CRU

May 9, 2025

CRU: Tariffs set to dampen global auto growth

Written by David Leah

Key takeaways

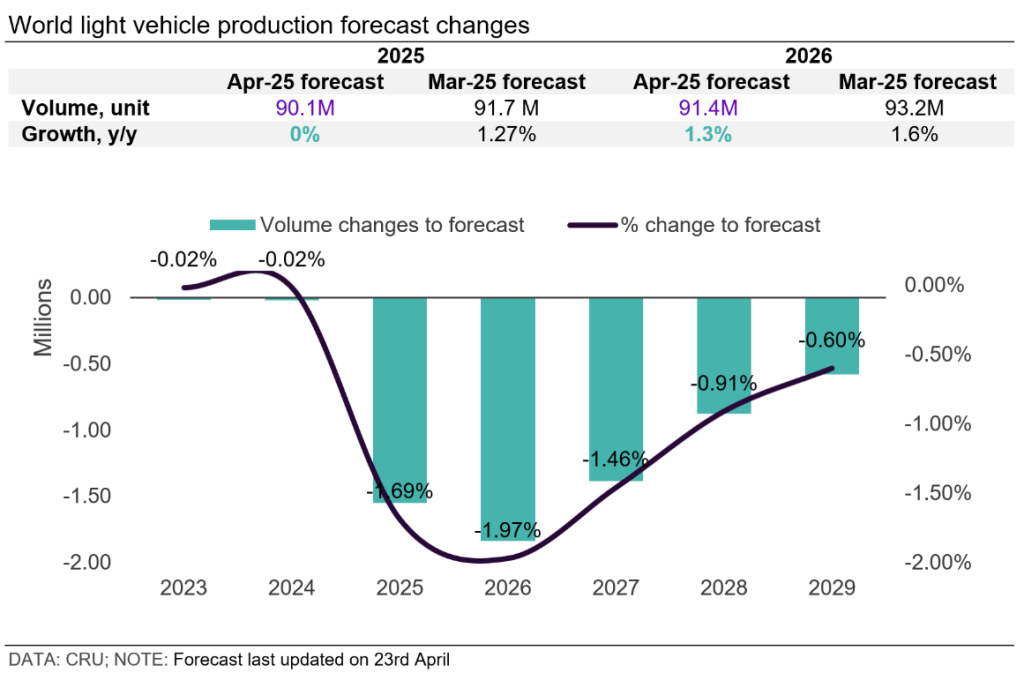

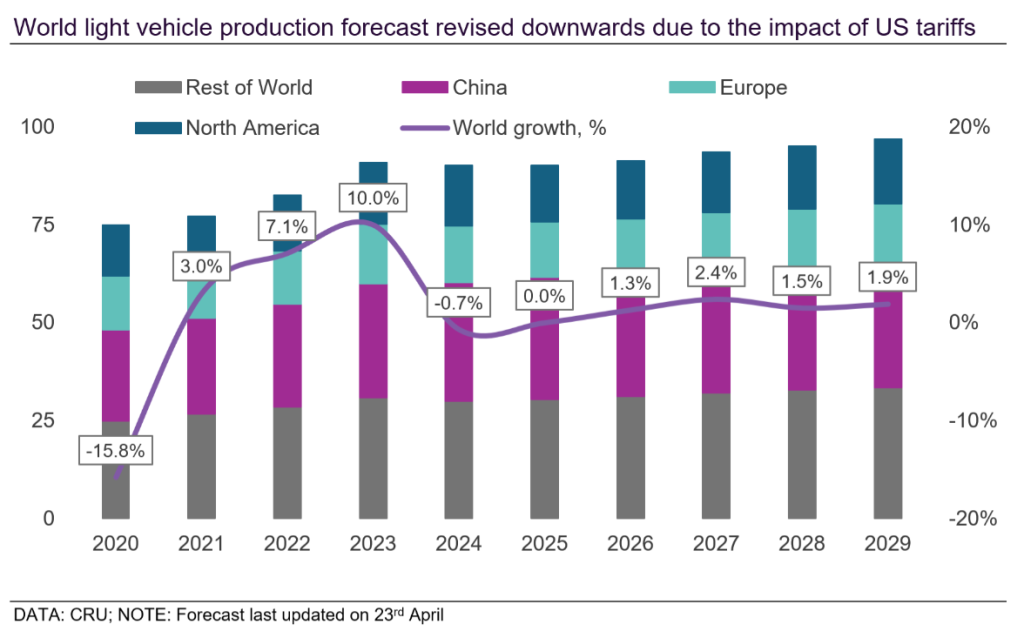

Global Production: The recently announced US tariffs on vehicles and key components from all markets are expected to significantly disrupt global production. We have significantly revised our outlook downward for the short to medium term. Markets with high exposure to the US, such as Mexico, Canada, South Korea, Japan, and Europe, are likely to experience weaker output. China, India, and Brazil are expected to drive global growth this year.

EV Demand: Though we have revised our EV forecast downward, China is expected to see robust EV growth this year, supported by favorable government policies. Proposed changes to the 2025 EU emission standards have led us to downgrade our EV outlook for the region, though double-digit growth is expected. In North America, the new tariffs are set to weaken overall vehicle demand, including EVs, by driving up prices.

