Fed indicators show a stable manufacturing sector

The latest Federal Reserve data paints a healthy and stable manufacturing sector. Steel Market Update is pleased to share this Premium content with Executive members.

The latest Federal Reserve data paints a healthy and stable manufacturing sector. Steel Market Update is pleased to share this Premium content with Executive members.

SMU’s steel price indices were steady to higher this week. Each of our sheet indices crept upwards from last week, while our plate index was unchanged.

Steel Market Update’s Steel Demand Index ticked back seven points last week, falling further into contraction territory.

Flat rolled = 66.3 shipping days of supply Plate = 57.0 shipping days of supply Flat rolled Flat-rolled steel supply at US service centers grew further in August. The dynamic resulted from some Q3 restocking efforts at a perceived market bottom, met with shorter lead times and weaker demand. At the end of August, service […]

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Following significant recoveries in late August, SMU’s Steel Buyers’ Sentiment Indices tumbled this week.

Steel mill lead times shortened for both sheet and plate products this week, according to buyers responding to our latest market survey.

SMU’s steel price indices showed mixed signals for a second consecutive week. Our hot rolled, cold rolled, and plate price indices inched lower from last week, as the galvanized index held steady and Galvalume's ticked higher.

Following June’s slump, the amount of finished steel entering the US market partially rebounded in July, according to SMU’s analysis of data from the US Department of Commerce and the American Iron and Steel Institute (AISI).

SMU’s Monthly Review provides a summary of important steel market metrics for the previous month. Our August report includes data updated through August 30th.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.”

Current steel mill lead time averages are a few days longer than levels seen one month prior, but remain near historical lows for both sheet and plate products.

Both our Current and Future Indices are now up to multi-month highs, indicating continued optimism among steel buyers.

Steel buyers found mills slightly more willing to negotiate spot prices this week, according to our most recent survey data. Though this negotiation rate has ticked up vs. our previous market check, overall rates have been trending downward since July’s highs.

Steelmaking raw material prices have moved in differing directions across August, a change of pace from the declines seen in June and July, according to SMU’s latest analysis.

SMU’s Steel Buyers’ Sentiment Indices moved in differing directions this week. Both indices have generally trended downward across 2024, but continue to indicate optimism among steel buyers.

SMU's latest steel buyers market survey results are now available on our website. Here are some key points that we think are worth your time.

Three out of four of our market survey respondents report that steel mills are open to negotiating new order prices this week, a slight decline compared to our previous market check.

Steel buyers continue to report short mill lead times for both sheet and plate products, according to SMU's latest canvass of the market. Lead times for hot-rolled and plate products marginally increased from our late July survey, likely due to limited restocking in anticipation of upcoming mill outages for scheduled maintenance.

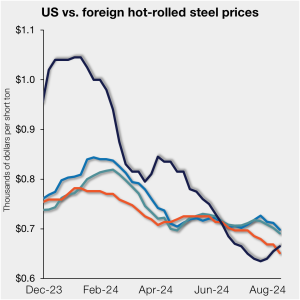

US hot-rolled (HR) coil prices are nearly even with prices for offshore material on a landed basis as domestic tags continue to inch up.

Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact info@steelmarketupdate.com. Flat rolled = 64.2 shipping days of supply Plate = 60.9 shipping days of supply Flat rolled Flat-rolled steel supply at US service centers grew in July with restocking as […]

SMU’s Monthly Review articles summarize important steel market metrics for the prior month. Our July report contains figures updated through July 31.

Following an uptick in mid-July, SMU’s Steel Buyers’ Sentiment Indices both eased this week. Current Buyers Sentiment has been see-sawing for the past few months, now back down to one of the lowest readings recorded since August 2020.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Historical survey results are also available under that selection. If you need help accessing the survey results, or if your […]

Buyers continue to report very short mill lead times on sheet and plate products, according to our latest market canvass of steel service center and manufacturer executives

Steel buyers of sheet products say mills are still flexible on spot pricing this week, though less so than two weeks prior, according to our most recent survey data.

The majority of steelmaking raw material prices declined in June, following the same trend seen in May, according to SMU’s latest analysis.

SMU’s sheet price ranges slid again this week. But the declines were more pronounced on tandem products whereas prices for hot-rolled coil held roughly steady.

SMU’s Key Market Indicators include data on the economy, raw materials, manufacturing, construction, and steel sheet and long products. They offer a snapshot of current sentiment and the near-term expected trajectory of the economy. All told, nine key indicators point lower, 16 are neutral, and 13 point higher. One thing worth noting: The nine indicators pointing lower are all lagging indicators. Many of those pointing upward are leading indicators.

SMU’s Steel Buyers’ Sentiment Indices both saw improvement this week. Current sentiment ticked higher but remains near the four-year low seen earlier this month. Future Sentiment continues to indicate that buyers are optimistic for future business conditions.