Analysis

June 6, 2025

CRU Insight: A 50% S232 tariff will raise US steel prices and shift trade flows

Written by Josh Spoores & Juliana Guarana

The increase of Section 232 tariffs on steel to challenging levels will lead to significatively higher prices for end consumers in the US market. Higher cost suppliers will be affected most, both from weaker demand and alternative supply options.

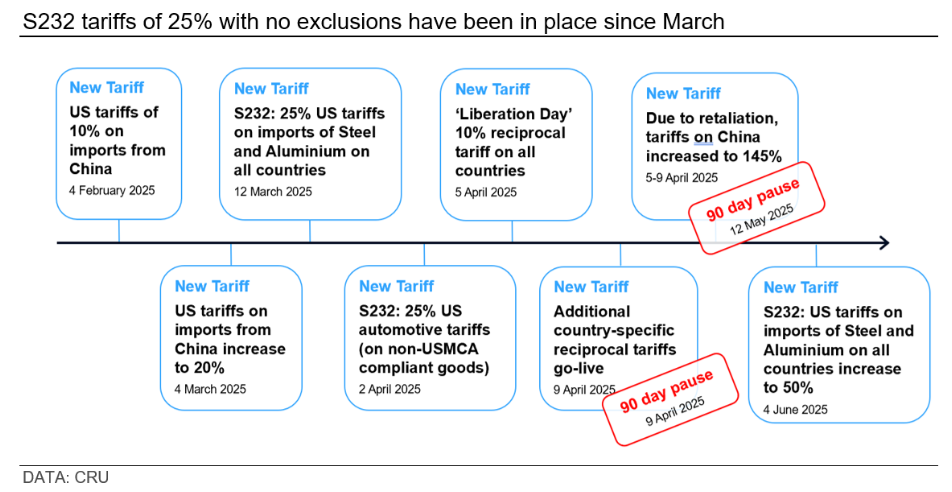

Section 232 tariffs on steel set to double from 25% to 50%

On Friday, May 30, US President Donald Trump announced that the current Section 232 tariffs on steel and aluminum imports will be doubled from 25% to 50%, effective from Wednesday, June 4. This announcement raised concerns about impacts on domestic manufacturers and end consumers, but no further details about potential exemptions or exclusions were provided (as of the June 3 publication date of this CRU Insight).

President Trump originally announced a reinstatement of the 25% S232 steel tariffs on Feb. 10. Tariffs were effective from March 12 with no country-wide exclusions.

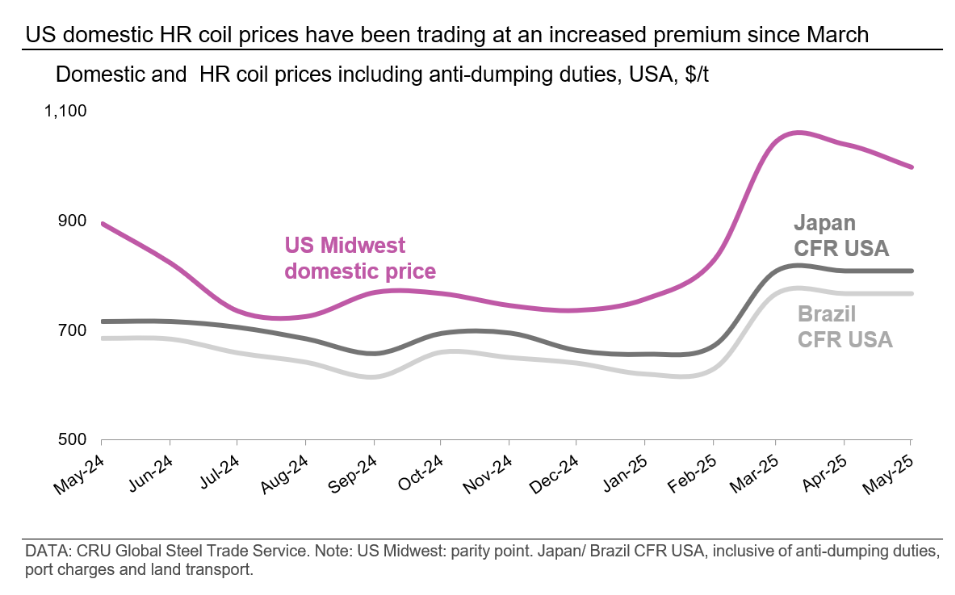

Since this announcement of 25% tariffs, domestic prices of HR coil – the largest and most volatile product in the USA – surged 37% from an average of $689 per short ton in January to an average of $945/st in April.

