Prices

October 10, 2019

Hot Rolled Futures: Activity Picking Up

Written by Gaurav Chhibbar

SMU contributor Gaurav Chhibbar is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Gaurav’s previous role, he was a trader at Cargill spending time in Metal and Freight markets in Singapore before moving to the U.S. You can learn more about Metal Edge at www.metaledgepartners.com. Gaurav can be reached at gaurav@metaledgepartners.com for queries/comments/questions.

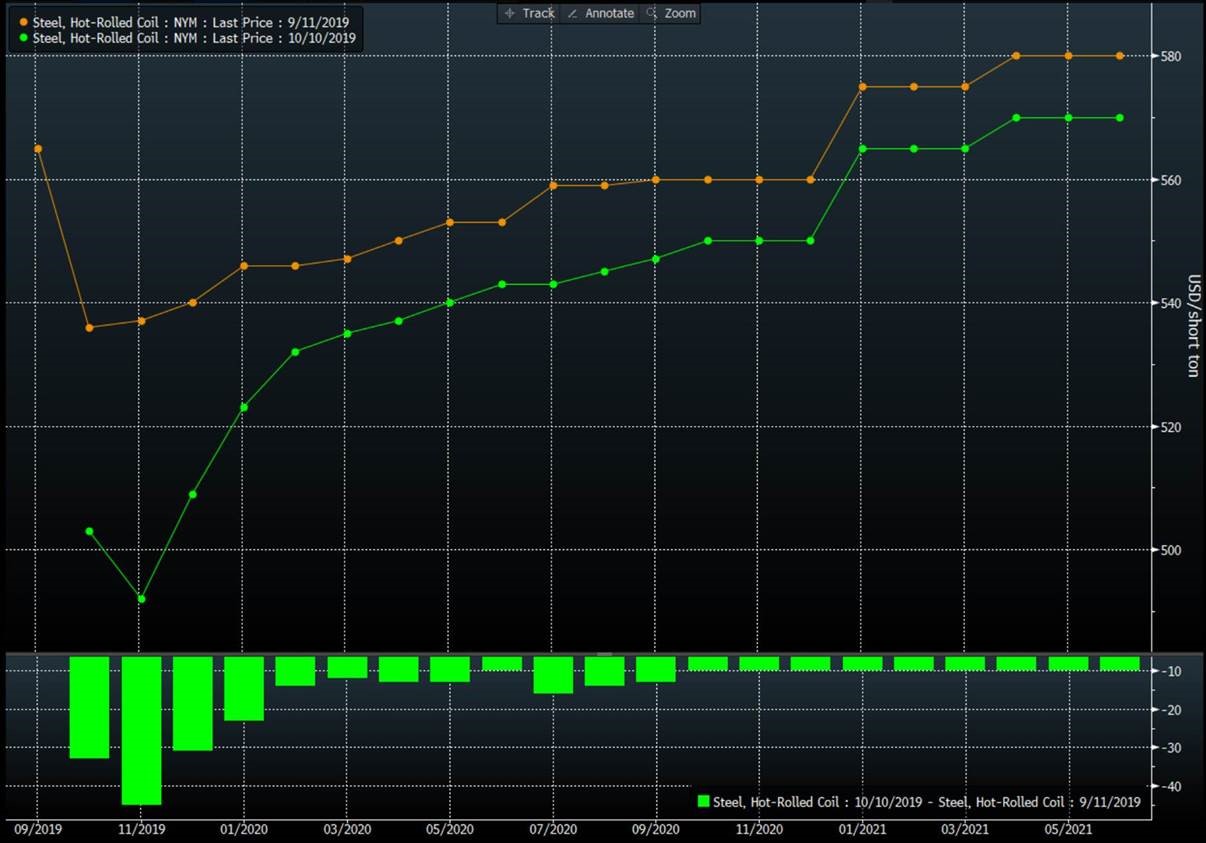

U.S. HRC futures are seeing some renewed buying interest. With the front of the curve falling from ~$540 to below $500, there is some level of short covering and index-deal locking that is driving the buying activity. In addition, with the curve steepening over the course of the last few days, there are opportunities for discount physical steel buyers to lay off some of that risk by selling the deferred months. While nearby fundamentals continue to be weak—short lead times, weak order books, buyers’ reticence to book tonnage—the market seems to be pricing an improvement in conditions further out into Q4 or early Q1. December futures are about $10 higher than Nov’19, while January is about $25 higher.

