Prices

March 26, 2020

Hot Rolled Futures: Uncertain Times Pushing HR Futures Volatility Higher

Written by Jack Marshall

The following article on the hot rolled coil (HRC) steel and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Steel

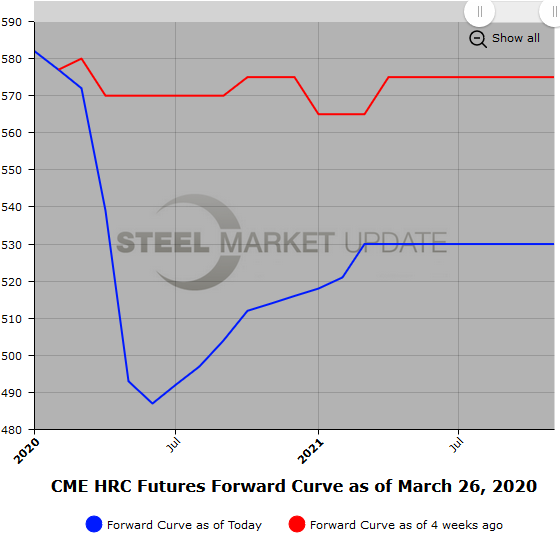

This month HR physical prices as reflected by the index basically started at $560/ST and rose $20-plus to hold, then fell back to $561/ST leaving the monthly average to rest at $572/ST. During the same period, the front 12 months of the HR futures curve gave up on average of roughly $65/ST — Q2’20, Q3’20 and Q4’20 all declined about $67/ST and Q1’21 declined $58/ST. As of last night, the Q2’20 was valued at $503/ST, Q3’20 was valued at $495/ST, Q4’20 was valued at $506/ST, and Q1’21 was valued at $513/ST. The curve reflects the expectation third-quarter results will be the most impacted by the spread of the COVID-19 virus. It should be noted that the futures market dipped even lower. On March 19, the average price of the front 12 months of the HR futures curve had declined from the beginning of March almost $81/ST.

So we have seen a number of hedge buyers come into the market to take advantage of the large discount to the current spot physical prices being reported. That buying has continued here this morning as the HR futures continue to tick higher. In spite of the uncertainty with regard to supply and demand of both HR and scrap, futures markets have been fairly robust with healthy volumes trading across most periods. Almost 490,000 ST of HR futures has traded this month with a few days posting close to record daily volumes.

HR participants will remain laser focused on any supply/demand news for further impacts as everyone watches the gamma in the rate of spread of the virus and tries to apply it to their operations. There have been a number of reported planned curtailments of HR production likely linked with a number of auto companies temporarily ramping down production to adjust for COVID-19 impacts, as well as the drop in tube demand due to lower oil prices. There remains a lot of uncertainty, which is reflected in the higher volatility in price movements in HR futures.

Below is a graph showing the history of the CME Group hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

Scrap

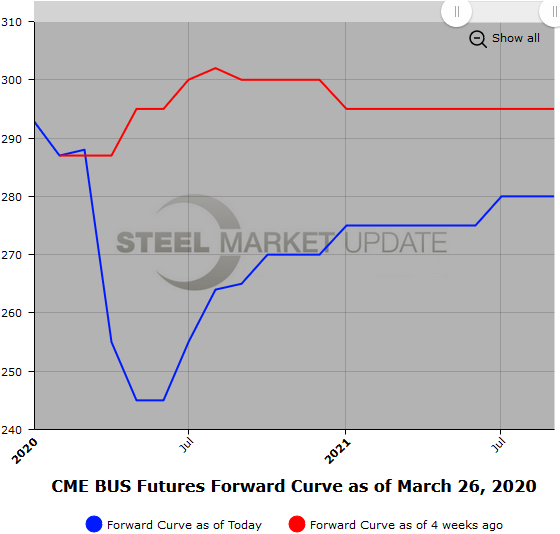

The BUS market is also dipping this month. While Mar’20 BUS settled at $297/GT, early chatter has Apr’20 BUS declining on the order of $50/GT. This is likely due to some production adjustments in the near term. During March the front 12 months of the BUS futures curve declined on average roughly $28/GT — Q2’20 declined about $40/GT, Q3’20 and Q4’20 declined about $26/ST, and Q1’21 declined about $20/GT. As of last night the Q2’20 was valued at $254/GT, Q3’20 was valued at $265/GT, Q4’20 was valued at $270/GT, and Q1’21 was valued at $275/GT. With the drop due to the virus impacts, the front 12 months of the futures curve is in a $20 contango. At some point the production cutbacks will impact the supply and likely further push up the middle and back months in BUS. Reduced collections of some types of obsolete could also impact supply, which will likely leave the Shred futures in contango as well.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here.