Analysis

April 17, 2025

April energy market update

Written by Brett Linton

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona luis.corona@crugroup.com.

In this Premium analysis we examine North American oil and natural gas prices, drill rig activity, and crude oil stocks. Trends in energy prices and rig counts serve as leading indicators for oil country tubular goods (OCTG) and line pipe demand.

The Energy Information Administration (EIA) recently released its April Short-Term Energy Outlook (STEO). The latest report projects declining crude oil prices, with a downwardly revised forecast due to rising inventories and slower demand growth. Natural gas prices are expected to rise through 2026, driven by increased heating demand and growing exports.

The report notes that recent trade policy changes are not fully reflected in these forecasts, and that the broader economic impact of these tariffs introduces significant uncertainty into future oil price and demand projections. Click here to read the full April STEO report covering energy spot prices, production, inventories, and more.

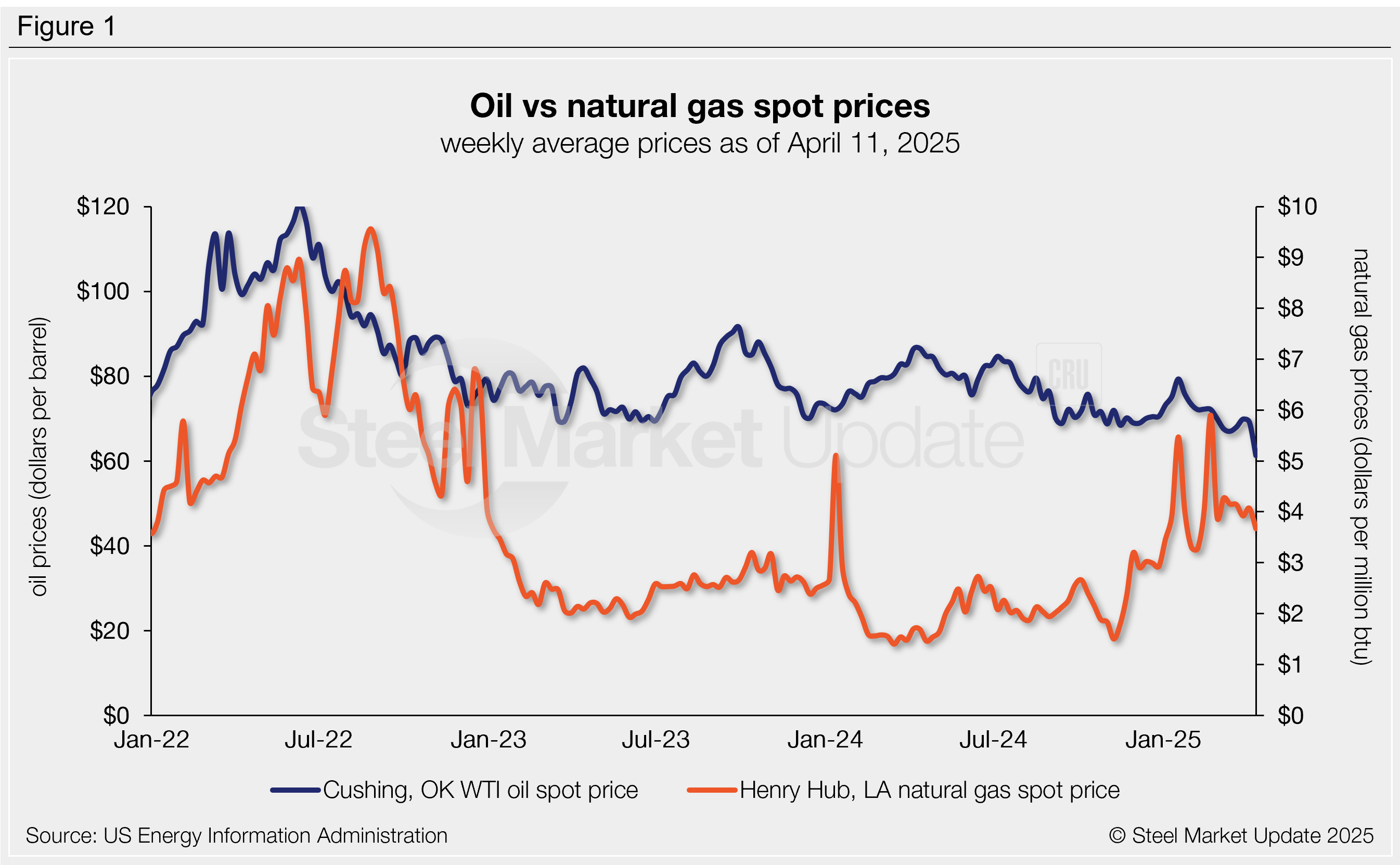

Oil spot prices

The weekly West Texas Intermediate oil spot market price has tumbled to a four-year low of $61.24 per barrel (b) as of April 11 (Figure 1). Oil spot prices have trended downward since the January peak of $79.28. In late February, prices slipped below the $70-90 per barrel range generally observed across the previous two years and have remained there since.