Key Risks: Rising protectionism and prolonged imposition of US tariffs pose a significant downside risk. Additionally, retaliatory measures could further escalate tensions, impacting global trade. However, the US administration appears willing to renegotiate certain trade terms with partner nations and offer flexibility for US-built vehicles, which presents a potential upside risk.

Forecast revised downward since last update

Production outlook revised down in US and markets with high exports to the US

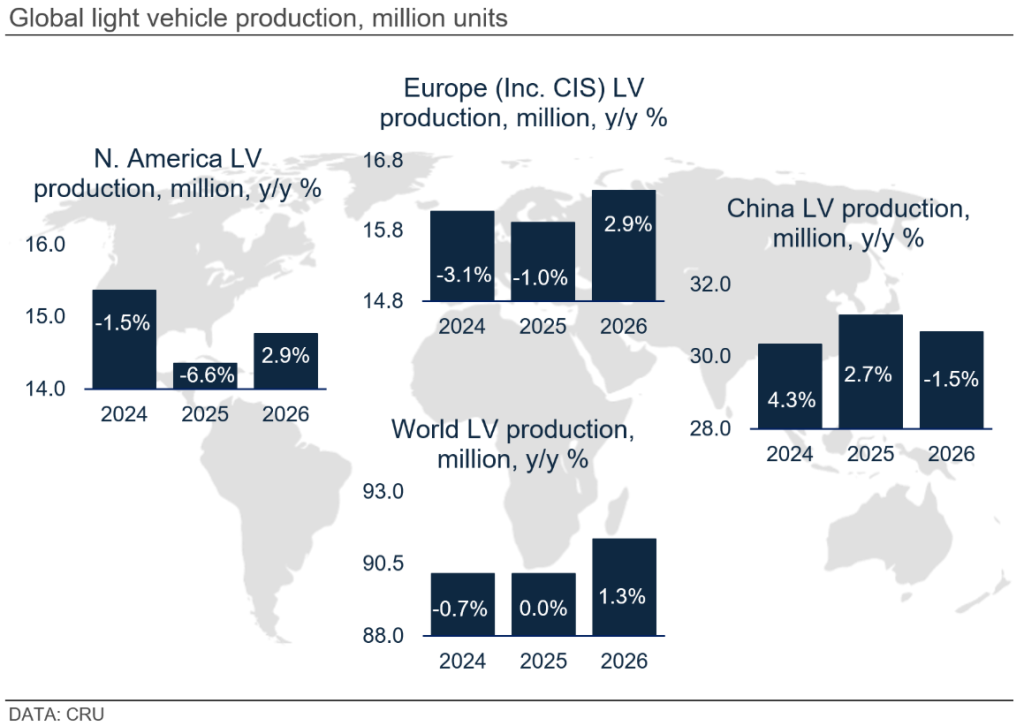

The global light vehicle production forecast has been revised downward, due to the rise in trade tariffs. Global output is expected to be flat this year, with declines in North America and Europe offset by growth in China, which is being boosted by government policies designed to stimulate consumption.

In North America, tariffs will increase costs and disrupt supply chains in the short to medium term, impacting both production and demand. As a result, we expect significant declines in production and sales this year.

