Analysis

September 26, 2023

Final Thoughts

Written by Michael Cowden

Sheet prices declined less than usual this week. Does that mean we’re nearing a bottom, or is it just a pause before the market moves lower yet again?

Your answer might depend on whether you think the United Auto Workers (UAW) strike will be a typical 4-6 weeks or whether it might be a lengthier disruption.

It’s above my pay grade to handicap the strike, so I’ll lay out the two cases I’ve heard for prices this week – a bull case that prices are near a bottom, and a bear case that they still have room to fall.

The Bull Case

I spoke to one mill executive who said his company had recently recorded their best booking week of the year.

Were the prices great? No. HRC was in the low $500s per ton for companies capable of buying 100,000 tons or more. The figure was the mid/high $500s per ton for those buying 10,000-20,000 tons or more. So why be proud of that? This week, he said, his company has been able to hold the line around $640-660 per ton for standard spot buys.

I’ve heard similar things from buyers. Namely, that (a) we might already be past the price bottom for “big tons” and that (b) the bottom for standard spot tons will follow on a bit of a lag.

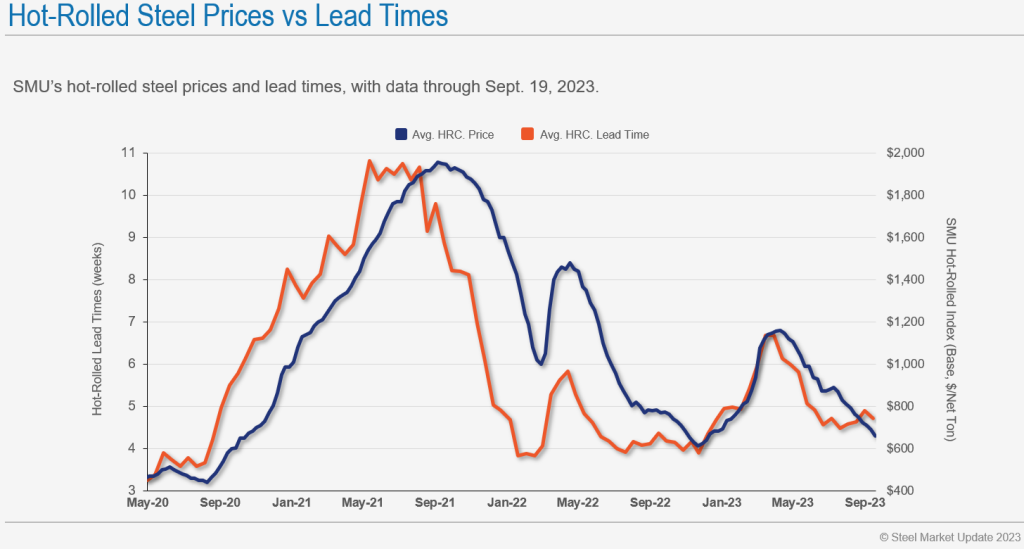

How is it that we’re talking about a potential sheet price bottom during an expanding UAW strike? The charts below might be instructive.

Below we’ve plotted out HRC prices and lead times.

As you can see, prices dropping below lead times doesn’t happen often. When it does happen, it’s often an indicator that prices are about to bottom out and rebound.

Some of you would disagree with this. You’ll say that HRC lead times are shorter than advertised. But keep in mind that these are averages.

