Market Data

January 8, 2023

Final Thoughts

Written by Michael Cowden

Higher prices rolled out by North American sheet mills are gaining traction downstream, according to our latest survey results.

Service centers report that they are raising prices to their customers. And manufacturers say they are seeing higher prices from their service center suppliers.

Both trends are more pronounced than what we saw in late August and early September, when mills announced a round of price hikes that mostly failed. But there are a few flies in the ointment.

Check out the charts below.

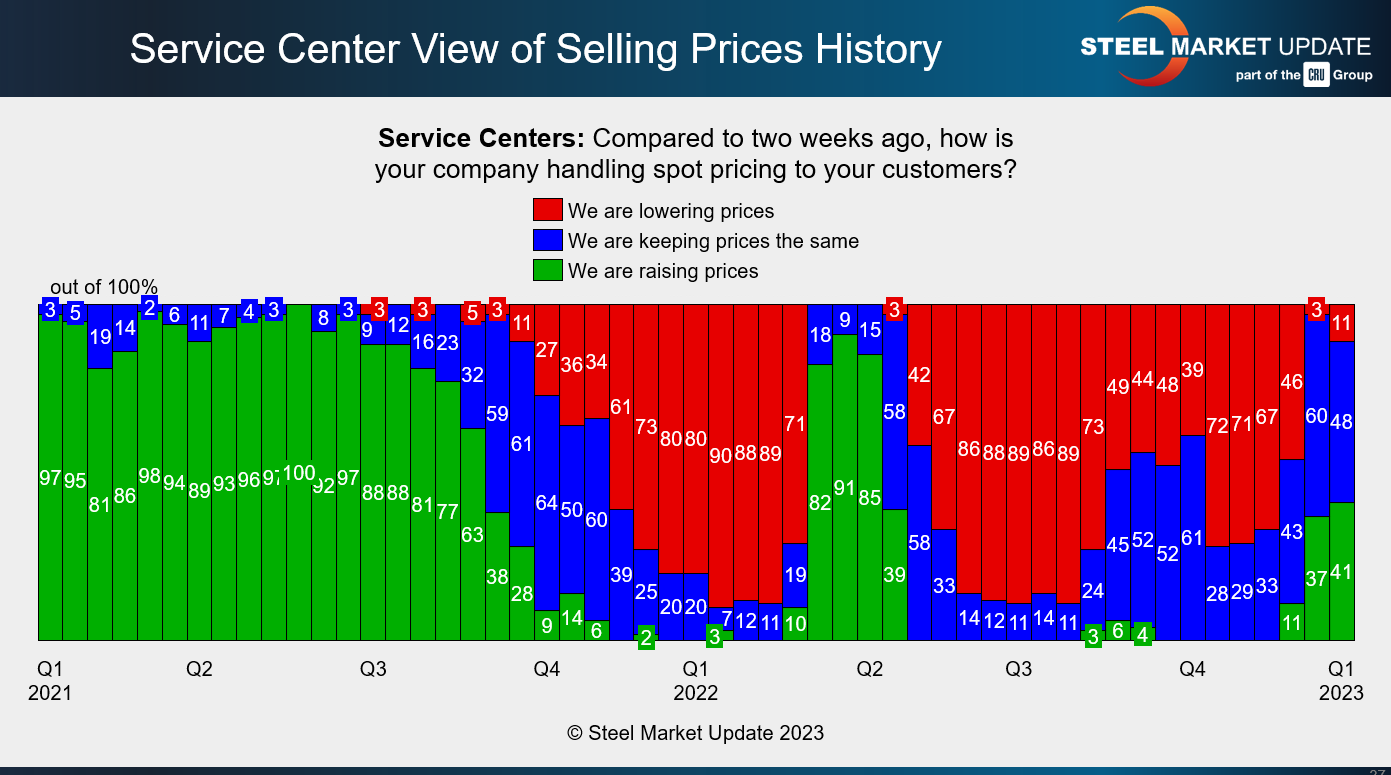

Let’s consider service centers first:

More than 40% of service center respondents say that they are raising prices to their customers, up modestly from our last survey. Nearly half say that they are keeping price unchanged. That’s the best reading we’ve seen since the price spike following the war in Ukraine. But this time, the uptrend was more modest and driven by more typical factors. Mills have announced price hikes of a combined $110 per ton ($5.50 per cwt) on sheet products since Thanksgiving. And they’ve gotten most of it. SMU’s HRC index stands at $695 per ton, up $80 per ton from $615 per ton before Thanksgiving.

