Analysis

May 12, 2025

Apparent steel supply bounced back in March

Written by Brett Linton

The volume of finished steel entering the US market rebounded in March, according to our analysis of US Department of Commerce and American Iron and Steel Institute (AISI) data. Referred to as apparent steel supply, we calculate this monthly figure by adding domestic steel mill shipments to finished US steel imports and subtracting total US steel exports.

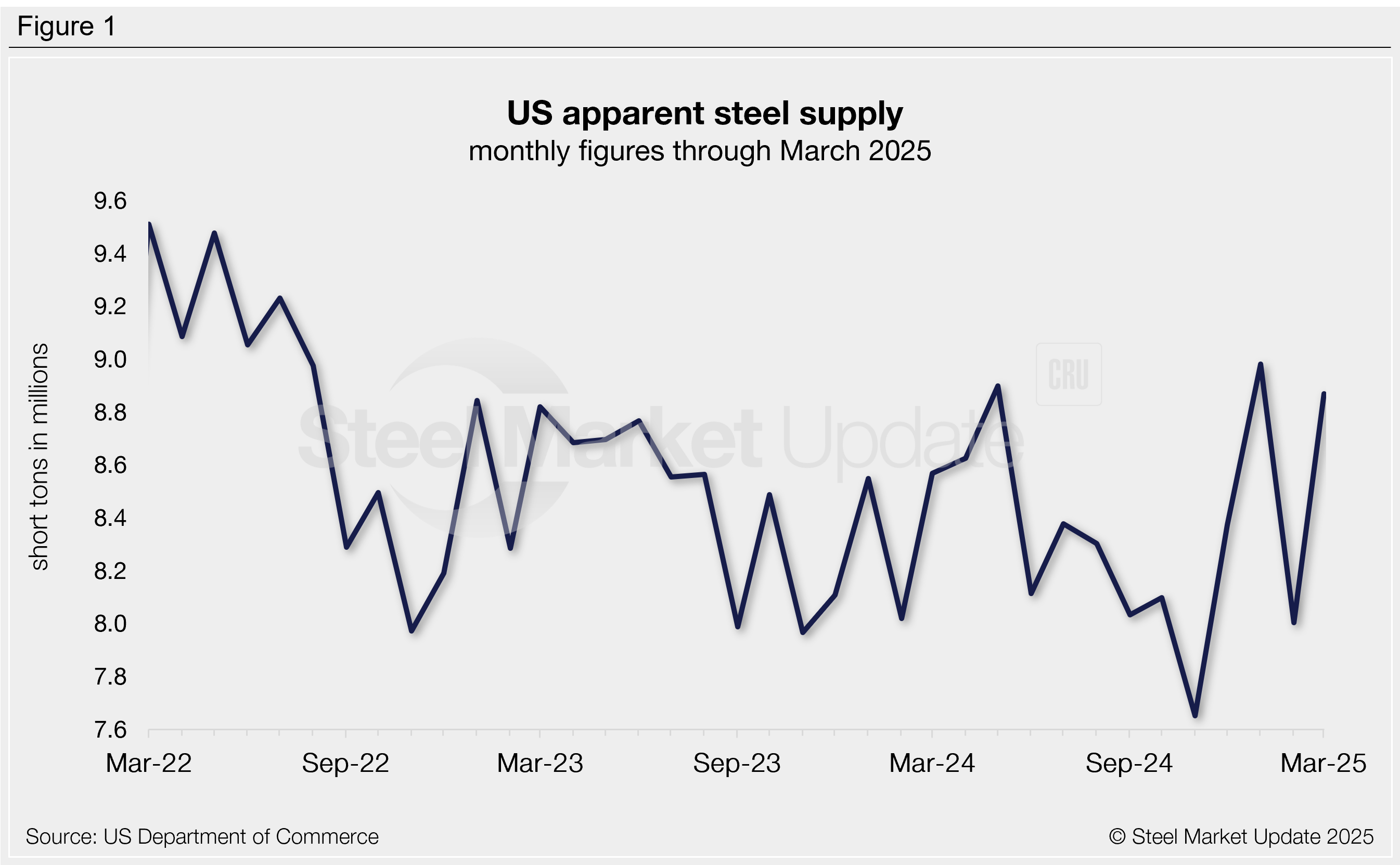

Apparent supply increased 11% month over month (m/m) in March to 8.87 million short tons (st), almost entirely reversing February’s dip. March supply is just 1% below the multi-year high recorded in January and 4% above March 2024 levels.

