HRC vs. plate price spread narrowing but still high

The premium plate has held over hot-rolled coil (HRC) has been narrowing but remains elevated compared to historical levels.

The premium plate has held over hot-rolled coil (HRC) has been narrowing but remains elevated compared to historical levels.

The LME three-month price was broadly stable on the morning of Jan. 19 and was last seen trading at $2,170 per metric ton (mt). The $2,200/mt level is now acting as a resistance it seems, but the break of the previous support level has not inspired a sell-off, at least not for now.

When I started in the scrap business many years ago as a rookie trader in Luria’s Cleveland office, I saw an industry composed of family-owned businesses stretching across a great industrial nation.

While there was little change in economic activity since its last update, the Federal Reserve reported declines in manufacturing in nearly all districts in its January Beige Book update.

Much discussion has centered on HRC futures and option liquidity. The perceived lack of liquidity is often used as a reason for not engaging in risk management, a profound folly in our opinion. Looking back over the last decade, the futures market has seen increased volume. The HRC futures volume in 2023 was 617% of 2013 numbers.

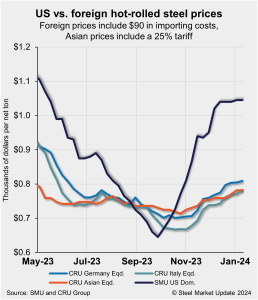

US hot-rolled coil (HRC) prices edged down this week while import prices moved higher on average. Domestic hot bands’ premium over cheaper imports declined as a result. But overall, US product remains substantially more expensive than overseas material. All told, US HRC prices are 21.4% more expensive than imports, a premium that is down three […]

What are people in the steel marketplace talking about this week?

Domestic buyers of steel sheet said mills were much more willing to negotiate spot pricing this week, according to our most recent survey data.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed slightly this month, according to SMU’s most recent pricing data.

There seems to be a growing consensus that the US sheet market has peaked at a high level and could begin losing ground from here. Whether declines happen quickly or whether sheet prices bop around at current levels for a few weeks more is the primary question.

US hot-rolled (HR) coil prices fell noticeably this week for the first time since late September. SMU’s hot-rolled coil price now stands at $1,025 per ton on average, down $25 per ton from last week. Cold-rolled (CR) coil was unchanged at $1,325 per ton.

Domestic scrap prices ended up down slightly after a roller coaster of trading in January, scrap sources told SMU.

Coming out of a strong fourth quarter, galvanized steel market participants are reporting an above-average start to January and are cautiously optimistic for 2024.

US service center flat-rolled steel inventories surged in December with the seasonal slowdown in shipments. At the end of December, service centers carried 64.8 shipping days of supply, according to adjusted SMU data, up from 54 days in November.

For two consecutive months, the initial scrap prices didn’t attract the amount of scrap that mills needed. A Detroit area mill came in at $460 per gross ton (gt) for busheling, which was down $50 from last month and down $20 on shredded and plate and structurals (P&S). But I guess they did not know at the time another mill in the district bought scrap sideways. Needless to say, that order filled right away. SMU could not find any supplier who sold at down $50.

The spread between cold-rolled coil (CRC) and hot-rolled coil (HRC) prices jumped during the week of Jan. 8 as cold rolled tags continued to rise while hot rolled tags held steady.

It’s been a sloppy start to the year for domestic hot-rolled (HR) coil and ferrous scrap markets. One of the loudest things to happen in HR this year might be something that didn’t happen at all. Namely, Nucor didn’t follow competitor Cleveland-Cliffs higher when Cliffs announced a price hike to start the year.

After a holiday period that saw HR futures volumes somewhat muted in December, the first week of January brought with it increased interest reflected in higher volumes.

SMU polled steel buyers on a variety of subjects this past week, including inventory, demand, steel sheet prices, imports, and what people are talking about in today’s marketplace. Rather than summarizing the comments we received, we are sharing some of them in each buyer’s own words. We’d like to hear your thoughts, too! Contact david@steelmarketupdate.com to be […]

Pig iron prices rose month over month (MoM) in all major regions aside from Europe on improved buying. Demand in the US remains robust while market participants report that availability of Brazilian material increased after tightening a month prior. Meanwhile, Ukrainian export capacity increased due to greater access to temporary sea corridors.

US hot-rolled coil (HRC) prices were unchanged this week but remain significantly more expensive than offshore product. While imported hot band tags increased vs. last week, gains were marginal, keeping domestic HRC substantially more expensive than imports. All told, US HRC prices are 24.3% more expensive than imports, a premium that is down only slightly […]

I expected that we’d start off January with prime scrap prices modestly up if for no other reason than industrial activity typically slows down over the holidays. And mills’ appetite for scrap typically increases in anticipation of stronger Q1 order activity.

Hot-rolled (HR) coil prices remain in the holding pattern they've been in since mid-December, according to SMU pricing archives.

Steel prices continued to move higher last month on the back of repeated mill price increases after tags reached a 2023 low of $645 per ton in late September. Hot-rolled coil (HRC) prices ended December at an average of $1,035 per ton ($51.75 per cwt), rising by $112 per ton during the month.

The US Department of Commerce will likely be lowering the antidumping duty (AD) rates on imports of welded steel pipe from the UAE.

Commercial Metals Co. saw robust demand from the construction markets in its first fiscal quarter, which ended on Nov. 30, 2023.

I’d have been surprised if anyone told me just last week that the January scrap market might move lower. What we saw on Friday were offers. Not settlements. And no doubt there are still some twists and turns in store before we can say for sure which way scrap will go.

A Detroit-area mill entered the scrap market on Friday afternoon with the following offers: The Chicago area followed suit: Mills in the Great Lakes region sensed there was ample supply of most grades. Also, they all bought heavily last month and so had sufficient inventories to make this move, market participants said. Still, the move surprised […]

The International Trade Commission (ITC) held a hearing on Thursday, Jan. 4, to consider arguments for and against the imposition of antidumping and countervailing duties (AD/CVDs) on tin mill products from a handful of countries. Both sides made compelling arguments.

SMU polled steel buyers on a variety of subjects this past week, including purchasing practices, steel sheet prices, scrap, and the future market.