The April STEO forecasts oil spot prices to average $68/b across the rest of 2025. Looking further ahead, 2026 prices are now forecast at $61/b, down from the previous estimate of $66/b.

Gas spot prices

Following the multi-decade lows seen in 2024, natural gas spot prices surged from November through February due to increased winter heating demand. Prices briefly touched a two-year high of $5.90/mmBtu in mid-February, but have settled back down since. The latest natural gas spot price receded to a nine-week low of $3.67/mmBtu as of April 11.

EIA revised its April natural gas forecast upward for the second consecutive month, forecasting 2025 prices to average $4.30/mmBtu. Estimates for 2026 have also been raised for the third consecutive month, rising from $4.50/mmBtu in March to $4.60/mmBtu in the latest report.

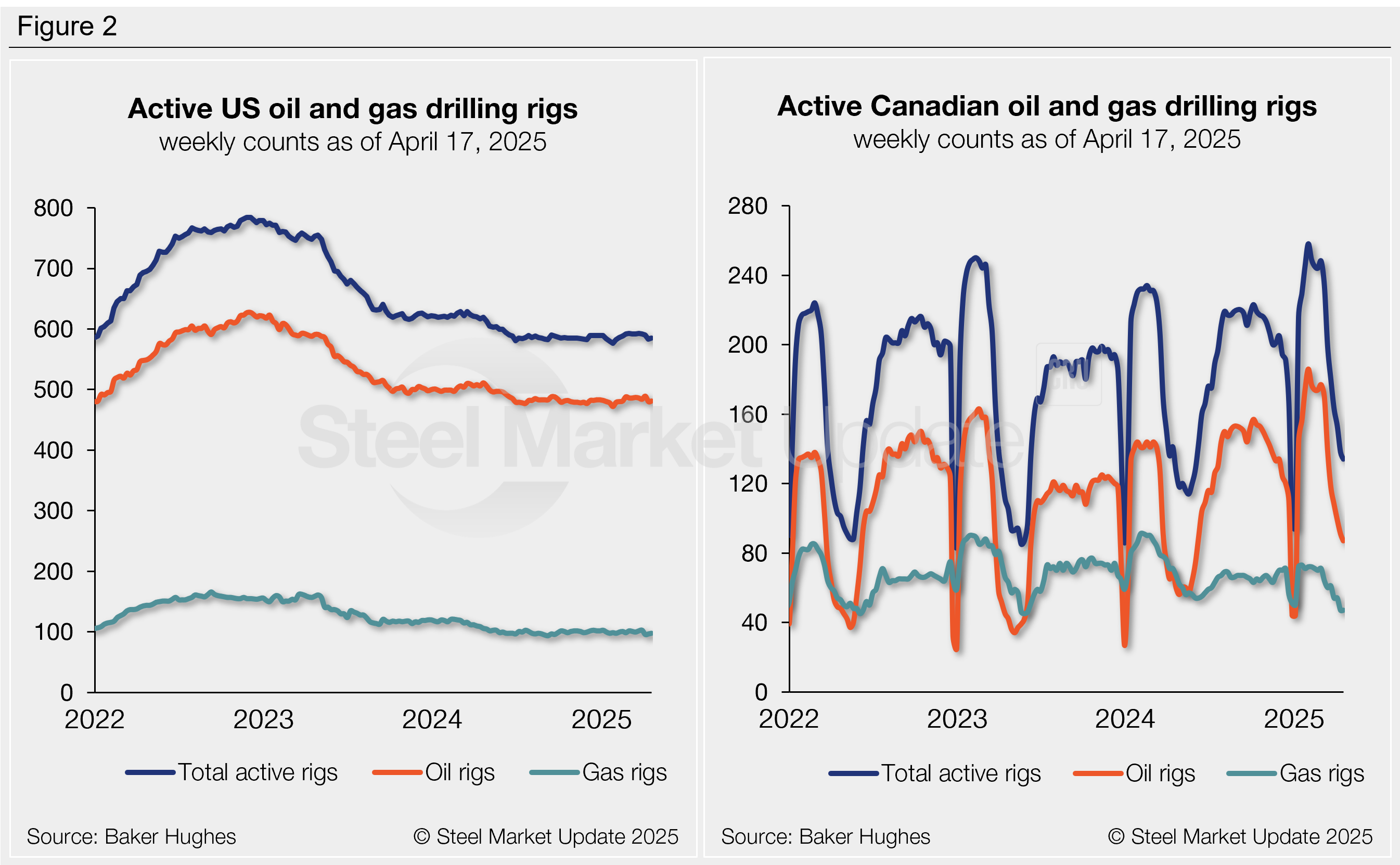

Rig counts

US drilling activity rose by two to 585 rigs this week, previously at a three-month low (Figure 2, left). Drilling activity has remained at reduced levels for the past 10 months, recently slipping to a three-year low of 576 rigs in January

Canadian drilling continues to seasonally decline following its winter peak. Total oil and gas rig counts fell by four this week to 134 (Figure 2, right). Canadian activity typically surges in January and February, then declines through April as thawing ground conditions limit access to roads and drilling sites.

