Analysis

April 23, 2023

Final Thoughts

Written by Michael Cowden

We’ve written in SMU about “green” steel and whether steel consumers, including market-leading OEMs, will pay a premium for it.

What about the potential for premiums in scrap too? Maybe not for green scrap. But what about for “prime grade” or prime-equivalent shredded scrap? Shred that transforms into prime – maybe we could call it Optimus Prime!

Joking aside, I’ve been thinking more about that after spending last week at the ISRI Convention and Exposition in Nashville, Tenn. It was one of the themes at the event, along the sidelines, and also among all the cool equipment and technology on display in the exhibit hall.

A Prime-ish Premium?

For a little context on premiums, consider the “green” steels introduced by US mills in recent years. US Steel’s verdeX or Nucor’s Econiq, for example. They are made with fewer carbon emissions than traditional steel. Mills want to collect a premium for the investment and work that has gone into decarbonizing their operations.

It’s not clear whether big OEMs, such as automakers, will be willing to pay a premium for green steel or will treat it more like a specification – a prerequisite for being a supplier. (The fact that not all mills will be able to make a low-carbon product might de facto create a premium, whether it is officially called one or not. But I digress.)

Point is, that debate is still ongoing. General Motors at Steel Summit last year indicated that it might pay a “green” premium in the short term but expects costs to come down as the availability of “green” steel increases.

Could we see a similar debate unfolding for “prime” shredded scrap, and to what extent is it already happening?

Steel Manufacturers Association (SMA) president Philip Bell noted in a presentation at ISRI that EAF steelmakers have made big strides in reducing pig iron consumption following Russia’s invasion of Ukraine last year.

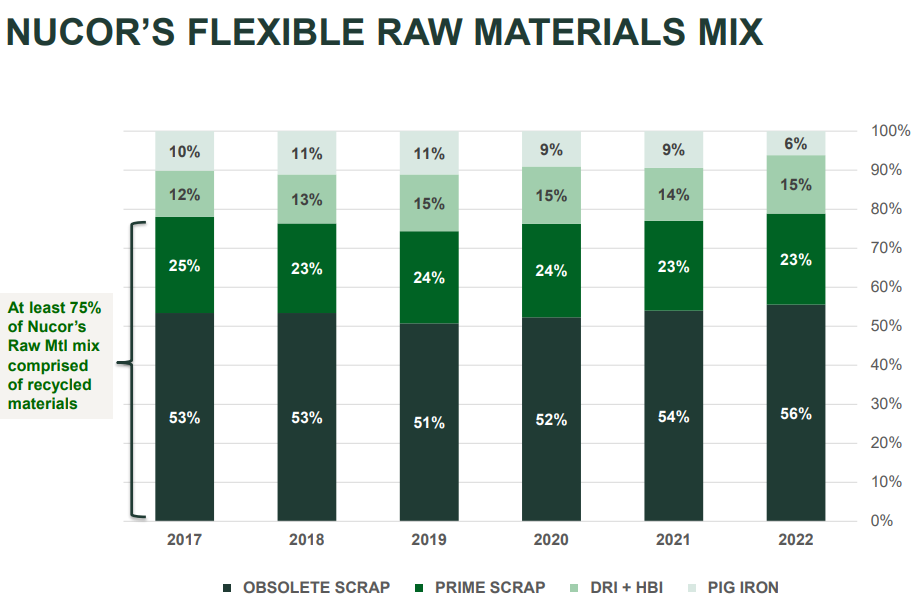

The slide below, from Nucor’s first-quarter earnings presentation on Thursday, illustrates that point well:

Pig iron accounted for only 6% of Nucor’s raw materials mix in 2022, down from 9% in 2020-21, and down from 11% in 2018-19.

Clearly, the steelmaker had been lowering pig iron use even before the war and was already investing in technologies that allowed it to produce more “low copper” shredded scrap. That shift went into overdrive following the Ukraine war.

Nucor in its first-quarter earnings call last year said it immediately stopped importing pig iron from Russia following the invasion, pivoting toward other raw material sources instead – not only other sources of pig iron but also alternatives to prime scrap.

