Analysis

May 5, 2024

Final thoughts

Written by Michael Cowden

Is it just me, or does it seem like the summer doldrums might have arrived a little early?

I could be wrong there. It’s possible we could see a jump in prices should buyers need to step back into the market to restock. I’ll be curious to see what service center inventories are when we update those figures on May 15.

In the meantime, just about everyone we survey thinks HR prices have peaked or soon will. (See slide 17 in the April 26 survey.) Lead times have flattened out. And some of you tell me that you’re starting to see signs of them pulling back. (We’ll know more when we update our lead time data on Thursday.)

I don’t want to draw any overly broad conclusions from that. If lead times slip, it might say less about demand and more about a trend of spring maintenance outages wrapping up.

Recall it was those outages (and an anticipated supply squeeze) that many thought would lift prices higher. We did see prices rise $50 per short ton (st) on average between mid-March and early April, according to SMU’s pricing tool.

That fell short of the price spike many anticipated. And, all else equal, I don’t see how that capacity coming back doesn’t mean more supply and some pressure on prices – at least on the margins if the spot market remains quiet.

Another factor: Imports remained high in April. A few of you told me you had expected that. Basically, some material slated to land in Q1 had been delayed because of issues on the Panama Canal and elsewhere. So no need to get too worked up about it.

Will imports be high in May be high as well? It’s hard to draw any conclusions until we have a few weeks of license data. But here is some food for thought in the meantime. The gap between foreign and domestic HR has narrowed. But US mills continue to command a roughly $300/st premium for CR/coated. That has left the spread between US CR/coated prices and those abroad very wide. How does that not leave room for continued import competition?

All of that is a bit macro. Turning back to the micro, I think I might have touched a nerve when I wrote that the economy couldn’t be all that bad if Vegas was packed in the middle of the week during the annual ISRI/ReMA conference.

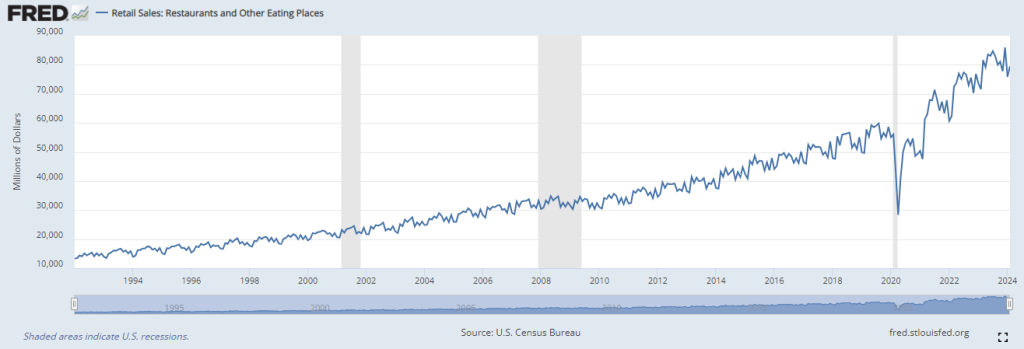

It really was hard to find a table at times. (Champagne problem, I know.) In my defense, restaurant spending is about as high as it’s ever been, according to figures compiled by the Federal Reserve Bank of St. Louis.

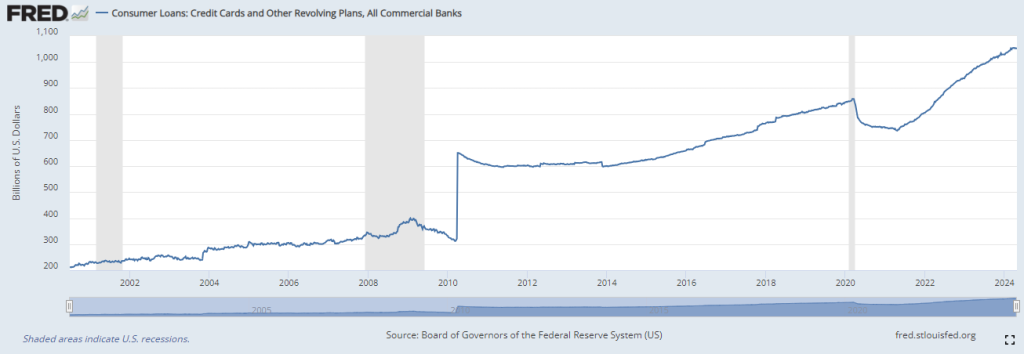

But, as some of you have pointed out, one flipside of that might be this: Consumer credit card debt is also about as high as it’s ever been, per the St. Louis Fed.

And while bigger companies might be doing just fine, some of you with smaller businesses tell me it’s getting more and more difficult out there. Prices have been volatile. Wages are higher. Borrowing costs are up. It seems to me like the hope is that things will, sooner rather than later, get back to something resembling normal.

Some of you also suggested that Nucor had “undercut” Cleveland-Cliffs by announcing an HR price of $825 per short ton (st) last week just days after Cliffs had announced a target price HR of $850/st. Some predicted that prices might fall into the low $700s/st – and into the $600s/st once you take contract discounts into account.

Why do I bring that up now?

Remember what I’ll call the “before times” – before the pandemic, before Section 232 – when it was not uncommon in competitive markets for EAF mills to sell a little below integrated mills. It made sense. All else equal, their costs were lower. And they typically relied more on the spot market.

Maybe that price discrepancy isn’t a sign of a slowdown. It might just be a sign of normalcy returning (slowly) to US markets. I hope so. After four year of volatility, normal might be the new black.

Steel 101 on June 11-12 in Fort Wayne, Ind.

Looking for a good way to start the week? Are you a steel nerd like us? If the answer to either is ‘yes!’, then check out SMU’s first steel-themed crossword puzzle!

We’ll be bringing you a new one each week until our Steel 101 training course on June 11-12 in Fort Wayne, Ind. The class will also feature a tour SDI Butler. (A big ‘thank you’ to SDI for allowing us to visit.) You can learn more and register here.

PS: If you’ve already attended Steel 101, you’ll have a leg up on the competition when it comes to our crossword puzzles. The answers can be found in the glossary of the Steel 101 workbook.