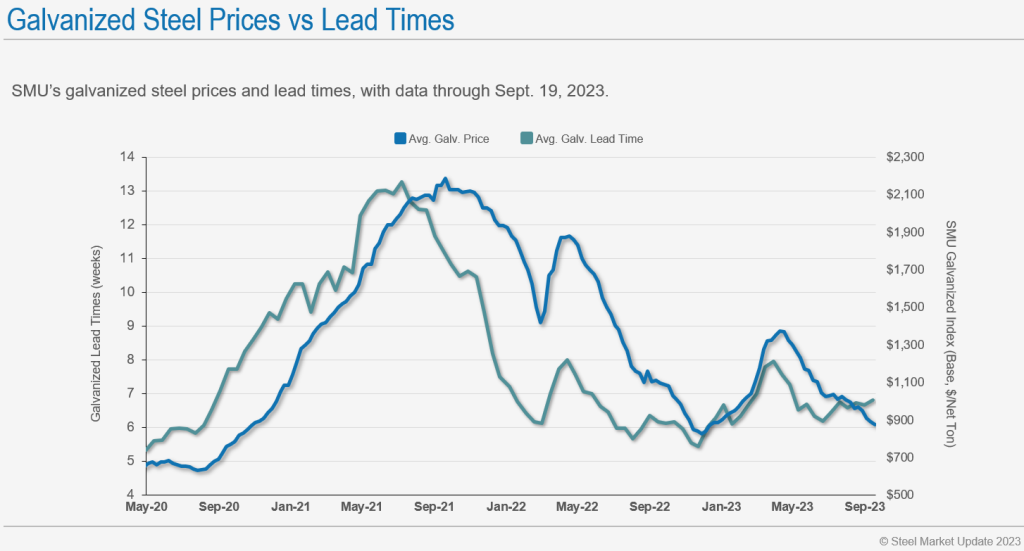

Also, we’re not just seeing that trend in HRC. Below are base prices vs. lead times for galvanized coil:

I think there is less room for complaint with the galvanized lead times. We know from a recent SDI lead time sheet that the steelmaker is out roughly 7-8 weeks for galv. That’s extended for SDI, especially considering that the company typically keeps lead times short by design.

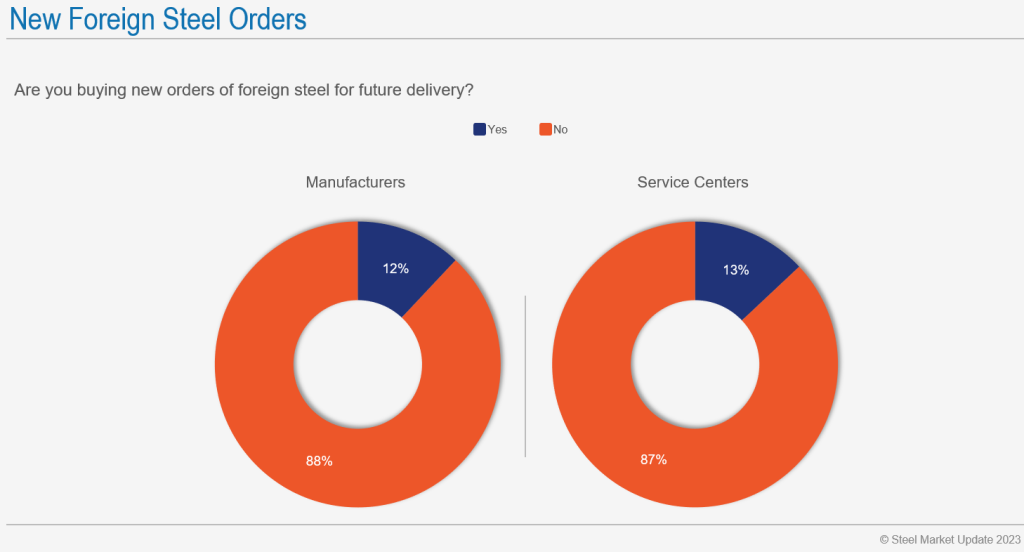

We’ve also written in recent editions that US prices are near parity with prices abroad and below them once you factor in freight and other costs.