The 25% tariff on fully assembled vehicles (with exemptions for US value-added content in USMCA-compliant vehicles), along with a 25% tariff on non-USMCA parts (with an allowance for up to 15% of a vehicle’s value in non-compliant parts used in US-built vehicles), is expected to significantly disrupt regional production.

However, recent concessions by the US administration, such as largely eliminating tariff stacking, exempting USMCA-compliant vehicles from the parts tariff, and providing rebates on the value of imported parts, offer some relief to automakers and present upside to our current base case.

In Europe, we have revised our production forecast downward, with output now expected to decline by 2% y/y (down from a 1% decline in our previous forecast). This will be the second consecutive year of declining output. The European auto sector continues to struggle amid weak consumer demand, rising competition, elevated vehicle prices, and a challenging economic and political environment that has eroded consumer confidence.

European OEMs face multiple headwinds, including trade tariffs, increasing costs, and excess capacity, which are prompting restructuring and resourcing efforts alongside calls for government support to improve competitiveness. The imposition of additional US-related tariffs is expected to further weaken regional production.

In China, vehicle production is expected to grow by around 3% y/y, driven primarily by domestic demand. Sales continue to be supported by the trade-in policy, local incentives, EV tax exemptions, and intense competition that keeps prices low. Although newly imposed US tariffs on Chinese automotive goods are not expected to significantly affect overall vehicle production, they may impact the sourcing of certain components and pose a downside risk by potentially weakening consumer confidence. Nonetheless, we expect relatively strong growth in China this year.

Key trends impacting the automotive industry

Rising protectionism: The US administration has imposed a 25% additional tariff on imported vehicle and key components. For USMCA-compliant vehicles, the tariff may be reduced based on the value of the US content. Canada and China have already responded with reciprocal tariffs. There is a growing risk this could escalate into broader protectionist measures.

EV policy rollback: The Trump administration has taken steps to begin rolling back the IRA tax credits, as well as EPA and CAFE regulations. These changes are expected to dampen EV demand and reduce compliance pressures on automakers, prompting a shift back toward ICE vehicles.

Pressure on EU policymakers: The European Commission has proposed a more flexible approach to meeting emissions standards. This would allow automakers to meet the targets over a three-year period, instead of one, helping them avoid fines. This change would ease the pressure to prioritize BEV sales as aggressively in 2025.

Competition in China: While the price wars in China this year have been relatively mild, competition remains intense. This will lead to market consolidation in the future. Foreign brands are struggling to compete, particularly in the EV segment. As a result, some automakers may re-strategize, exploring options ranging from exiting the market to strengthening partnerships with local brands.

Chinese expansion: Chinese carmakers are poised to expand their global footprint. A reversal of historical trends is possible, with western OEMs potentially forming joint ventures with Chinese brands in western markets or even selling underutilized plants to Chinese automakers seeking to localize production.

Rise of the plug-in hybrids: Plug-in hybrids have seen a resurgence in popularity in China. Several pure-play BEV manufacturers have announced plans to introduce plug-in hybrid models. Outside of China, some legacy automakers are also planning to launch plug-in hybrids in the US and other markets.

Opportunity for Chinese carmakers in Europe: While plug-in hybrids are set to be phased out in the EU by 2035 due to the effective ICE ban, EU regulations are encouraging larger batteries in the latest generation of PHEVs. Additionally, the recent increase in EV tariffs on China-made EVs does not apply to PHEVs, presenting a short- to medium-term opportunity for Chinese automakers. This would allow them to offset some of the additional costs on their BEV lineup caused by higher BEV import duties.

North America: Trade tariffs set to disrupt sales and production

Impact of US tariffs on automotive industry

Since taking office, the new US administration has imposed a range of tariffs, including an additional 25% on aluminum and steel imports, a 25% tariff on fully assembled vehicles (with exemptions for US value-added content in USMCA-compliant vehicles), and a 25% tariff on non-USMCA parts (with an allowance for up to 15% of a vehicle’s value in non-compliant parts used in US-built vehicles). These tariffs are expected to drive inflation, disrupt supply chains, and increase costs for automakers and suppliers.

There are signs that this policy is already having an immediate impact on OEM strategies and build rates. Some carmakers have temporarily suspended production, both domestically and abroad, as they readjust their planning to the new tariffs. In addition, several manufacturers are seeking to increase output of domestically built models to reduce their exposure to the tariffs.

