Prices

February 25, 2021

Hot Rolled Futures: Paper Stuffin’

SMU contributor Bryan Tice is a partner at Metal Edge Partners, a firm engaged in risk management and strategic advisory. In this role, he and the firm design and execute risk management strategies for clients along with providing process and analytical support. Prior to Metal Edge Partners, Bryan held a variety of commercial leadership roles involving purchasing, sales and risk management for Feralloy Corporation, Cargill Steel Service Centers and Plateplus Inc. You can learn more about Metal Edge @ www.metaledgepartners.com. Bryan can be reached at Bryan@metaledgepartners.com for queries/comments/questions.

Nearly 28 years ago when I started my career in the steel business, much of the steel processing equipment lacked the technological advances seen in today’s modern processing lines. During my first several months of employment as a sales trainee in Detroit, I worked on the production floor learning the business from a “hands on” perspective. Back then it was common on slitting lines to stuff paper or cardboard in the outer mults of processed slit coil to compensate for the center to edge thickness variation and to ensure a tight wrap. I must admit, it was a little unnerving inserting small shims of cardboard by hand at the recoiler of a slitter running a few hundred feet per minute. Fortunately, technology and safety standards have evolved.

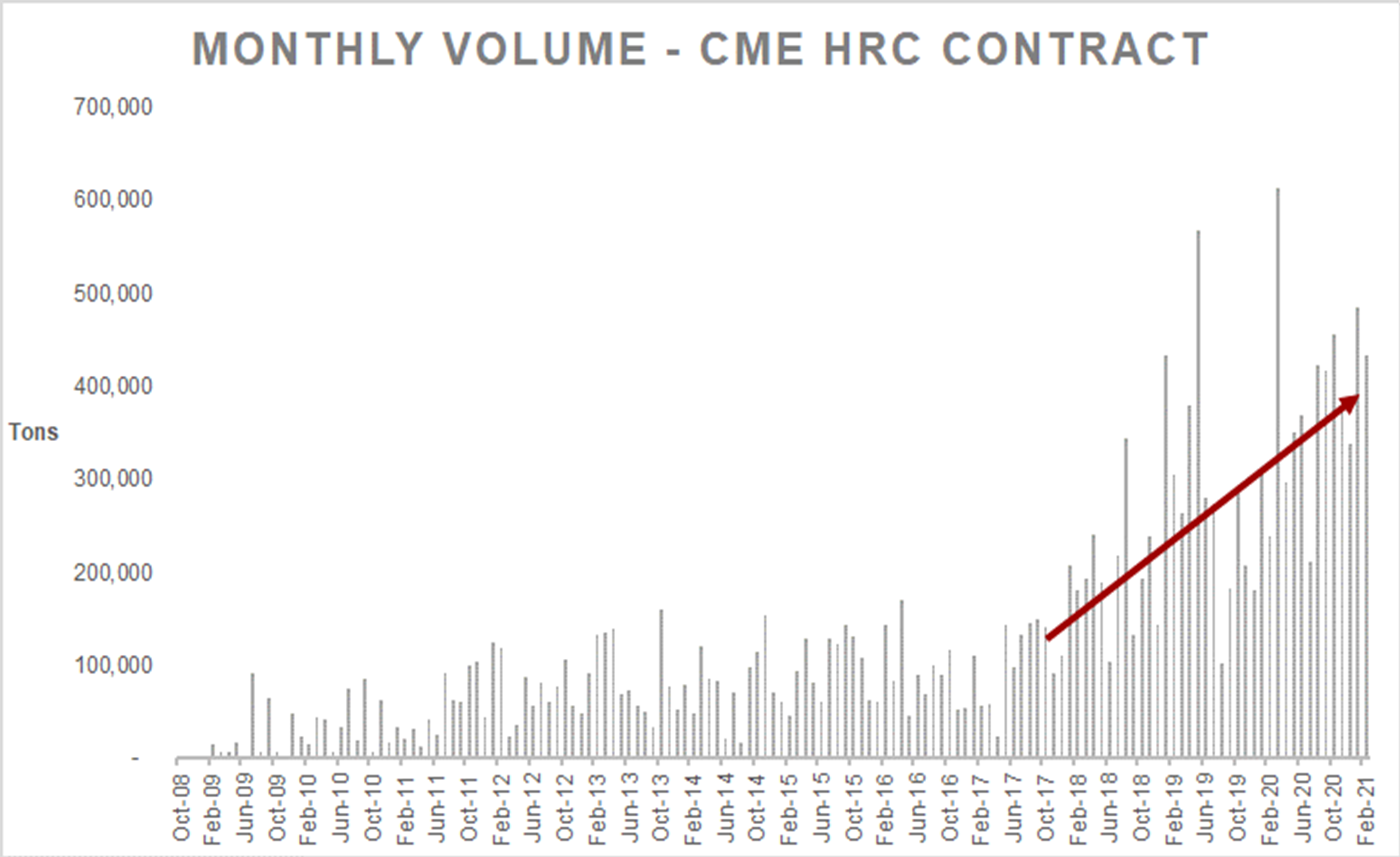

These days I work with a different sort of paper; steel derivative contracts, which are often referred to as “paper contracts.” Fortunately, these too have evolved. The market continues to see greater adoption of risk management tools as the chart below highlights.

With the increasing liquidity of steel and scrap derivatives, market participants have a wider array of tools available to mitigate steel price risk. As a steel buyer, you can lock in your steel costs for a period of time into the future, given you have a properly constructed floating price physical steel agreement. Take for example a steel buyer who, ahead of the Thanksgiving holiday last year, was worried about steel price escalation into the first quarter of 2021, chose to lock up a small part of her steel costs by buying HRC futures contracts. The below example is a snapshot of the settlements of the HRC futures curve on Nov. 20, extended with a hypothetical purchase of 50 lots equivalent to 1,000t in each month December through February, since the company has a monthly lagged index with a $40/t discount for their physical steel.