With domestic price low and lead times relatively standard, few respondents to our survey say they are looking to buy foreign steel:

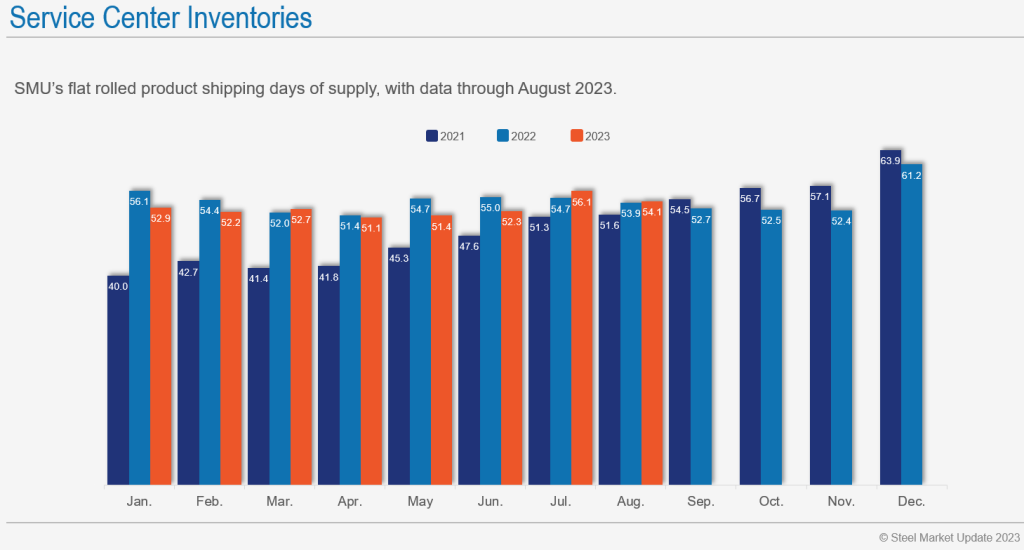

And what do inventories look like?

Here’s where they were in August:

August 2023, the orange bar, is down modestly from July and roughly on par with where we were in August 2022, the light blue bar.

We won’t have September numbers until the middle of next month. That said, and as we’ve noted before, many steel buyers have been reducing inventories over the last month. I wouldn’t be surprised if September inventories were also lower.

In other words, this looks a lot like what we saw in the fourth quarter of last year. That’s when low domestic prices and limited offshore buys helped set the stage for a sharp rebound in Q1.

And make no mistake, there is a school of thought, one that has gained significant traction over the last two weeks, that prices will pop in Q4 as soon as there is any inkling that the UAW strike might end.

The Bear Case

On the HARDI call today, it was pointed out that few people had expected galvanized prices to fall below $1,000 per ton. And yet here we are in the $800s per ton on average – meaning that we’re collectively not very good at predicting the future.

And while it was not a majority opinion, at least a couple of people on the call expressed concern that the UAW strike could become a protracted one.

Keep in mind that the UAW has struck just three assembly plants to date. The strike at parts distribution centers, announced last Friday, might have more impact on dealers than on automotive production. In other words, steel production is probably less impacted now than it was at this point in the 2019 strike against all GM facilities.

But it’s no secret that the UAW and the “Detroit Three” automakers are far apart on a range of issues. What happens, then, if the strike expands this Friday to more assembly plants? I’m guessing we might see more blast furnace idlings, especially at mills heavily exposed to automotive. We might also see the extension of current or upcoming fall maintenance outages.

I can see why some are predicting a lengthy strike. President Joe Biden on Tuesday joined a picket line in Belleville, Mich. – a first for a sitting president. He told striking workers: “You deserve what you’ve earned. And you deserve a whole hell of a lot more than you’re getting paid now,” according to The Washington Post.

That’s not exactly the kind of language that might bridge the gap between the “Detroit Three” automakers and the UAW. (Well, President Biden also said earlier this month that there would be no UAW strike. So let’s not overestimate his influence on these negotiations.)

In any case, what happens to the consensus that has formed over the last two weeks – that prices are at or near a bottom – if UAW President Shawn Fain announces more “Stand Up” strikes on Friday? Let me know your thoughts!

Tampa Steel Conference

Our Tampa Steel Conference might not be until Jan. 28-30, 2024. But our early-bird discount expires Sept. 30. And hotel rates are only going to go up as we get closer to peak tourism season in the Sunshine State. So register now!