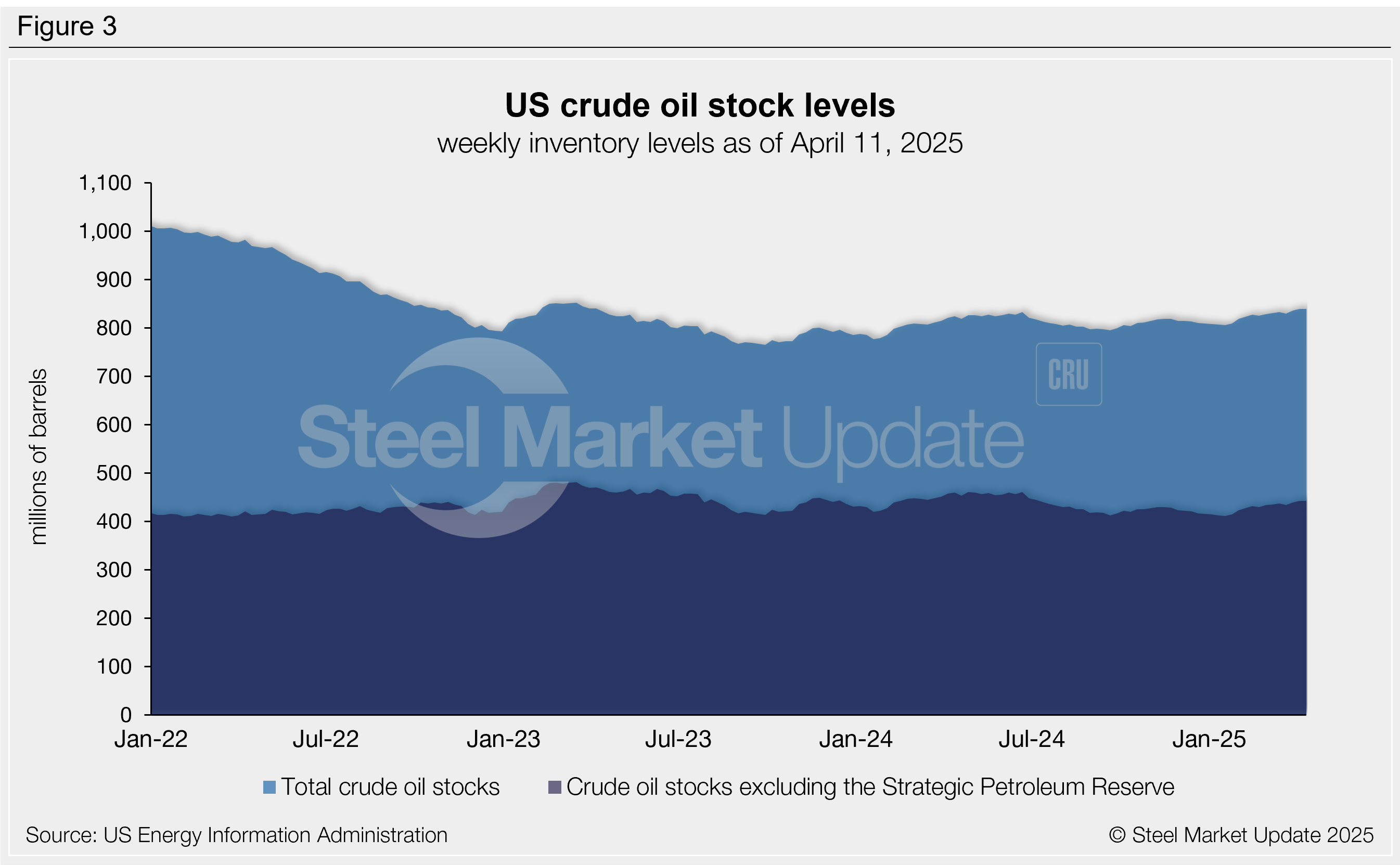

Crude stock levels

US crude oil stock levels have gradually recovered across 2025, rising to a two-year high last week of 840 million barrels. Stock levels are 4% higher than the start of the year and 2% higher than levels seen this time last year (Figure 3).