Final Thoughts: Are we nearing peak steel market tightness?

Could we see prices continue to inch higher, plateau, and then start to slide back? A lot hinges on whether and how long it takes mills to catch up on orders.

Could we see prices continue to inch higher, plateau, and then start to slide back? A lot hinges on whether and how long it takes mills to catch up on orders.

With global capacity projected to increase by 138 million mt by 2028, the gap between capacity and demand will continue to grow over the next three years. And that assumes the conflict in Iran does not stifle global demand.

Prices for iron ore, aluminum, pig iron, and shredded scrap have all risen in the last 30 days. Busheling scrap held steady, while zinc and coking coal declined.

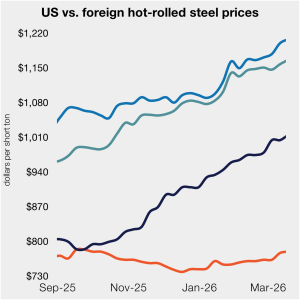

CR imports from Germany, Italy, and Japan on a landed basis remain much more expensive than domestic product. But South Korean imports remain competitive, in theory, even with the 50% Section 232 tariff.

Turkish steelmakers entered the scrap market after returning from the Ramadan holiday.

The pig iron market in Brazil has been quiet lately. There have been few bids or offers made by market participants.

The price gap between US hot-rolled coil (HR) and landed offshore product remained within a tight band this week. The dynamic continues as both stateside and offshore prices have trended higher.

North American auto assemblies gained ground in February, up more than 8% vs. January, but still down more than 4% year on year (y/y), according to GlobalData.

SMU’s Mill Order Index (MOI) eased in February. The result came as a marginal increase in service center intake levels was offset by higher shipments, according to our latest service center inventories data.

Sheet prices continue to inch higher. And people who once thought hot-rolled coil (HR) prices couldn’t go above $1,000 are now saying $1,100 doesn’t seem out of the question.

The pace of sheet and plate price increases slowed this week, with most products holding at some of the highest levels seen in over a year.

The bulk scrap export market into Turkey is starting to form after several weeks of inactivity.

Global raw steel production declined 3.7% from January to an estimated 141.8 million metric tons (mt) in February, according worldsteel data. Output was one of the lowest totals over the past three years.

The ongoing Middle East conflict, the resurgence of broad-based tariffs under Section 122 of the Trade Act of 1974, and the looming US midterm elections are not isolated developments. Rather, they form a kind of feedback loop in which each issue influences, and is influenced by, the others.

Since the Supreme Court ruled the IEEPA (reciprocal) tariffs imposed by the Trump administration were illegal, the subject of refunds has been circulating. A lower court has ruled refunds are due to importers affected by these tariffs, which amounted to an estimated $166 billion.

Plate market sources say the week has been quiet, but that overall, business remains consistent.

Steel buyers remain highly optimistic for their businesses’ chances for current and future success, according to SMU’s latest Steel Buyers’ Sentiment Indices.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

When nations eye their trade policy these days, are they only seeing tariffs? It might seem that way, especially after reading a presidential executive order or five over the last year. But is the condition spreading?

As spot prices for hot- and cold-rolled coils edge higher, mill capacity utilization rates hover below 80%, raising concern among some market participants.

Steel mill lead times extended to multi-year highs on both sheet and plate products this week.

Most steel buyers report that domestic mills are unwilling to negotiate price on new sheet and plate spot orders.

Freight rates have remained high in the US and Northern Europe, and there has been little or no activity in the Mediterranean region since our last export update on March 10.

Apparent steel supply increased from December to January, but remains on the low side compared to recent years.

US service centers’ flat-rolled steel supply declined for a second consecutive month in February, with shipping days of supply slipping to 52.2 on an adjusted basis, according to SMU data.

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

While decarbonization has fallen out of the headlines a bit, that doesn't mean it's gone away. Tariffs, geopolitical instability, outright war... there has been a lot to write about in the last year.

Heating and cooling equipment shipments declined in January to the second-lowest rate recorded over the past nine years.

The weather is still influencing the recycled metals market as we head into spring, sources say.

US steel exports jumped 33% in January but remain historically low, according to recently released US Department of Commerce data.