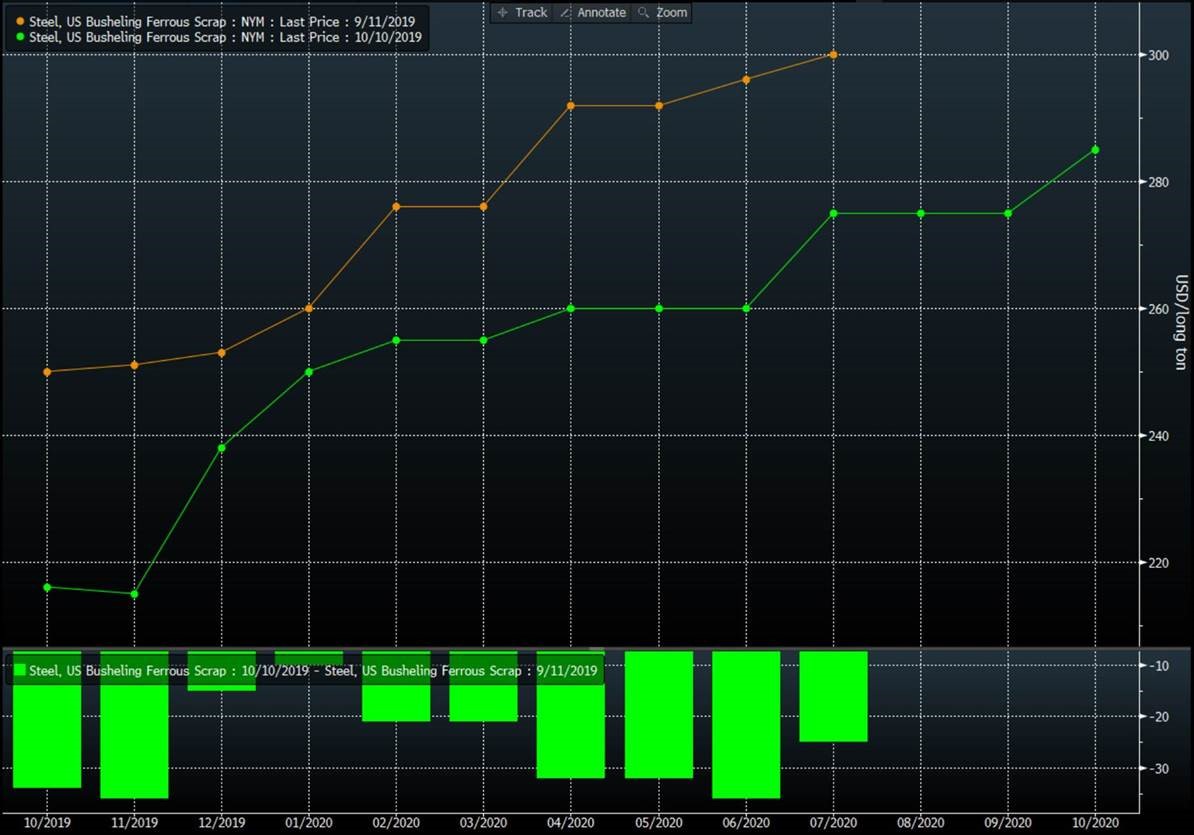

The shape of the HRC curve is not very different than what you see in Busheling Scrap futures. The Jan’20 premium over Nov’19 is $35. With scrap prices having fallen rapidly over the last 60 days, it is easy to understand why Nov’19 is at such a discount. However, for minimills as well as buyers who procure steel based on scrap prices, it may be worthwhile to look at buying scrap futures to protect any margin compression against sales they are making at fixed prices for 2020. Increasing chatter around weaker flows into scrap yards has fueled interest among those looking to buy scrap. Some still contend that there is no reason to panic and that weak steel demand will force lower production (or lower scrap consumption) to balance the market. However, there is a growing camp of believers who feel apparent demand for HRC is on the verge of ramping up. They allude to low inventories as being a leading indicator for what might change the direction of the market.