What’s a little surprising – if you look in the upper right-hand corner – is that we’ve seen a slight increase in the number of service centers reporting that they’re lowering prices. It’s only 11%. It’s entirely possible that the uptick is just noise. But I’d suggest keeping a close eye on that one in our next market survey, results of which will be released on Friday, Jan. 20.

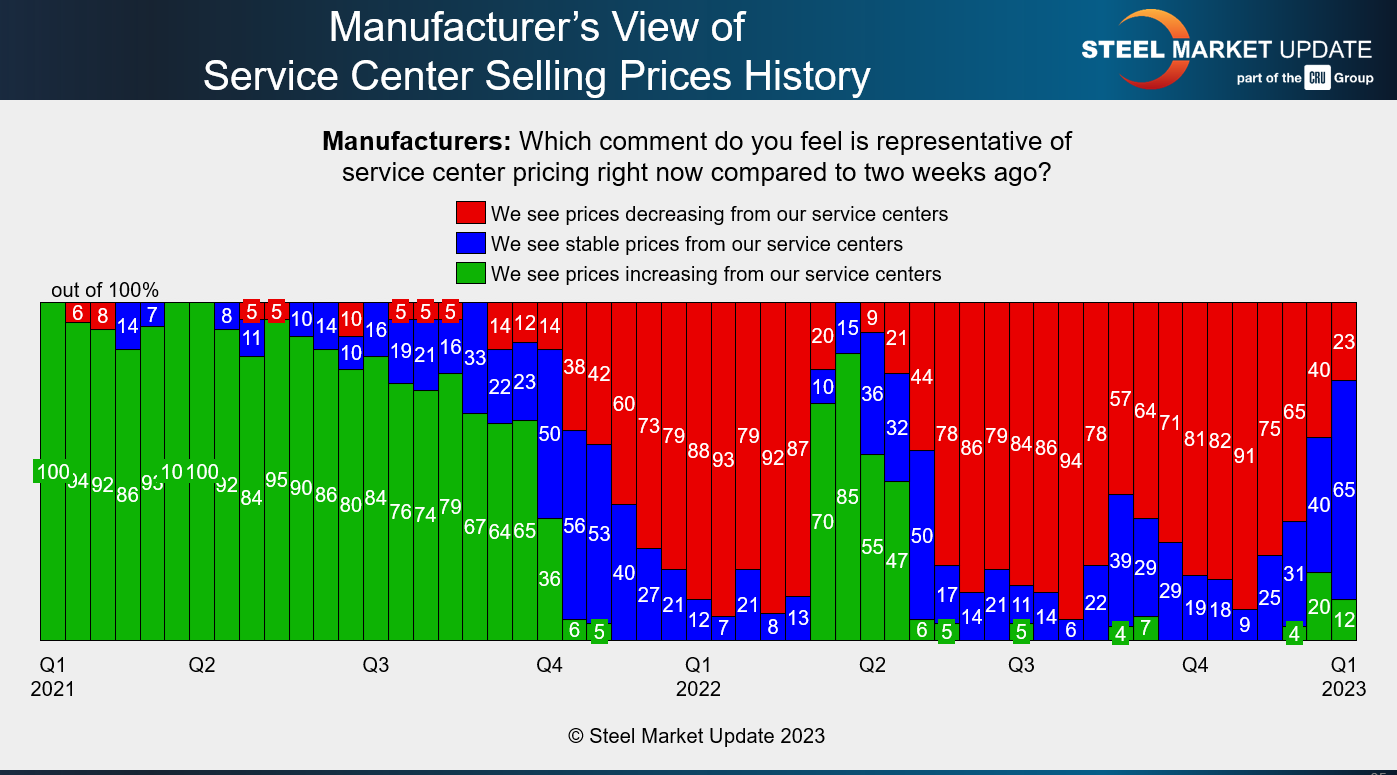

Here’s the same question asked of manufacturers:

We ask that question to manufacturers to keep service centers honest. Here, too, we’re seeing the strongest results we’ve seen since the outbreak of the war in Ukraine. And the latest reading is a lot better than what we saw in August/September when most service centers continued to cut prices even after mills made price-hike announcements.

