Prices

July 14, 2022

HRC and Bush Futures: Sleepy Summer Market Continues

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

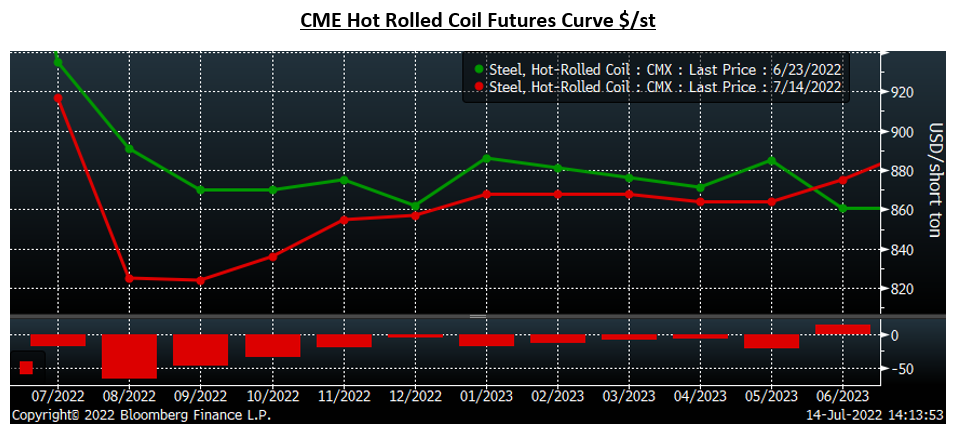

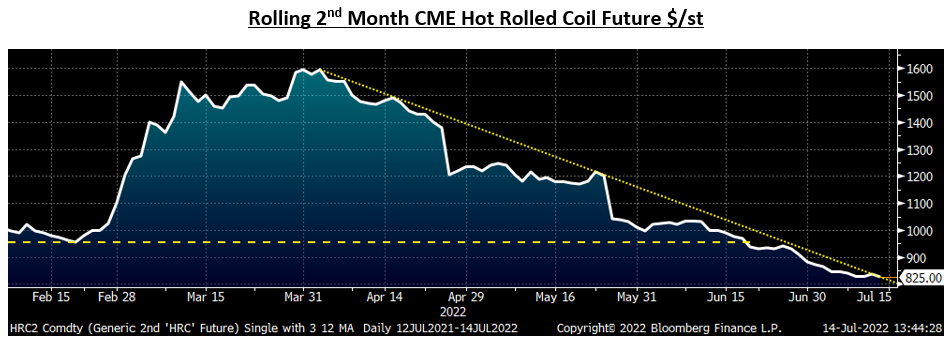

There is not much to report on since my last contribution on June 23. The August and September futures have declined by $66 per ton and $46 per ton during that time. But the rest of the curve has seen little change, especially relative to the declines seen since futures peaked in March and April. The August future peaked on March 15 at $1,639/ton and settled today at $825/ton, down $814/ton or 49.7%.

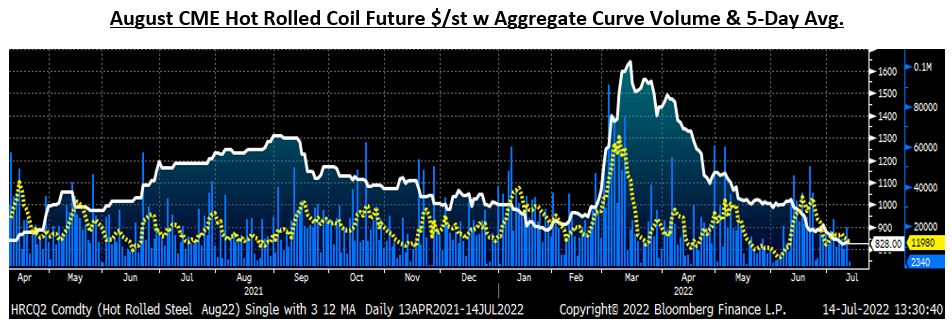

Volatility in HRC futures has cratered along with trading volume, which, after briefly picking up in mid-June, has fallen to a five-day average of 13,448 tons as of yesterday’s close.

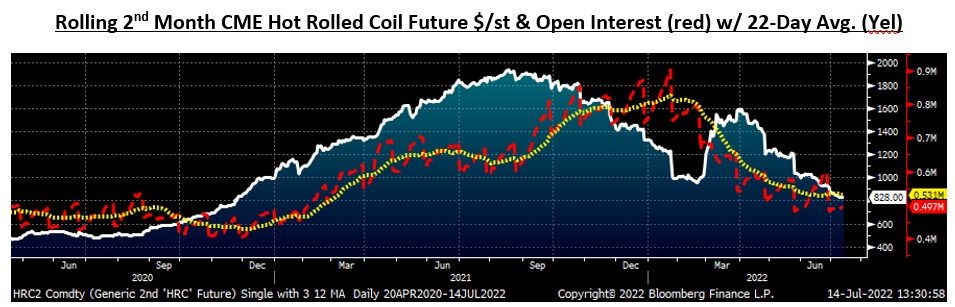

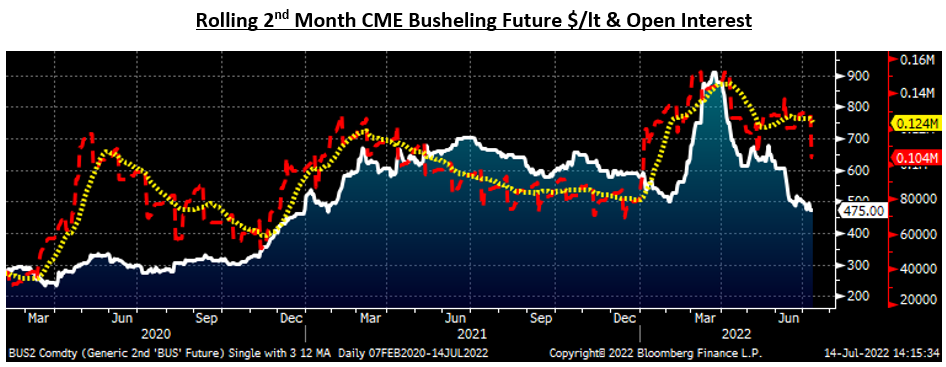

Open interest has flattened out around 530,000 tons since peaking just above 900,000 tons in January. Open interest is the number of outstanding futures contracts, or tons in this case.