The US requires steel imports to meet domestic demand

The US is a net importer of steel as domestic production is not sufficient to meet demand. This will not change in 2025.

New capacity will come online in 2025, but the US steel market will still need imports. In 2024, imports accounted for 20% of finished and semi-finished steel demand. New domestic flat and long products capacity of nearly 5 million metric tons is planned to start up in 2025, but the US will still need approximately 16 million mt of imports split across plate, longs, and sheet markets (see related CRU Insight here). Some domestic idle capacity can be reactivated, but will be insufficient to fully meet the country’s demand.

US buyers are heavily reliant on imports for some high-value products that require specialist production facilities. One example is wire rod, particularly on specific grades such as tyre cord, where domestic capacity is limited. The revised Section 232, which took effect in mid-March, removed the previous exemption on tyre cord imports, and product-specific exclusions by company will be only in effect until their end date.

The increase of Section 232 tariffs to 50%, with no exemptions and exclusions, will translate into a steep rise in purchasing costs for steel buyers. This, in turn, will lead to significatively higher prices for end consumers in the US market. As a result, the ultimate impact of these tariffs is expected to lead to demand destruction in steel end-use sectors.

Higher US domestic prices mean import offers have been competitive since March

International shipments continued to flow into the US despite the 25% tariff introduced on March 12 on all steel imports from all countries, as domestic prices in the country rose substantially following the announcement of the Section 232 tariffs reset. The surge in domestic prices was driven by increased buying activity as market participants looked to secure material ahead of potential further price hikes due to sudden changes in US import policies.

As a result, while CRU’s US Midwest HR coil price was at $949/st in late March, import offers were reported to be in the mid-$700s (delivered duty paid). As the chart below illustrates, landed import prices of HR coil from key trade partners have remained well below US domestic prices since March.

According to CRU’s Global Steel Trade Service (request a demo here), in the third week of April, CR coil offers from Asia were available at $970/st DDP Houston, while domestic CR coil prices were assessed at $1,169/st. Import offers remained competitive relative to domestic pricing in May, with CR coil offers around $960/st DDP into Houston in the second week of May, while domestic prices were assessed at $1,125/st.

Higher-cost suppliers will be the most impacted by tariff increases

While steel consumers will be the most impacted domestically by the rise of Section 232 tariffs, the increased tariffs are also expected to reshape steel trade flows into the US market as the country’s demand for imports is likely to shift away from higher-cost suppliers towards more competitive options. However, not all lower-cost suppliers will have the capability to supply the high-value part of the product mix imported currently. For those high-value products, the risk is more from weaker demand and customers’ willingness to pay.

The biggest historical exporters to the US will face increased competition. Canada, Mexico, Brazil, the EU, South Korea, and Japan all benefited from exemptions to Section 232 tariffs prior to their reinstatement in March 2025. These countries will now have to compete on equal terms with countries that were never exempt, such as Turkey, Algeria, and Egypt.