Our current base case assumes that the 25% tariff on fully built vehicles will remain in place for the foreseeable future. However, we think there could be some scope for new trade deals, which would reduce trade tariffs for some countries and export focused OEMs.

Some concessions may be made on the component tariffs due to their complexity and the potential negative impact on US built vehicles. The administration has already signalled a delay in counting only the US-content in USMCA-compliant vehicles, which was initially expected to take effect from May 3. Further changes include some tariff relief and rebates on parts, as well as confirmation that tariffs will not be stacked. As a result, there is some upside risk, but the near-term outlook remains bleak.

The impact on production is expected to be immediate, with carmakers that have a lower domestic footprint being the most exposed. We anticipate the effect on demand will materialize over the coming months rather than immediately, as consumers may rush to buy vehicles before price increases take hold, and as day supply remains elevated, boosting sales. Nonetheless, we expect sales to decline this year, with most of the impact occurring in the second half.

Over the medium to long term, some carmakers are likely to increase their domestic demand but demand is expected to remain subdued, which will weigh on production. There is some upside potential, particularly given the administration’s apparent willingness to adjust policy to support domestic manufacturers and be open to renegotiating the balance of trade with some nation states.

North American short-term production

The Federal Reserve Board reported a 9% seasonally adjusted annual rate decline in US vehicle production in March 2025, marking the fifth consecutive y/y decline in the monthly selling rate.

Meanwhile, GlobalData estimates that output declined by 4% y/y in March. First-quarter results have been mixed across OEMs, with some carmakers experiencing production slowdowns due to model changeovers, while others have seen strong growth from new model ramp-ups.

Overall, US vehicle production fell by approximately 8% in 2025 Q1. Further, sharper declines are anticipated in the coming months as carmakers feel the effects of tariffs, including supply disruptions and increased costs.

Cox Automotive reported US vehicle inventories at 2.69 million units at the end of March, around 10% lower than at the start of the month. Inventory levels have dropped significantly as consumers rushed to purchase vehicles ahead of anticipated price increases. As a result, new car sales rose by 11% y/y in both March and April.

We expect fewer incentives to be offered in the coming months as inventory tightens. While prices are broadly expected to rise, immediate pricing trends have varied by OEM, a number of carmakers waiting until the end of May before making a move.

Mexican automotive production grew strongly in March, following modest gains in the first two months of the year. The production increase came ahead of the implementation of new US tariffs. Meanwhile, domestic demand in Mexico cooled in March, growing by just 1% y/y. However, hybrid and EV sales posted double-digit growth, driven by improved charging infrastructure and stronger consumer interest in these powertrain types.

The recent imposition of a 25% tariff on Mexican imports is expected to weaken domestic production, given the increased costs and Mexico’s heavy reliance on exports to the US. However, the current exemption on USMCA-compliant parts should provide some relief. We expect carmakers to re-strategize to mitigate the impact of tariffs, which could result in some production being relocated, particularly for models destined for the US market.

