Analysis

April 15, 2025

HVAC equipment shipments mixed in February

Written by Brett Linton

Heating and cooling equipment shipments increased 2% from January to February, according to the latest data released by the Air Conditioning, Heating, and Refrigeration Institute (AHRI).

Water heater and air conditioner/heat pump shipments climbed higher, while warm-air furnace shipments eased month over month (m/m).

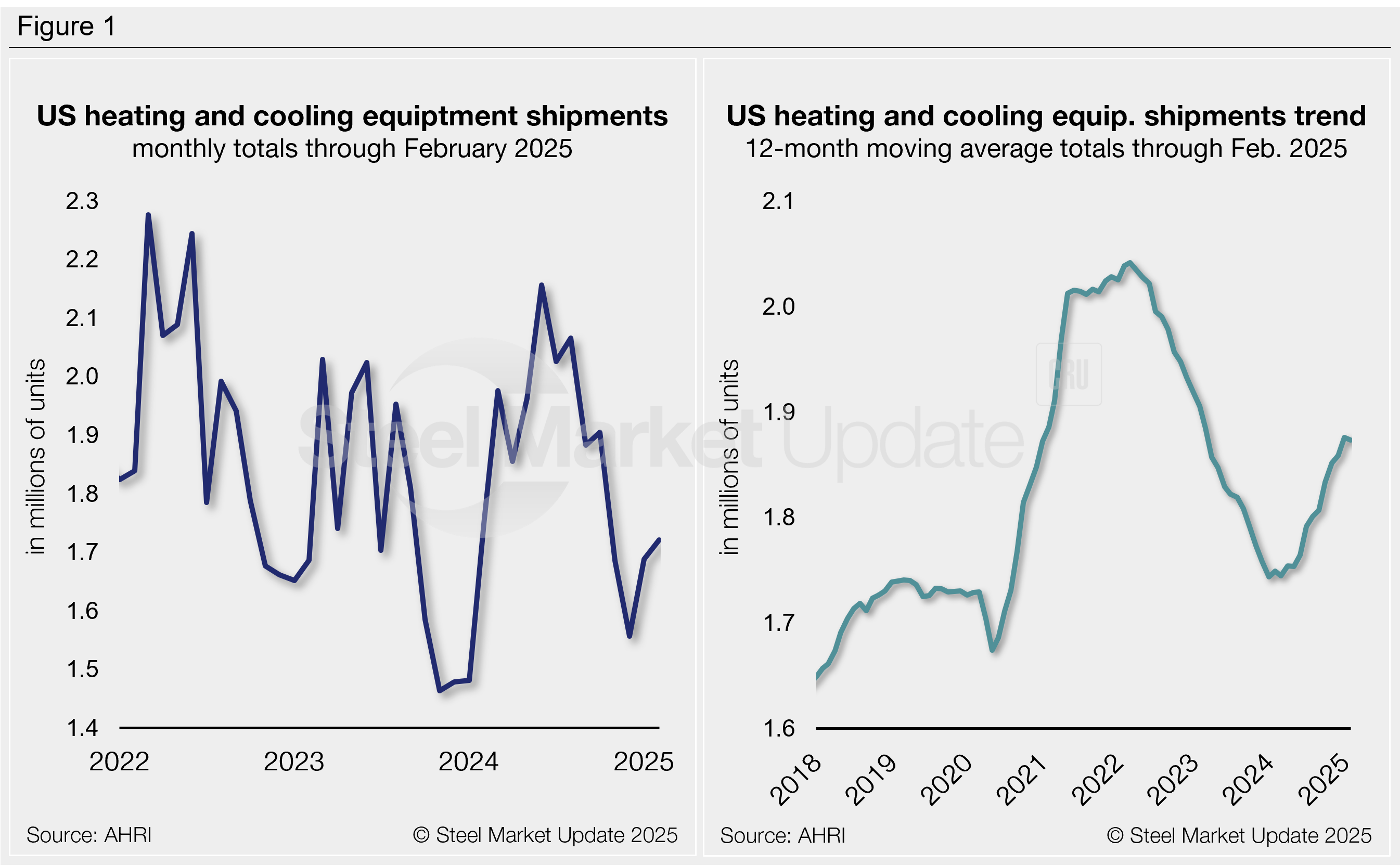

February shipments increased by 33,000 units m/m to a four-month high of 1.72 million units (Figure 1, left). This recovery is seasonal, as air conditioner and heat pump shipments typically decline each winter and recover in the spring and summer months.

Following eight consecutive months of positive annual growth, February shipments were 2% less than shipments seen one year earlier.