A similar story is playing out at Steel Dynamics Inc. (SDI). SDI noted on its first-quarter earnings call last week that it continues to spend money on scrap segregation. That will allow it to recover more valuable nonferrous scrap for its copper joint venture and the aluminum rolling mill it is building. It will also reduce the amount of copper and aluminum in its ferrous scrap.

Recall impurities like copper can make steel more brittle and prone to crack in the automotive stamping process. That’s why prime scrap and virgin metallics like pig iron are preferred over shredded scrap for making sheet.

Also recall that Nucor owns The David J. Joseph Co. (DJJ), one of the largest scrap processors and brokers in the US. SDI owns Omnisource, another massive US-based scrap recycler. So what these steelmakers say about scrap matters, a lot.

Remember, too, all that talk about prime scrap being a precious metal? If we’re going to avoid a shortage of prime scrap – and reduce consumption of imported pig iron – a key part of the equation might be “prime” shredded scrap. As with steelmakers and green steel, no doubt scrap recyclers will want ROI on the more complex separation systems and more sophisticated magnets that they’ll need to make shred with purity and iron content qualities more closely resembling prime.

Will steelmakers be willing to pay more for “prime grade” shred? Or will they, like OEMs, hope that it will instead become a cost of doing business for their suppliers?

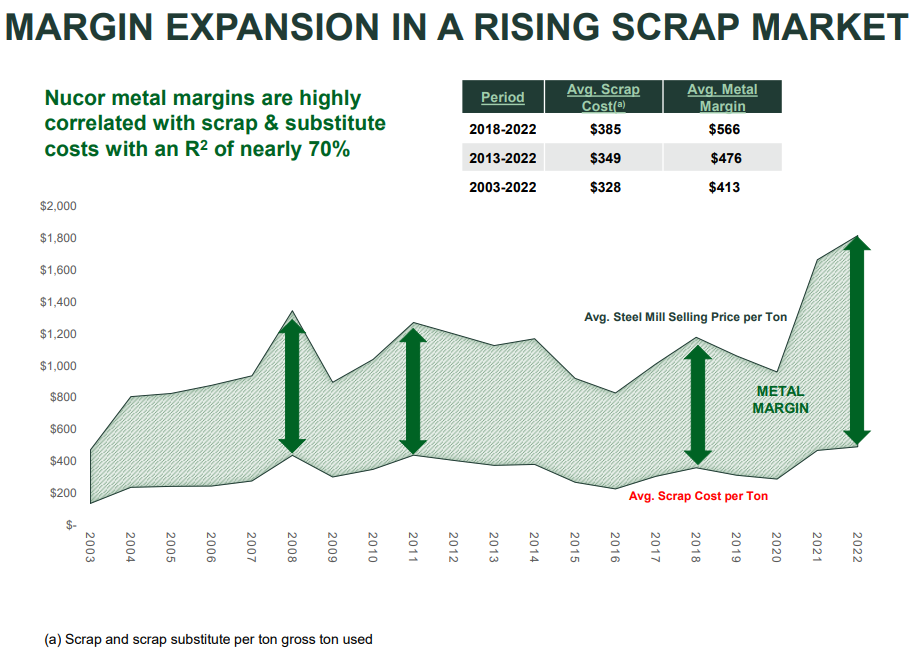

Metal Margins

Also, if we see premium grades of scrap evolve, what that does to metal margins – aka, the spread between scrap costs and steel selling prices.

Nucor in its earnings presentation noted that both scrap prices and metal margins have gone up over the last 20 years, and that metal margins have risen more than scrap costs.

Over the last five years, we saw a big spike in metal margins in 2018 following the implementation of Section 232 tariffs on finished and semi-finished steel imports – but not on scrap imports. We also saw margins explode after the pandemic.

Are those higher margins sustainable? Or will higher scrap costs, albeit for a more sophisticated product, start to eat into them?

That’s fodder for another Final Thoughts. In the meantime, thanks, from all of us at SMU, for your continued business!

SMU Steel Summit

We’ve already revealed some of the big-name speakers for our Steel Summit conference on Aug. 21-23 in Atlanta. This year will also feature more scrap content that we’ve had in years past. You can learn more and register here. (It’s not too early. Hotels near the Georgia International Convention Center tend to go fast.)

By Michael Cowden, michael@steelmarketupdate.com