What’s also notable is that there is a bit of disconnect. Only 12% of manufacturers say they are seeing increased prices from service centers, down from 20% in our last survey. That could be noise. But it’s also worth keeping an eye on in future surveys.

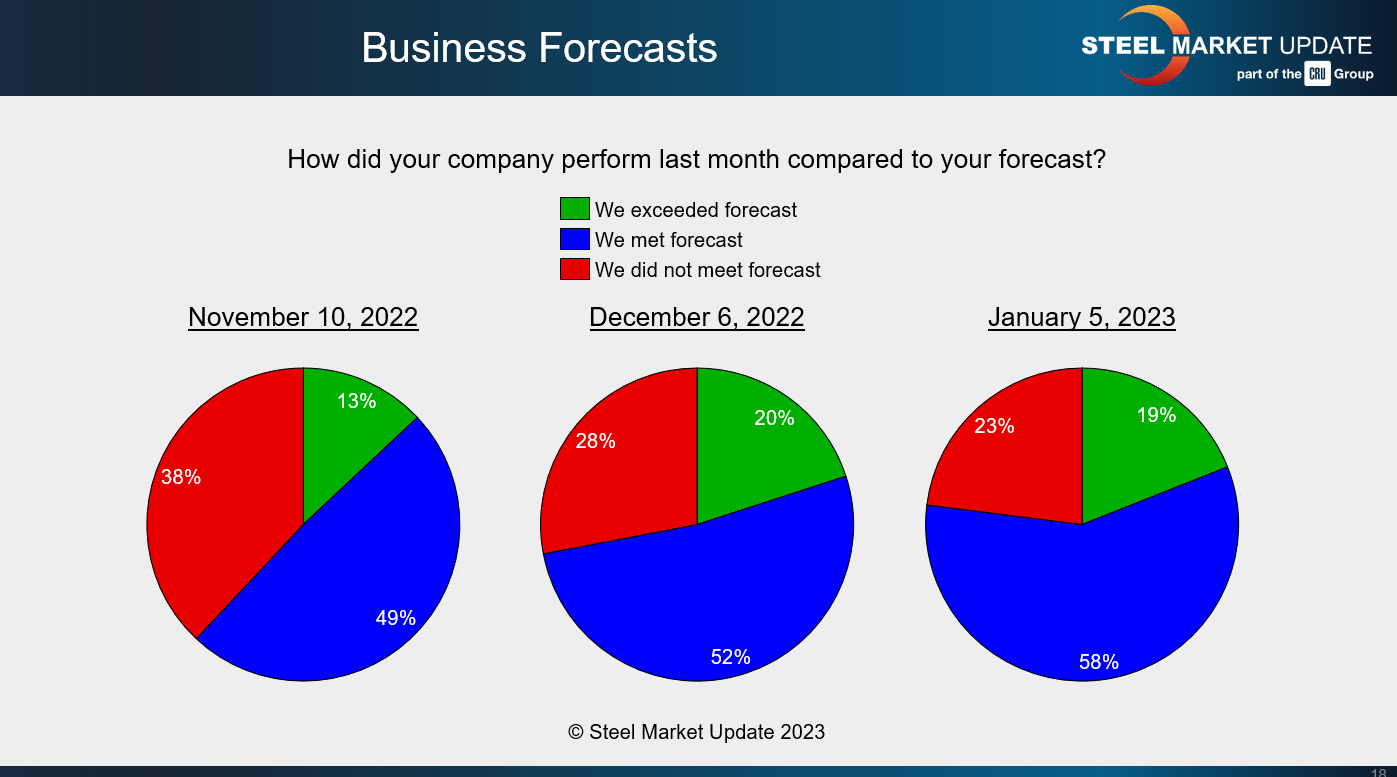

Other data mostly supports those who think that prices will continue to move up in the weeks ahead. This is one of my favorite survey questions – are people meeting their forecast:

Results over the last two months are improved compared to early November, which suggests that higher prices are not based solely on sentiment or momentum.

