Analysis

October 10, 2024

Final Thoughts

Written by Michael Cowden

I’m trying to make sure this is not a TL;DR Final Thoughts. As a journalism school professor once told me, ‘No one but your mom reads more than 1,000 words.’ Also, as the old adage goes, a picture is worth a thousand as well.

With that in mind, below are a couple of charts I think go a long way toward explaining how prices and lead times have been relatively stable despite concerns about demand.

Why aren’t prices going up?

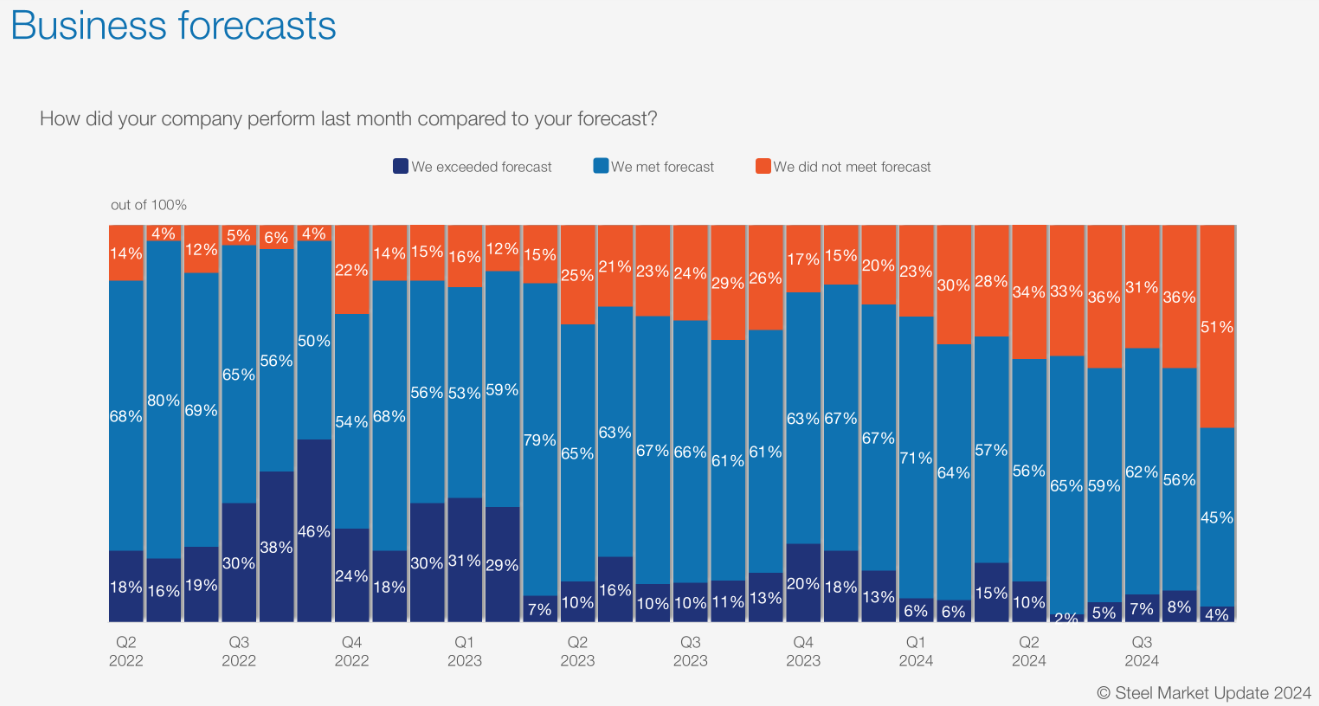

Take a look at the chart below. We asked a simple question: “How did your company perform last month compared to your forecast?”

Rewind to 2022. The vast majority of folks responding to our surveys said they were meeting or exceeding forecast. (There is no data for Q1’22 because we hadn’t introduced the question yet.) In most months, only 5-10% said they were missing target.

The number missing forecast increased to roughly 15-30% in 2023. In 2024, it’s ticked steadily (if unevenly) higher from there. And 51% of respondents in our survey this week said they missed forecast in September.

I try not to read too much into any one survey. Even so, it’s worth noting that that’s the highest number we’ve seen since we’ve been asking this question.

Here’s what respondents were saying:

- “We were pretty much right on forecast; very slight beat.”

- “Fell slightly short of forecast.”

- “There has been a noticeable drop in volume.”

- “Slow demand.”

- “Buyers pulled back more than expected last month, and some pullback on automotive – mainly Stellantis.”

- “For us, this market is worse than 2009 in terms of volume.”

Ethan Bernard has more on the troubles at Stellantis here. As for 2009, I feel like it’s sort of steel’s version of “Voldemort.” Don’t say it. Or it’ll come back and hunt you down.

I’m not in the 2009 camp. And I’m not sure the person who wrote that is either. Because while volumes might be off, prices are a lot better now than they were then.

SMU’s price for hot-rolled (HR) coil averages $695 per short ton (st) now. Rewind to 2009, and HR prices were as low as $380/st, according to our pricing archives. Adjusted for inflation, that’s about $555/st in 2024 dollars. (That’s according to the US government’s inflation calculator.)

If demand and volumes are off, what’s keeping prices steady around $700/st?

Why aren’t prices going down?