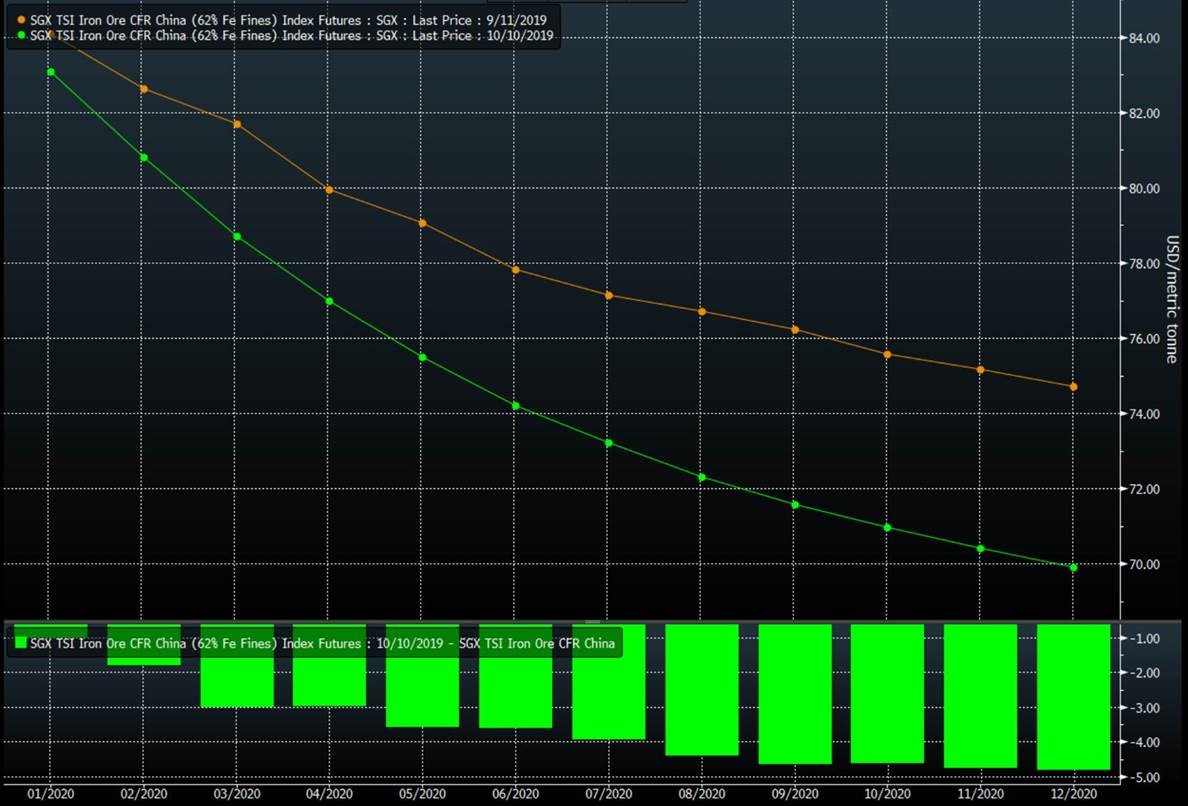

Internationally, ore has been quite sticky and continues to hold steady. As production cuts take effect in China, the mills turn towards buying higher grade ore. There are increasing signals that going into year 2020, ore demand will look worse than today (lower Chinese steel production). Compounded with fears of surplus ore supply, the ore curve tells the classic old tale of a market waiting to see a push lower. I’d caution those who think we are about to see a big, imminent decline by directing their attention to what quality mix changes for mills in China did to lump or pellet premiums in 2017-18.

Lastly, for those looking at the current market and wondering which way they should look to trade, I’d urge them to keep an eye out and monitor those long dated sales they are making without having either sufficient inventory or hedges in place. Good luck trading!

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information.