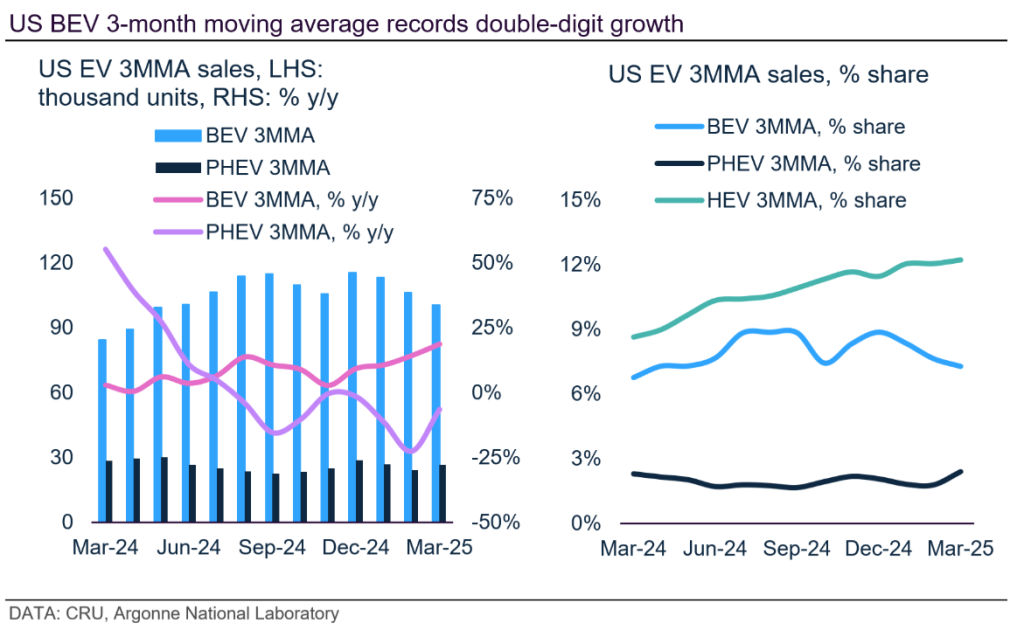

US BEV trends and outlook

Despite ongoing policy uncertainty, BEV sales grew strongly in the first quarter of 2025, driven by expanded model availability and a surge in demand ahead of the anticipated removal of the IRA tax credit and ahead of potential price rises due to the implementation of tariffs. Growth was also amplified by a low base.

We expect the US BEV market to continue expanding in 2025, although at a significantly more moderate pace, with BEVs likely to be disproportionately affected by the tariffs. The expected slowdown reflects anticipated rising BEV prices due to tariffs. In addition the increasing likelihood that the administration will rescind the IRA consumer tax credit, which may have brought forward purchasing into 2025 Q1, and weaken EPA emissions standards. Since taking office, the Trump Administration has rolled back the national EV target and paused funding for charging infrastructure programs.

We have revised our forecast to reflect these likely policy changes. We now expect slower growth for BEVs and xHEVs, while increasing the projected ICE vehicle share. Despite this, we still foresee an upward trajectory for BEVs over the forecast horizon, although at a reduced pace.

Europe: Production faces a perfect storm

European short-term production analysis

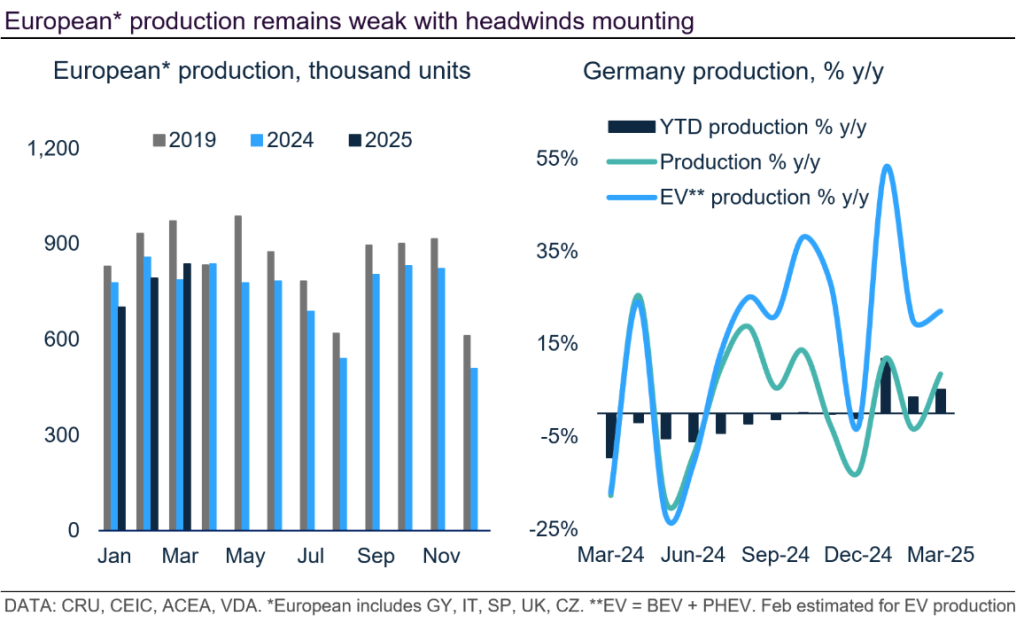

Using the latest actuals from Germany, the UK, Spain, Italy, and the Czech Republic as a proxy for European production (see chart below), Europe declined by 4% in Q1. Vehicle production remains subdued, weighed down by economic and geopolitical headwinds that continue to dampen consumer confidence.

