 2020, I might be writing chronicles about the end of his eight years in the White House now instead of projecting what the next Trump administration would accomplish or break. Oh, well—that’s life. Trade will necessarily be a key feature of relations with China for the next four years.

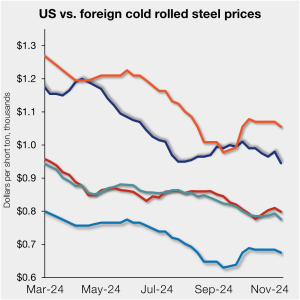

The price spread between US-produced cold-rolled (CR) coil and offshore products slipped in the week ended Nov. 15, on a landed basis.

North American auto assemblies rallied in October, rising 11.3% above September, reaching the best output year to date. Assemblies were also up 7% year on-year (y/y), according to LMC Automotive data.

The number of active oil and gas rigs ticked lower in both the US and Canada last week, according to the latest data released from Baker Hughes.

This CRU analysis from discusses steel sheet prices, demand, and inventory levels around the globe this past week.

New York state’s manufacturing sector saw substantial recovery in November, according to the latest Empire State Manufacturing Survey from the Federal Reserve Bank of New York.

According to data from the US Bureau of Economic Analysis, US light-vehicle (LV) sales accelerated to an unadjusted 1.33 million units in October, a rise of 1.7% from September and 10.6% from a year ago.

No more excuses! The election is over. Donald Trump will be inaugurated on Monday January 20 with the Republican party in control of Congress. Now, it is time to get back to work!

The investment is aimed at growing Kloeckner’s automotive and industrial segment in the US and Mexico.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events. Rather than summarizing the comments we collected, we are sharing some of them in each buyer’s own words.

After failing to reach agreements with its creditors, Altos Hornos de México (AHMSA) has been formally declared bankrupt by a Mexican bankruptcy court.

US hot-rolled (HR) coil prices edged up this week, while tags in offshore markets moved lower. As a result, domestic tags pulled ahead of imports on a landed basis. Since becoming level with import prices in late August, stateside tags had been mostly stable, though they slowly drifted closer to parity over the past month. […]

President-elect Donald Trump will officially retake the White House on Jan. 20. I’ve been getting questions about how his administration’s policies might reshape the steel industry and domestic manufacturing. I covered the tumult and norm busting of Trump's first term: Section 232, Section 301, USMCA - and that's just on the trade policy side of things. It's safe to say that we'll have no shortage of news in 2025 when it comes to trade and tariffs.

Prices for sheet and plate products were mixed this week. While market participants have noted a post-election uptick in activity, most said that it was (so far) nothing to write home about.

At the request of domestic petitioners, the Commerce Department has postponed its deadline for making preliminary countervailing duty margin determinations in the coated steel trade case investigations.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on tomorrow’s SMU Community Chat. The webinar will be on Wednesday, Nov. 13, at 11 am ET. It’s free to attend. You can register here. Timna – who has coined Sheet Storm, Scrap Squeeze, and Galv Galore – is one of […]