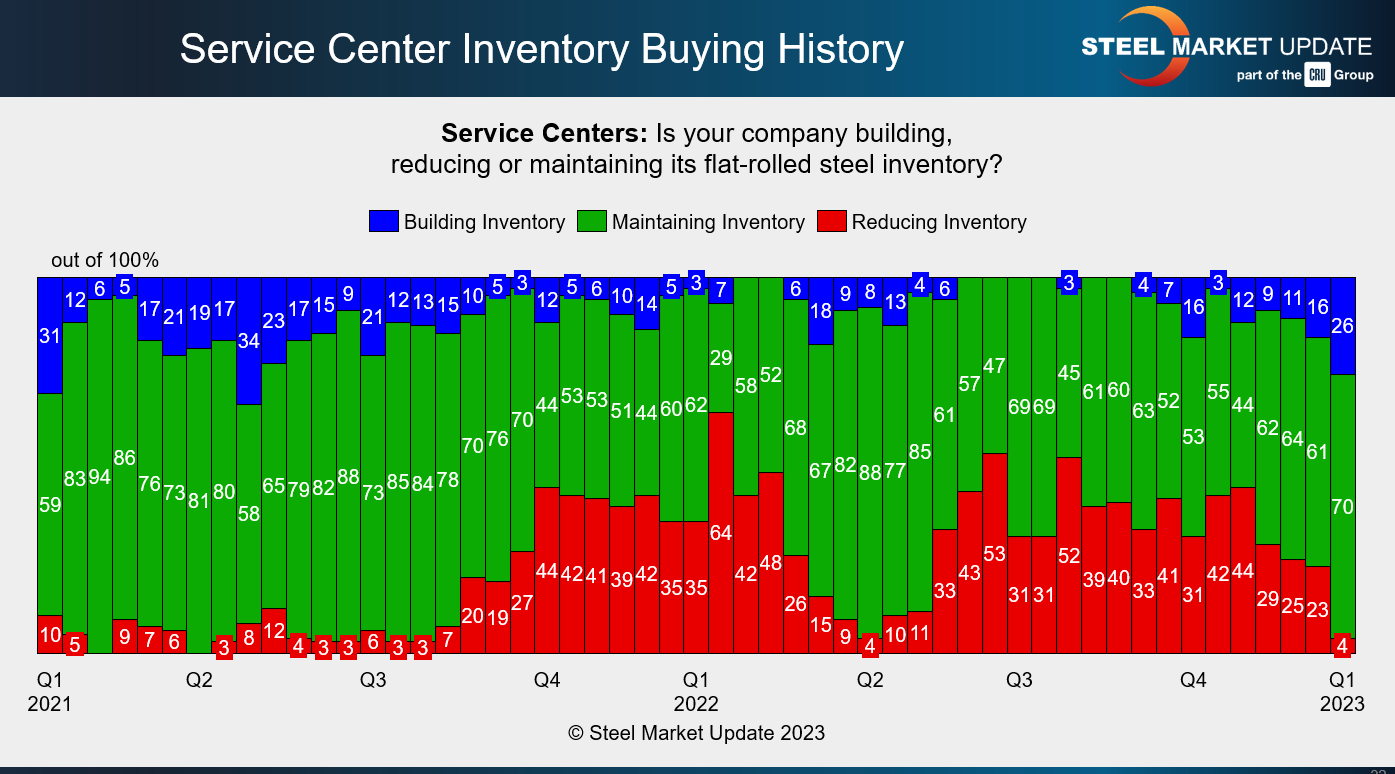

Another indication of a shift in the physical market – and not just in market psychology – is what appears to be a change in service center buying patterns.

Only 4% of service centers report that they are reducing inventories. Seventy percent say they are maintaining inventories. And 26% say they are building stocks. We haven’t seen a result that strong since the summer of 2021. To be clear, I’m not predicting that we’re getting back to a market that hot. There is no way we’re going back to nearly $2,000 per ton HRC. And, as I noted last week, mostly survey respondents don’t think we’ll break out above $800 per ton.

My point is simply that prices at or above current levels are probably sustainable at least in the short term. And I wouldn’t be surprised to see mills announce another round of price hikes on higher January scrap costs.