Yet, production picked up in March, growing 6.5% y/y. This growth was inflated by a low base in 2024 due to model changeovers and the timing of the Easter holidays, which resulted in fewer working days. Nonetheless, several markets recorded a marked increase in exports during March, with some frontloading shipments to the US ahead of the implementation of new tariffs.

The recently imposed 25% US tariffs on vehicles and key components are expected to significantly impact export volumes in the coming years. Some carmakers have already suspended exports to the US as they assess their medium- to long-term strategies. As a result, we expect European production to decline by around 2% y/y in 2025, further exacerbating pressure on domestic automakers, many of whom are already grappling with excess capacity.

Automakers will likely respond by reducing vehicle exports to the US, increasing prices, and prioritizing models built locally. In the short to medium term, they may also consider shifting more production to the US, while focusing on domestic and alternative export markets to offset losses and boost output.

Meanwhile, an impending US-UK trade deal will be welcomed by UK carmakers. Several premium OEMs, such as Jaguar Land Rover, are heavily reliant on the US market and with no manufacturing footprint in the US are especially vulnerable to the new tariffs.

Separately, the recent UK-India trade deal is a positive development for the UK automotive industry. Tariffs have been slashed from over 100% to 10%, under a quota system, offering some carmakers new export opportunities and making the UK a more attractive destination for investment.

The European Commission has announced plans to support the industry, particularly by easing and unveiled plans to incentivise local production of battery cells and components. The extent of this support will determine its impact on domestic production.

The commission also intends to introduce incentive measures to boost BEV demand, including promoting social leasing schemes for BEVs, accelerating the adoption of BEV corporate fleet vehicles, and expanding the rollout of charging infrastructure over the forecast period. These efforts are expected to stimulate demand.

European short-term sales analysis

Total light vehicle sales across the “Big 5” Western European markets (Germany, France, the UK, Italy, and Spain) grew y/y in March 2025, following two consecutive months of decline. However, results were mixed.

France recorded the most significant y/y decline due to changes to its bonus-malus scheme in February, which pulled demand forward into that month. Meanwhile, Spain and the UK posted strong growth. Spain benefited from robust private vehicle demand, supported by the Restart Auto+ aid program, which offers grants of up to €10,000 for vehicles affected by the floods in Valencia. In the UK, sales were boosted ahead of changes to EV excise duty (road tax) set to take effect in April.

Despite the March uptick, overall European demand remains under pressure from weak consumer confidence, high vehicle prices, and ongoing economic and geopolitical challenges. However, an increase in new model launches and rising competitive pressure may begin to exert downward pressure on prices, although we still expect overall sales to decline y/y in 2025.

European BEV trends and outlook

European BEV sales continued to show positive momentum in March, even as the overall automotive market remains subdued. Most markets recorded solid BEV growth, supported by recent model launches and more aggressive pricing. Still, the broader outlook remains uncertain. The European automotive industry is facing a perfect storm of weakening demand, rising competition, geopolitical risks, and increasing costs.

In response to these pressures and growing stakeholder concerns, the European Commission has proposed an action plan to support domestic manufacturers. The plan includes several measures, such as a more flexible approach to emissions targets, allowing carmakers to average their emissions over a three-year period instead of one.

While this softens the average fleet emissions requirements for this year, we still anticipate double-digit BEV growth in 2025. Automakers must continue to manage their emissions performance, even under the more relaxed framework. Furthermore, the introduction of more affordable, high-volume models, increasing competition from Chinese brands, and the UK’s Zero Emission Vehicle (ZEV) mandate will continue to drive BEV sales growth.

China: EV sales set to continue to accelerate in 2025

China short-term sales analysis

According to the China Association of Automobile Manufacturers (CAAM), passenger car wholesales grew by 36% m/m and increased by 10% y/y in March. Meanwhile, the China Passenger Car Association (CPCA) reported domestic sales rose 14% y/y.

Domestic demand remains strong, supported by favorable local and national incentives, such as the trade-in policy, and more accessible financing options for buyers. As a result, we have marginally increased our sales forecast for the year by 50,000 units and expect the market to grow by 3.6% y/y.