Trends

To smooth out seasonal fluctuations, shipment data can be annualized as a 12-month moving average (12MMA) to better showcase long-term trends. On this basis, total shipments peaked in early 2022 following the post-Covid surge, then declined through late 2023. Shipments began to recover in early 2024 and have continued to do so since. Following January’s 22-month high, the February 12MMA declined less than 1% m/m and remains strong at 1.87 million units (Figure 1, right).

Shipments by product

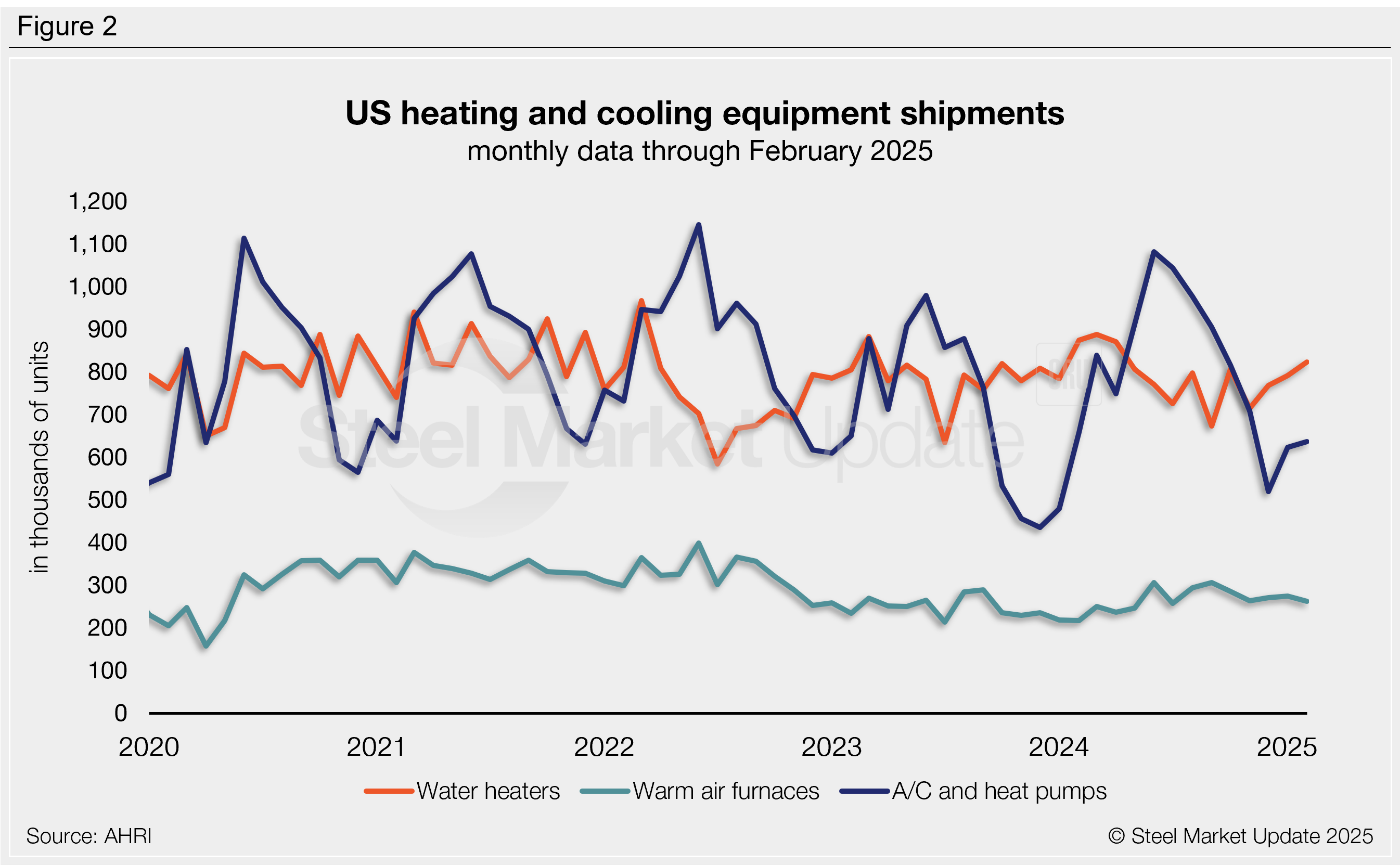

- Water heater shipments grew 4% m/m in February to a 10-month high of 823,000 units, marking the third consecutive month of increasing shipments. February shipments were down 6% compared to one year prior, but 2% higher than February 2023 levels.

- Shipments of warm air furnaces fell 4% in February to a seven-month low of 262,000 units. Despite the monthly drop, shipments remain solid compared to past years. February shipments were 21% higher this year than the same month last year, marking the ninth-consecutive month with positive annual growth.