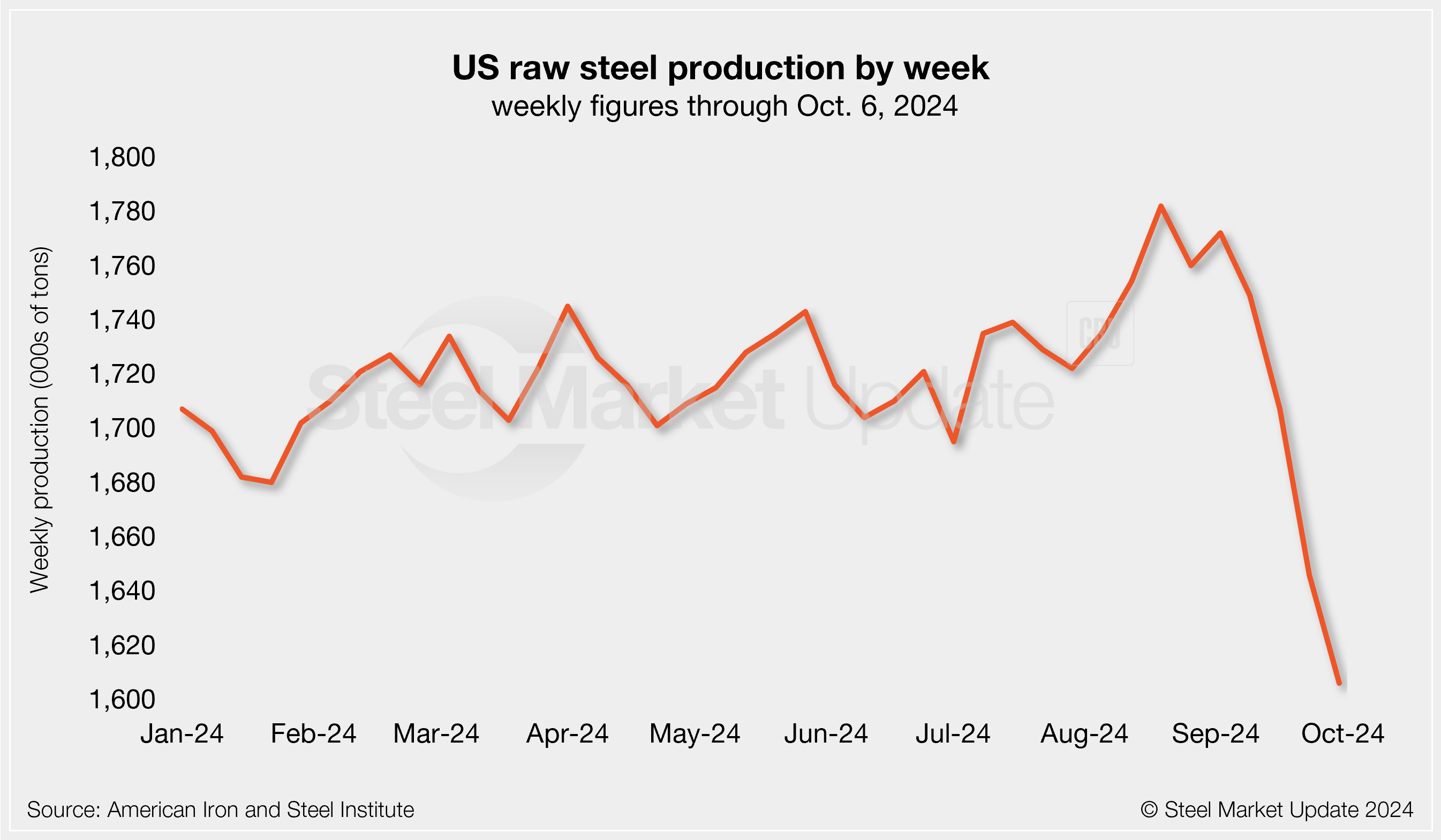

This might be oversimplifying it. But simply put, domestic production fell sharply in mid/late September and early October.

Some of that might be steelmakers ratcheting back production in response to weaker demand. A good portion of it could also be maintenance outages. You can see from our maintenance outage calendar that much of the downtime is in October.

What happens a few weeks from now when most of those outages are over? Will lead times be close enough to Q1, typically a busier time of the year, to keep prices from slipping too much further? Could those outages be extended? Or could we have a sloppy year-end market, as we’ve seen in past years?

In the meantime, and despite those outages, steel buyers tell us that most mills remain willing to negotiate lower prices.

Another adage, at least in steel, is that you can’t get ahold of your mill representative when times are good. And that they’re calling you when the market is soft. We’re guessing there might be more catching up now than there was last year, when prices were (in the case of HR) exactly where they are now but on their way higher.

Tip o’ the hat

We tend to get a little obsessive about short-term trends. It’s hard not to when you’re polling the market every week.

But steel is about a lot more than that. And I think Steel Dynamics Inc. (SDI) deserves some credit for becoming the first steel producer to certify its decarbonization targets with the Global Steel Climate Council.

Those targets, which align with the Paris Agreement, stretch out as far as 2050. What I think is cool: The company is taking concrete action now – like a project to replace anthracite coal used in its EAFs with biocarbon.

Biocarbon is a fancy way of saying, for example, the bark and other trimmings left over from a timber mill. So, you know, doing what EAFs have long done – turning someone else’s waste into something very useful.

SMU subscription levels

The first chart above is a sneak preview of results from our full steel market survey. We’ll release those to our premium subscribers on Friday.

Give us a shout at info@steelmarketupdate.com if you’re executive and you’d like to upgrade to premium. Premium gives you all the news and prices you get in executive, along with our proprietary data – not just the surveys but also useful stuff like service center shipments and inventories.

You can also ping us at info@steelmarketupdate.com if you’re active in the market and would like to participate in the survey. Your feedback helps us keep our finger on the pulse of the industry – especially when it moves in unexpected directions.