In the above example, the company was not immune to the dramatic rise in physical steel prices as those costs still flowed through and averaged $1,036/t (before hypothetical discount), but as you will see the gains of $798,000 on the derivative contracts offset their rising physical costs and allowed them to enjoy a $730/t cost for the 3,000t that was hedged.

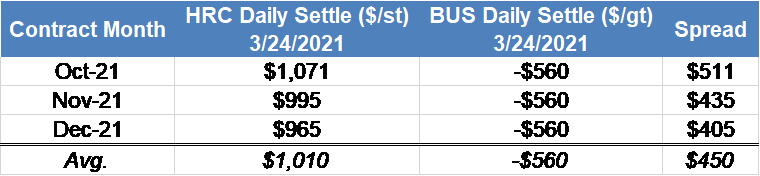

On the other hand, I think about new steel capacity scheduled to enter the market later this year and the potential opportunity for steel mills to lock in margins as HRC vs. scrap spreads are near all-time highs. Should a mill choose to buy a portion of their fourth-quarter 2021 scrap needs by purchasing busheling BUS futures at Wednesday’s settlement, and sell the HRC contract, they would have the opportunity to lock in a spread of nearly $450/t (before GT/NT conversion). Clearly these future spreads are lower than the current margins enjoyed by many of the EAF mills today, but could offer some historically favorable margins to protect against any future scrap price inflation/steel price deflation.

Today we sit in a much different and inherently more difficult environment with steel prices at all-time highs. Much of the fundamental analysis deployed to determine the magnitude of this historic rise in prices, such as the scrap to steel spreads, has been disproven. Many steel distribution executives may feel as if they are in some sort of steel purgatory as they fret about their ability to procure enough steel to deliver their companies to the promised land, while worrying about prices peeling back and sending them into the fiery abyss. I have pondered the recent WSJ article on Europe’s intention to double the tariffs on American whiskey imports into the EU to 50% on June 1 (which was implemented in retaliation of the steel/aluminum tariffs against European countries) and wonder if that puts the fate of Section 232 back on the front page. All these factors are likely to keep volatility at a fever pitch.

Trading steel derivatives is not without risk but does offer market participants an actionable tool to help accomplish a variety of goals, whether they are providing customers with longer dated fixed price solutions, fixing their future steel costs, locking in margins, or protecting their unsold inventory against a potential price correction.

As the HRC futures market continues to climb the wall of worry, many of you may share the same anxiety about where steel prices go from here. But depending on your market view or the risks you are looking to mitigate, stuffin’ some paper in your book may be worth considering. No safety glasses required!

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information