- Air conditioners and heat pump shipments increased 2% m/m in February to 636,000 units. While shipments rose m/m, levels remain below seasonal norms. February shipments were 3% lower than levels seen one year prior and 2% off from the same month of 2023. Note that air conditioner/heat pump shipments are very seasonal, as evident in Figure 2.

All products see annual growth

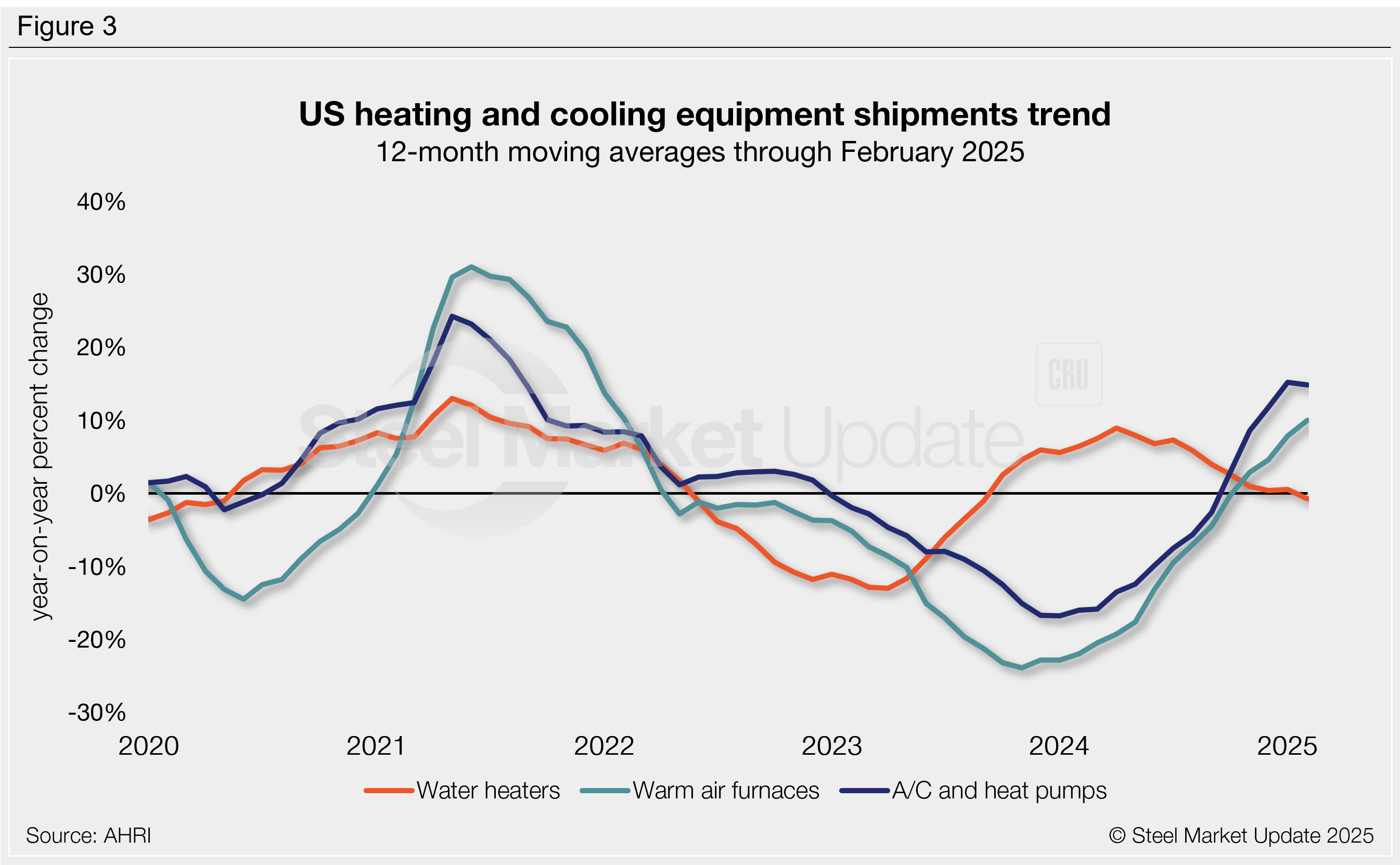

Figure 3 shows the annual growth rate of shipments by product on a 12MMA basis:

- Air conditioner and heat pump shipments experienced the largest annual gain, rising 15% from the previous year to one of the highest annual growth rates witnessed since 2021.

- Warm air furnace shipments grew by 10% year over year (y/y), the highest rate witnessed in three years.

- Water heater shipments saw a modest annual decline of 1%. Previously positive, this growth rate has been steadily declining since peaking in mid-2024.

An interactive history of heating and cooling equipment shipment data is available here on our website. If you need assistance logging in to or navigating the website, please contact us at info@steelmarketupdate.com.