Oregon Steel and SSAB aim to push plate prices higher

Oregon Steel Mills and SSAB Americas announced higher plate prices to close out the week.

Oregon Steel Mills and SSAB Americas announced higher plate prices to close out the week.

The main impact on the ferrous value chain from the Middle East conflict will be the higher energy costs in a prolonged scenario.

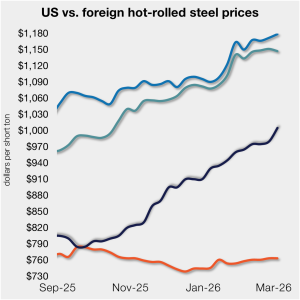

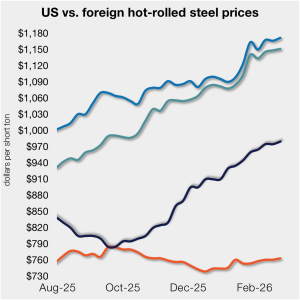

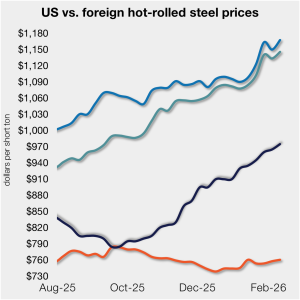

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week, as stateside tags continue to rise.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

Economic activity across the US increased at a light-to-modest pace in seven of the 12 Federal Reserve Districts, according to the US Federal Reserve’s latest Beige Book report.

Let’s say the going price for HR is around $1,000/st. Want to place a 1,000-ton spot order at that price? Good luck. It probably won’t be easy.

SMU's sheet and plate prices increased this week to new multi-month highs.

Crude-oil and natural-gas prices spiked, metals opened higher and some fertilizer benchmarks climbed after the US and Israel launched a “pre-emptive” strike on Iran, killing the supreme leader and plunging the region into chaos.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,005 per short ton (st), up $15/st from last week.

Sources in the domestic hot- and cold-rolled coil market said they are beginning to feel prices creeping up this week.

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product remained largely flat again this week, as price movements stateside and abroad mirrored each other.

Plate industry sources said the market has been characterized by three factors lately: fewer domestic mills willing to fulfill spot buys, inconsistent lead times, and erratic demand.

SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Even folks who had been firmly in what I’ll call the “February peak” camp now seem to agree that sheet and plate prices could move higher for longer than they anticipated.

Sheet prices continue to grind higher on tight supply and 'okay' demand. Plate finally saw some movement after weeks of stability as price increases begin to stick.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $990 per short ton (st), up $10/st from last week.

Global steel plate prices are expected to trend upward as North American restocking and European regulatory costs will drive the market, even as recovery in Asian markets remains gradual and cost-dependent.

The galvanized steel market is navigating price increases and longer lead times with a surer footing than in prior months.

Since late 2025, mills have begun to hold a firmer stance on prices, tightening their grip at the start of this year and holding on since

Once wintery weather gives way to sunnier spring conditions, plate sources foresee the market accepting the $50-60 per short ton spot price increases issued by Nucor Plate Group, Oregon Steel Mills, and SSAB.

Three of SMU’s price indices increased this week, while two remained steady, all holding at multi-month highs.

SSAB Americas wants to increase plate prices by at least $60 per short ton, $10 more than rival Nucor’s price hike last week.

Nucor increased its list price for hot-rolled (HR) coil to $980 per short ton (st) on Monday, up $5/st from last week.

Nucor on Friday announced plans to increase plate prices by $50 per short ton (st).

CRU: US Midwest sheet prices have continued to rise from our mid-January assessment.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

SMU’s sheet price indices inched up to new multi-month highs this week, while plate prices held steady.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $975 per short ton (st), up $5/st from last week.

Plate market participants expect domestic producers to issue a $40-60 per short ton (st) price increase.