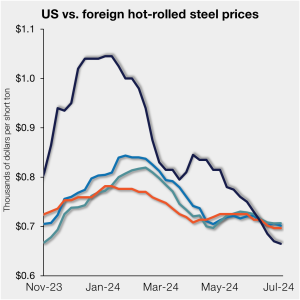

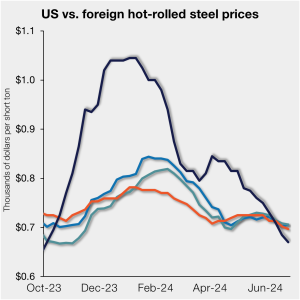

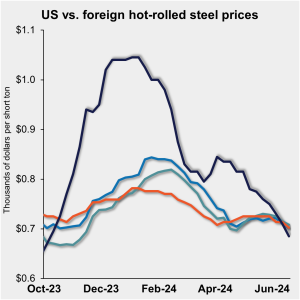

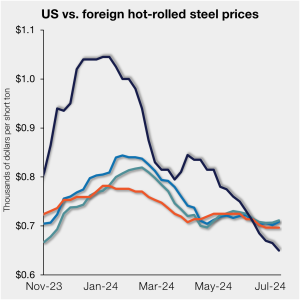

Sliding US HRC prices fall further below imports

US hot-rolled (HR) coil prices continued to drift lower this week, falling further below imported hot band tags on a landed basis. SMU’s check of the market on Tuesday, July 9, put domestic HR coil tags at $650 per short ton (st) on average, down $15/st vs. last week. Domestic HR coil prices are now […]