Supply has fluctuated within a stable range over the past two and a half years, averaging 8.40 million st per month during that time (Figure 1). However, volatility has increased in recent months. Supply fell to a near four-year low of 7.65 million st last November, then rebounded to a two-and-a-half year high of 8.98 million st in January. For context, the highest monthly supply in our 15-year data history was 10.90 million st in October 2014, while the lowest was 6.52 million st in April 2020.

Trends

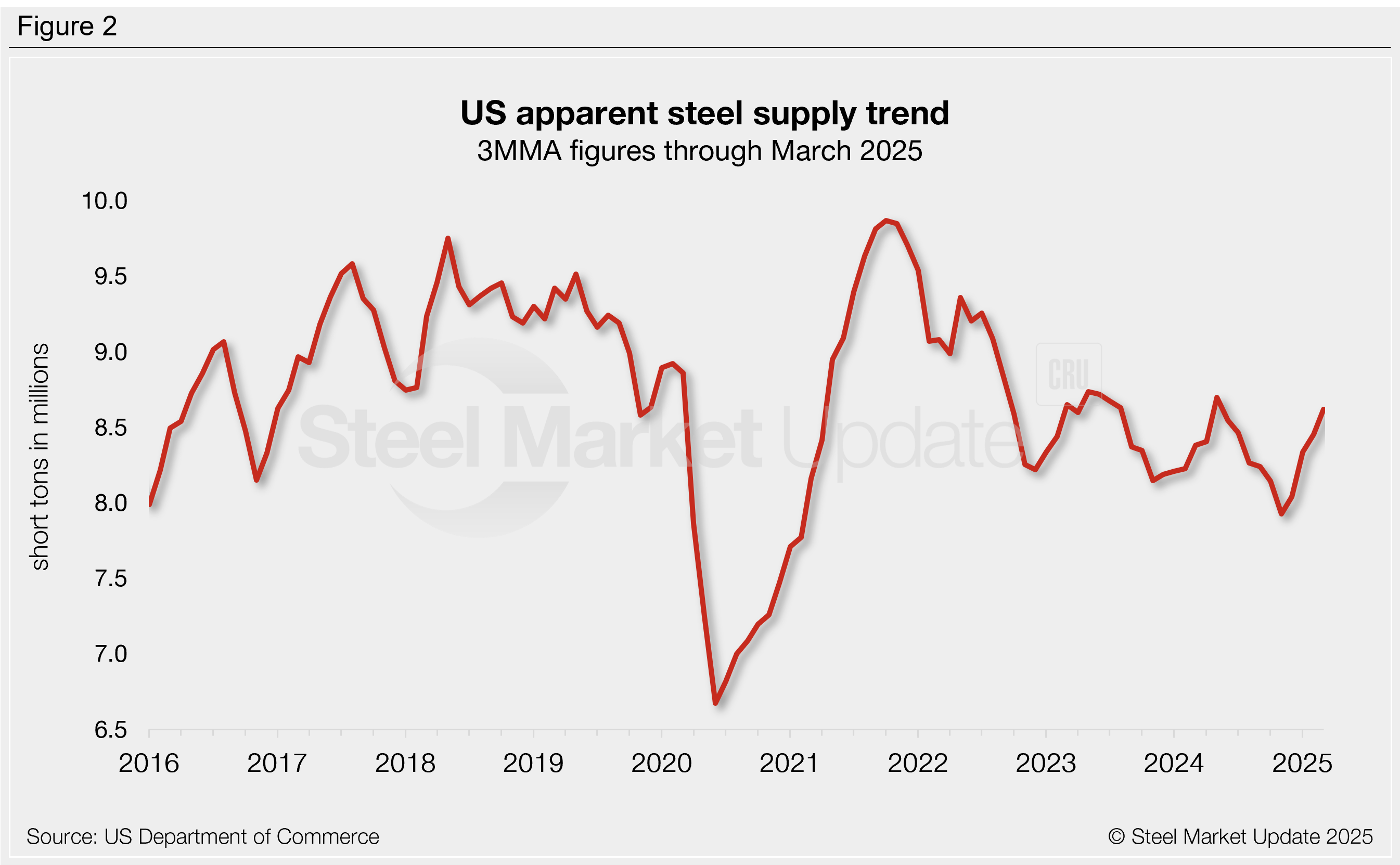

To smooth out monthly fluctuations and better highlight underlying trends, supply can be calculated on a three-month moving average (3MMA), as shown in Figure 2.

On this basis, supply generally trended lower following its late-2021 peak of 9.87 million st. The 3MMA increased in March for the fourth consecutive month to a 10-month high of 8.62 million st. This comes just months after the near four-year low 3MMA of 7.93 million st seen in November. One year ago, the 3MMA was marginally lower at 8.38 million st, and two years ago it was almost identical at 8.65 million st.