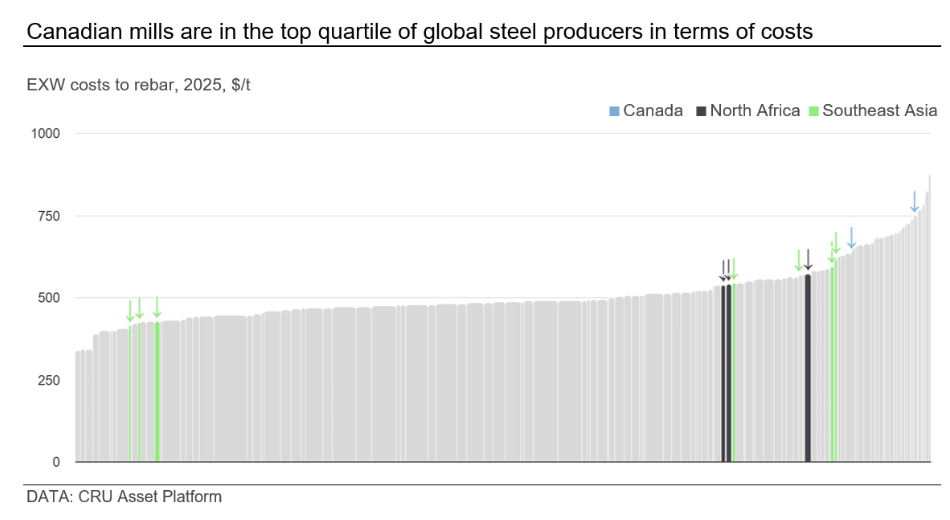

Canada is likely to be one of the most affected countries by the increase in Section 232 tariffs. The country is heavily dependent on the US market, with around 90% of its steel exports going to the US. Exports from Canada are skewed towards high-value products as production costs are high, so they are unable to compete with lower-cost exporters for commodity-grade products. This means their economic reach is low, and alternative exports will be challenging to find. Canadian mills are among the top quartile of global steel producers in terms of costs (see related Insight here), as illustrated by the chart below, taken from CRU’s Steel Asset Service (request a demo here).

As reported in CRU Global Steel Trade Service(request a demo here), some US longs’ import order volumes have already shifted away from Canada and Mexico towards countries such as Algeria, Egypt, Malaysia, and Vietnam, which are lower-cost suppliers that are now more competitive on price against previously exempt competitors.

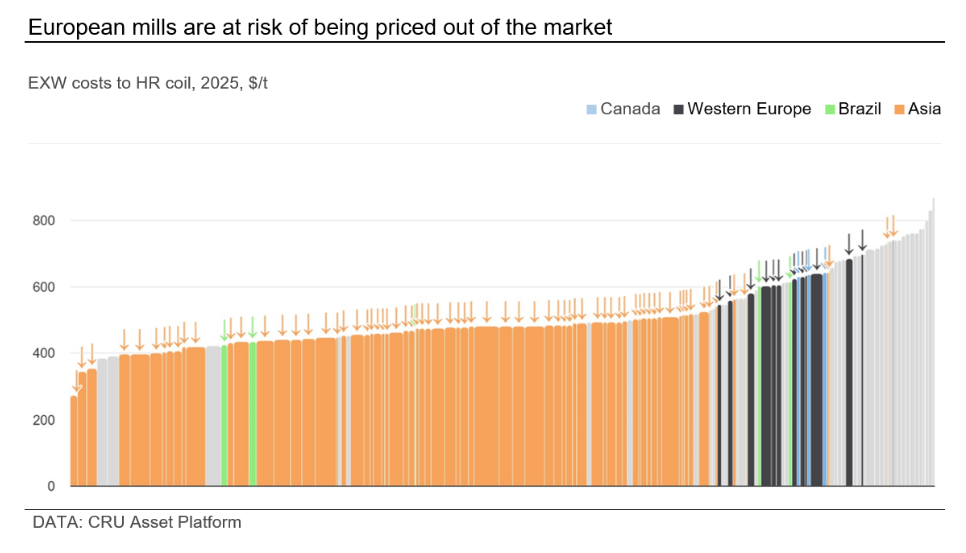

EU countries are also at greater risk of being priced out of the market, as European mills are less competitive than lower-cost Asian mills and may struggle to find an alternative sale within economic reach. The European Commission issued a statement following President Trump’s latest announcement, declaring that the region is prepared to impose the countermeasures announced on April 14 if no negotiated solution is reached.

Since the Section 232 tariffs’ increase will pose significant challenges to steel supply chains, end consumers, and historical trade partners, some negotiation to lower or eliminate tariffs is expected to take place. Country-specific reciprocal tariffs announced in April have been temporarily paused to allow talks to proceed, while the UK was the first country to secure a zero-tariff deal with the US (still subject to signature) on steel and aluminum on May 8.

Global Steel Trade Service will continue to monitor this evolving situation closely, and we will adjust our forecasts as events develop.

This Insight piece was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.