Analysis

August 19, 2023

Final Thoughts

Written by Michael Cowden

I’m excited to see pretty much the entire steel industry this week in Atlanta. I’m looking forward to networking and to learning from our great lineup of speakers.

I also want to draw your attention to some highlights from our latest steel market survey. (Full results are here.) Some of these topics will be discussed along the sidelines as well as up on the stage.

UAW Negotiations

For starters, how seriously should the steel market take the threat of a United Auto Workers (UAW) strike? Recall that the current labor contract between the UAW and the “Big Three” automakers – Ford, General Motors, and Stellantis – expires on Sept. 14 at 11:59 pm.

We asked steel market participants in our latest steel market survey whether they thought there would be a strike. It was close to a 50/50 split: 45% said there would be a strike, and 55% said the two sides would reach an agreement.

That said, even among those who think there will be a strike, many predict it might be only short and mostly symbolic – meaning an any extended stoppage might catch the market by surprise.

Here are some of the responses we received:

“No one can afford a strike.”

“I have to think that ‘cooler heads will prevail’. But maybe that is just being naïve. Certainly a lot of bluster out there right now.”

“New deal. But after some tense negotiations and threats of a strike.”

“The president won’t allow a strike to happen, similar to the railroad strike.”

“UAW demands are off the charts.”

“While it sounds like a giant increase in wage, the auto companies knew a sizeable increase was coming simply by watching other increases to contract. Despite all the posturing, they are not as far apart as it would appear.”

“I don’t see a full strike benefiting either side. Thus, I look for smaller disruptions to drive a point home and keep up the pressure on the bargaining process.”

“Short strike, but both sides need a deal to be reached.”

“I suspect there will be a short, non-disruptive stoppage and nothing longer.”

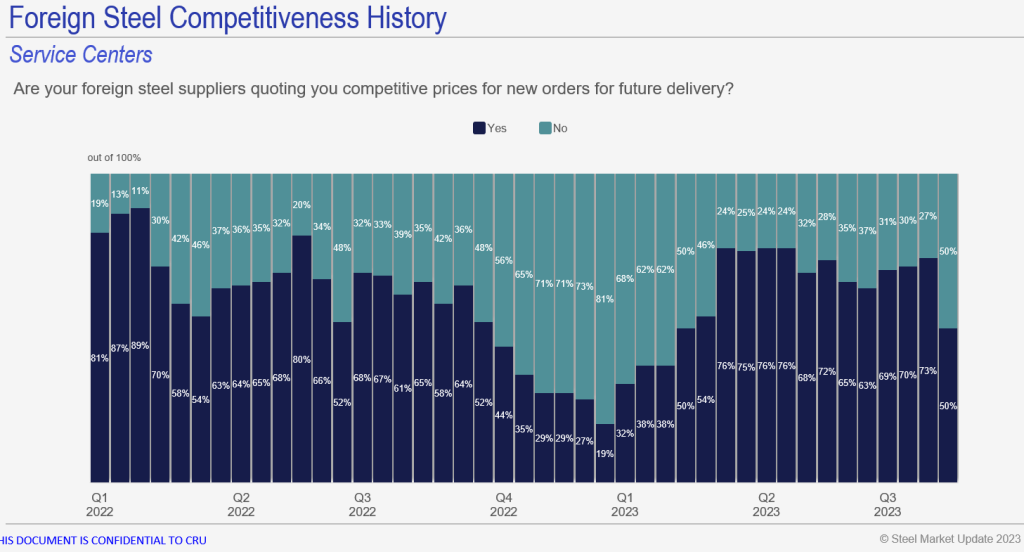

Imports Losing Appeal?

This one hasn’t garnered as much attention as UAW contract talks. But it’s perhaps just as important to the day-to-day steel market.

As with UAW negotiations, it’s a 50/50 split on whether import prices are competitive with domestic prices.

That might not seem like much at first glance. But check out the chart below.

We haven’t seen a reading like that since early in the first quarter of 2021 – before US prices surged higher.

Recall that before that happened, in late November/early December 2022, domestic sheet prices had hit their lowest point of 2021 – falling into the $600s per ton, and in the $500s per ton on the low end of our range. (You can chart that data out for yourself with our pricing tool.)

In other words, low domestic prices and short domestic lead times resulted in buyers moving away from imports in early 2024. Import prices are once again close to US prices on a landed basis. Domestic lead times aren’t very long either. So could we see a trend of lower imports in the second half of this year?