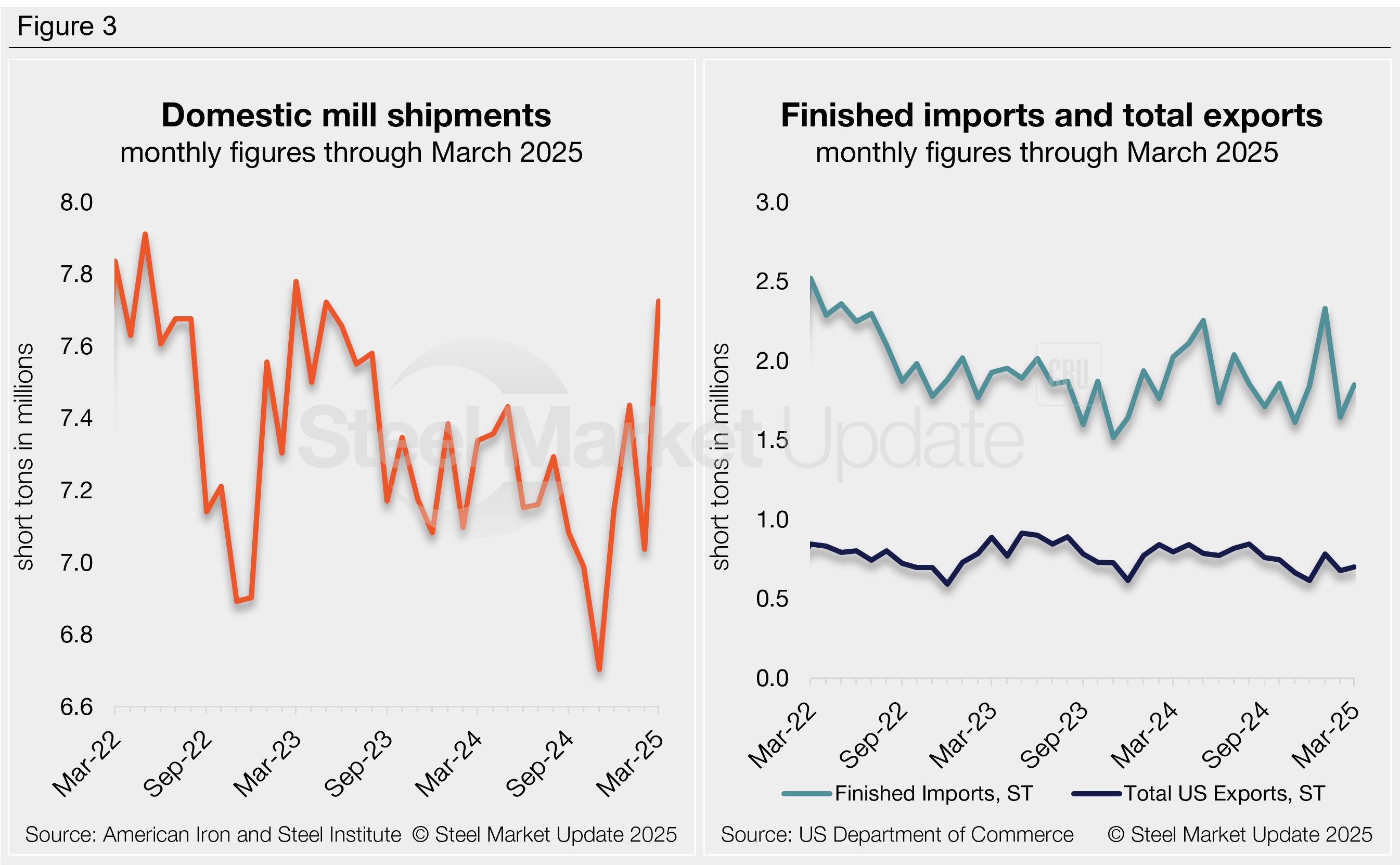

Figure 3 graphs the individual inputs for apparent supply, clearly showing that domestic steel mill shipments were the primary driver for March’s increase.

-Domestic shipments rose 10% (689,000 st) m/m in March to a two-year high, accounting for 87% of total supply.

-Finished steel imports increased 12% (201,000 st) in March.

-Steel exports ticked up 4% (24,000 st) from February, minimally offsetting the overall rise in supply.

-Net imports (finished exports minus exports) made up 13% of March’s supply, similar to the previous month (12%) and levels one year ago (14%).

To see an interactive graphic of our apparent steel supply history, click here. If you need any assistance logging into or navigating the website, contact us at info@steelmarketupdate.com.