The rolling 2nd month CME future, now August, broke below February’s $955 per ton low on June 16 and has continued lower since.

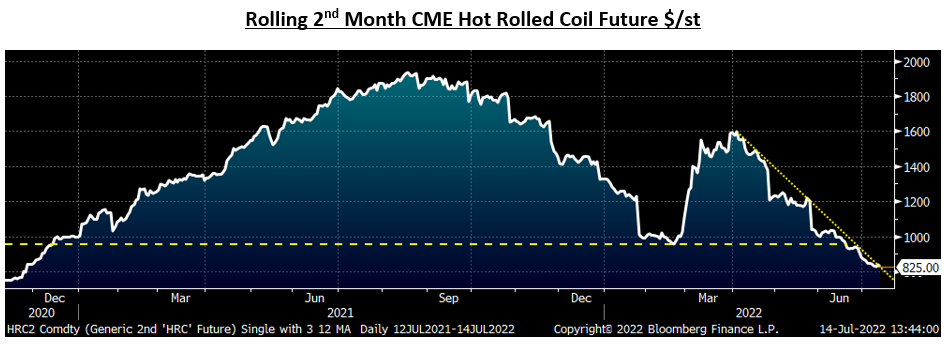

Taking a closer look at the chart, you will see the August future is currently touching the down trendline that started back in early April. Will the August future continue to decline or will it start to peek above its downtrend?

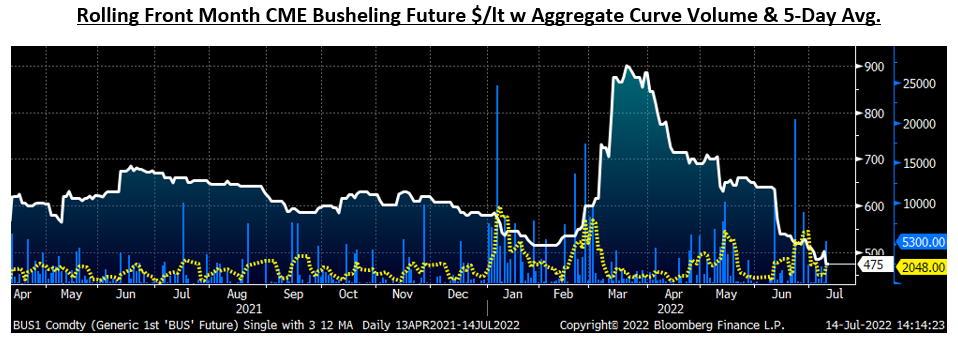

Fears of supply disruptions resulting from Russia’s full-scale invasion of Ukraine in February sent busheling futures prices briefly above $900 per long ton in March. Any disruption to busheling supply has since been resolved sending the month’s settlement sharply lower. The April busheling future settled at $778.65/long ton, the highest settlement on record, but well below $900/long ton. Earlier this week, the July future settled down $133.92/long ton MoM at $500.86/long ton with the August future pricing in another decline to come trading at $475/long ton, the lowest level since January 2021. Volume has fallen sharply as well with trading coming in fits and spurts, or as they say in the business “trading by appointment.” The five-day average daily volume has been oscillating between 1,000 to 2,500 tons per day in July.

Open interest across the busheling curve has also fallen following July’s expiration to 104,000 long tons, its lowest level post expiration since last December.

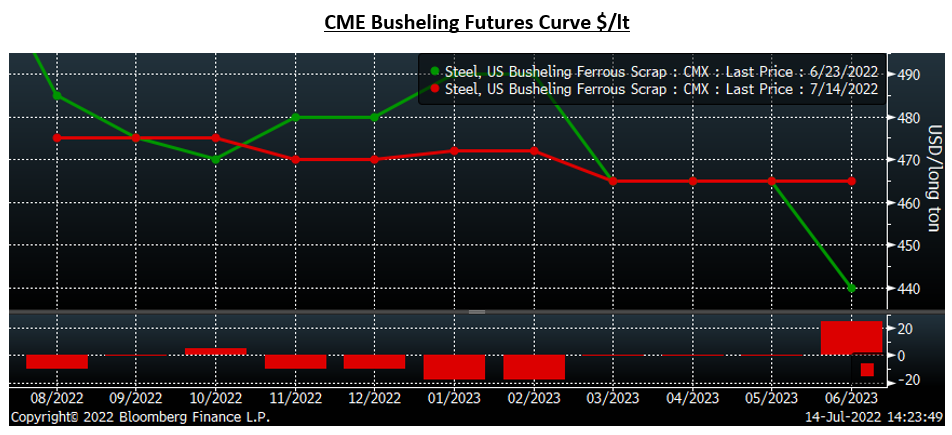

Since June 23, the busheling futures curve has seen little movement with no future up or down by more than $22 per long ton through next June.

Now seems like a great time to work on your tan, spend some time with the family or go to Europe and see Big Ben. Just keep one eye on the market of course as these ultra-low levels of volume and open interest mean relatively illiquidity and an environment that can quickly turn a sleepy summer market into a rip-roaring one in no time.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.