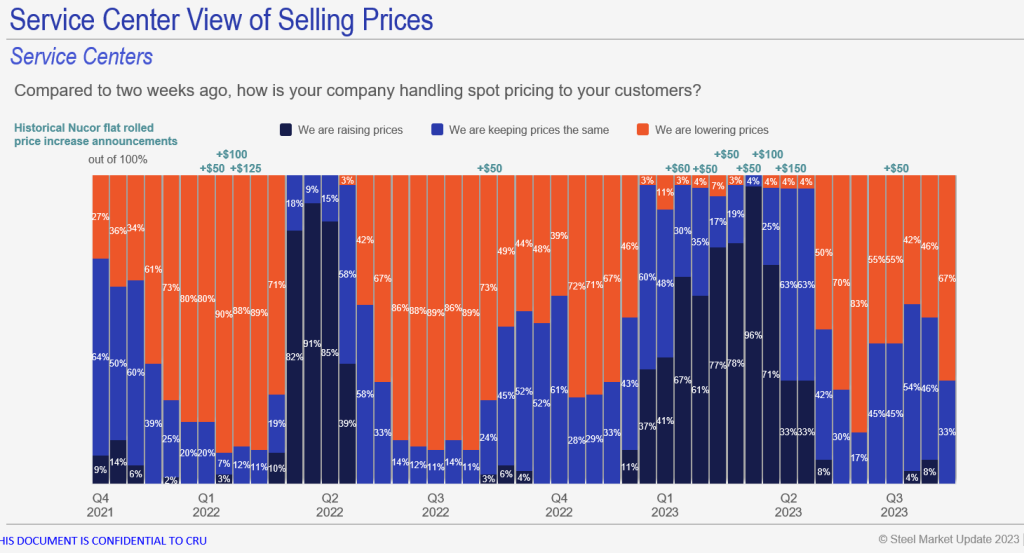

Service Center Prices Still Moving Lower

Despite the potential for lower import volumes, service centers continue to drop prices to their downstream customers:

Sixty-seven percent of service center survey respondents said that their companies were lowering prices. We haven’t seen a result like that since late in the second quarter when 83% of service center respondents reported lowering prices.

That’s what SMU founder, John Packard, sometimes referred to as “capitulation” territory. That occurs when steel buyers become just as tired as mills of seeing falling prices (and falling inventory values). It something leads them to support mill price hikes as a means of stopping the slide.

We saw some evidence of that in mid-June following a $50-per-ton sheet mill price hike. Could we see something similar again now? And would service centers and mills hold the line? Or would it be like late June/early July, when efforts to enforce higher prices were half-hearted?

PSA re the U.S. Steel Sales Process

The other big current event in steel, besides the UAW strike, is the potential sale of U.S. Steel.

That news broke just after noon on Sunday, Aug. 13. U.S Steel said it had received multiple unsolicited offers. We learned the same day that one was from Cleveland-Cliffs. Later in the week, it was reported that ArcelorMittal was also in the hunt.

I am not going to add speculation about who other buyers might be or whether any deal would result in a purchase of all or part of U.S. Steel. As many of you know already, Cleveland-Cliffs decided at the last minute that company chairman, president, and CEO Lourenco Goncalves could not speak at Steel Summit because of the sensitivities surrounding the sales process.

And so I very much appreciate that other US mills are still participating in the event – including U.S. Steel. But what I want all of you to know now is that some of them will not be able to talk about the sales process. U.S. Steel, for example, said last week that after announcing the potential sale that it would not make additional public comments. That remains the case.

I realize the potential sale of an iconic American steelmaker will no doubt be a topic of debate along the sidelines. But, again, please recognize that some companies will not be able to speak about the matter on stage. Nor will their employees be able to speak about it in private conversations. Please respect that.

Steel Summit 2023 App and Streaming

If you’re attending Steel Summit this year, you should have by now downloaded the Steel Summit 2023 app from the app store.

You will use it for networking, receiving agenda updates, and participating in polls as well as Q&A sessions. You can also use the app to stream the proceedings to your devices should you need to step away from the conference hall.

Steel Summit of course starts on Monday. It’s awfully late to book a last-minute flight. But we welcome walk-ins. If you plan to walk in, please register ahead of time if you can.

Should you be unable to attend in person, we are now offering the option to register for the event for a reduced fee of $1,495 using promotional code VIRTUAL23 during checkout.

That will allow you to follow us live from your office or home as well as to network with attendees onsite. Recordings of some, but not all, conference proceedings will be available for 30 days after the event.

That’s it for now. I’ll see many of you very soon in Atlanta!