However, the recent imposition of tariffs by the US on Chinese imports could dampen consumer confidence and have a knock-on effect on vehicle demand, though we expect the impact to be relatively mild.

China exported around 116,000 vehicles to the US last year, a small share of its total vehicle exports (around 2%). As such, we do not anticipate a significant effect on automotive production. However, the tariffs on components and parts are expected to have broader implications, particularly for US-based suppliers and carmakers. Consequently, we still expect vehicle production in China to grow by around 3% this year, driven largely by robust domestic demand.

China BEV trends and outlook

BEV sales continued their strong start to the year in March 2025, registering y/y growth of over 50%. BEV market penetration also reached its highest level this year, with BEVs accounting for just under 30% of all light vehicle sales in China last month. Although PHEV sales continue to rise, the pace of growth has cooled compared to the second half of 2024.

Despite ongoing global geopolitical uncertainty, we remain optimistic about overall automotive and NEV growth in China this year. Consumer sentiment remains strong, and the market will be supported by local and national incentives, including the continuation of the trade-in policy and the NEV purchase tax subsidy, which will decrease from 10% to 5% in 2026.

While competition remains intense, the price war has been relatively mild compared to last year, with fewer overall price cuts for EVs. However, promotional discounts for ICE vehicles have increased, as carmakers seek to boost demand for this powertrain type and regain market share.

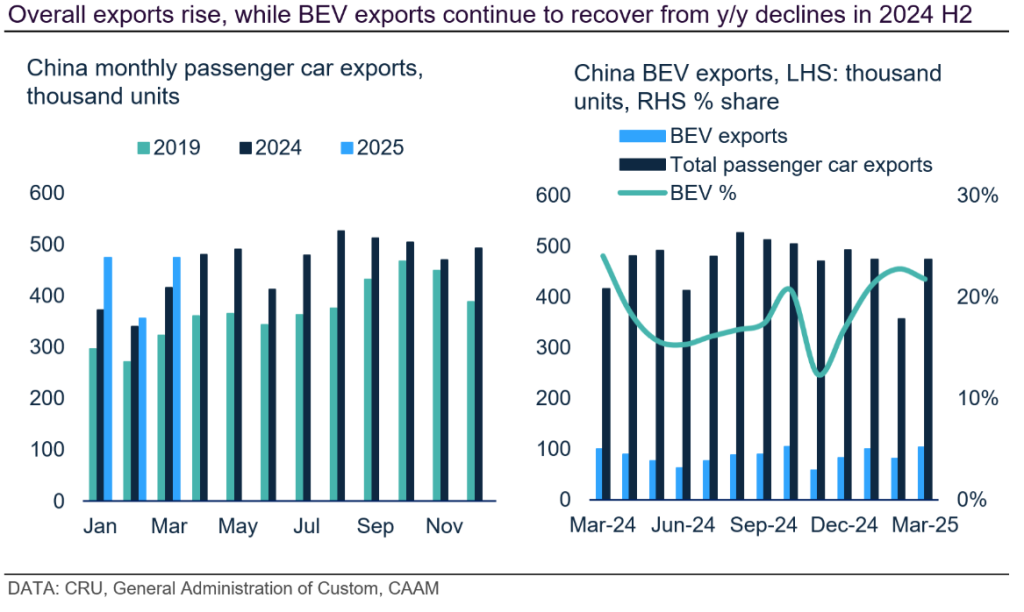

BEV exports are showing signs of recovery after y/y declines in the second half of last year, as automakers continue to expand their footprint in foreign markets with favorable tariffs, such as the UK. Interestingly, carmakers are also prioritizing other powertrains, such as plug-in hybrids, which face lower tariffs than BEVs in the EU for instance.

Inventories

The Vehicle Inventory Alert Index increased 59.8% in April, reflecting both y/y and m/m increase. However, while the index remains above the 50% threshold, consumer demand continues to be supported by favorable policies aimed at stimulating consumer spending.

Beyond 2025, further details on the upcoming China 7 emission standards are expected to be announced. The MIIT has also introduced new fuel consumption and EV credit requirements for automakers for 2026 and 2027, with NEV credit ratios set at 48% and 58%, respectively.

While there is a surplus of credits due to significantly higher EV sales, some carmakers have struggled to meet EV credit targets. This will place additional pressure on them to prioritize EV production and further intensify competition.