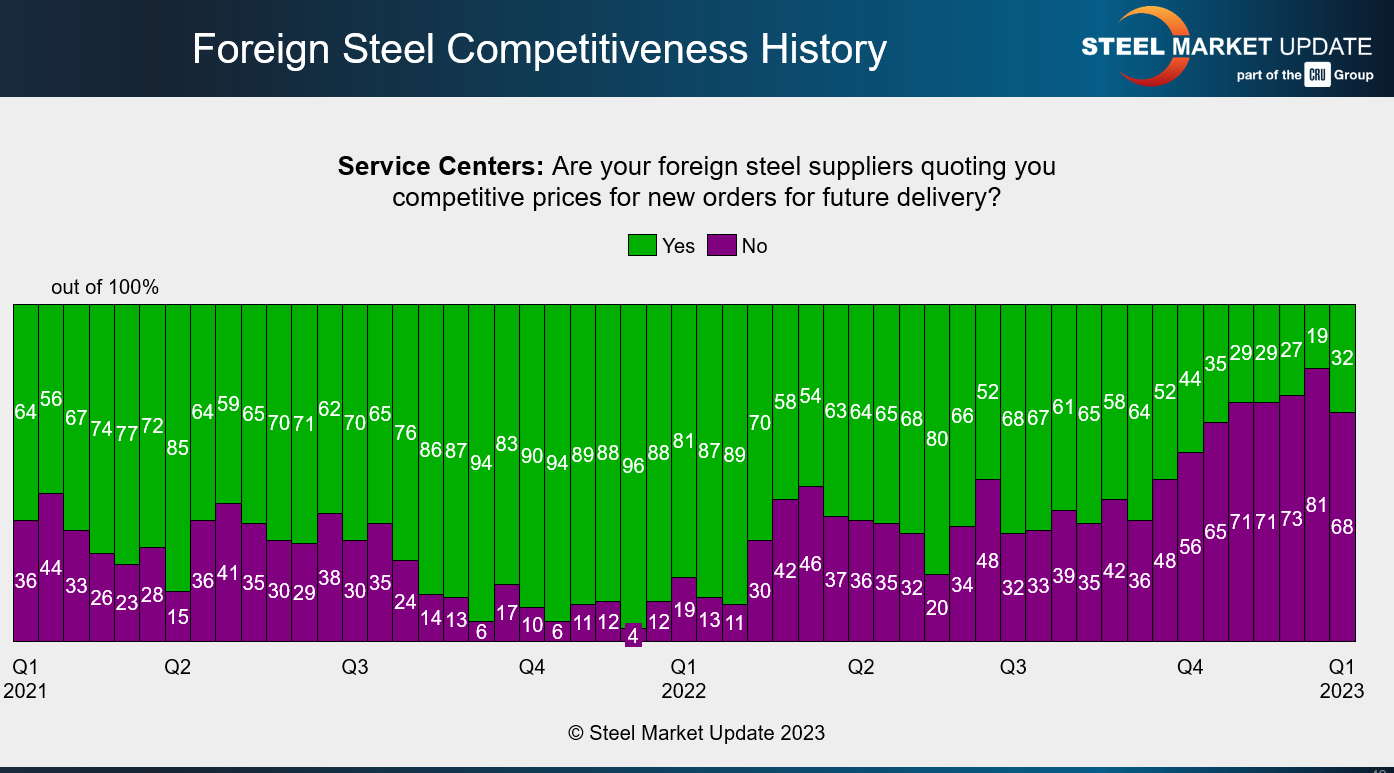

Could mills get greedy and announce too many price hikes? I can’t answer that. But I’ll leave you with one last slide to keep an eye on, this one about imports:

We’ve seen a modest increase in the number of survey respondents reporting that imports are competitive – 32% now, up from 19% in our prior survey.

If you drill down into the results, which you can do here, you’ll see that trading companies aren’t having much luck offering hot-rolled and cold-rolled products to US buyers. They report that the prospects of selling offshore coated, notably Galvalume, or plate to domestic consumers are better.

US mills tend to overshoot the market on the way up and on the way down. You could make the case that US mills brought sheet prices too low in early November. Might they overshoot to the upside later this quarter or in Q2?

Here is what some steel buyers and traders had to say about whether imports were attractive.

“Domestic still needs a month or two to make foreign steel more attractive.”

“Our customers are making more domestic buys vs imports now. But we are seeing more price checking for futures as domestic mills keep raising prices.”

“Depends on products. Bare Galvanized no. Pre-painted galvanized yes. Bare and pre-painted Galvalume yes. CRC and HRC, no.”

“No new Korean (HRC) offers yet and not sure if the price gap will be attractive enough.”

“Only countries like Australia or Mexico can be competitive (on CRC). No 25% Section 232 tariffs. I assume Brazil will also be competitive. But not to the West Coast.”

By Michael Cowden, Michael@SteelMarketUpdate.com