Prices

May 12, 2016

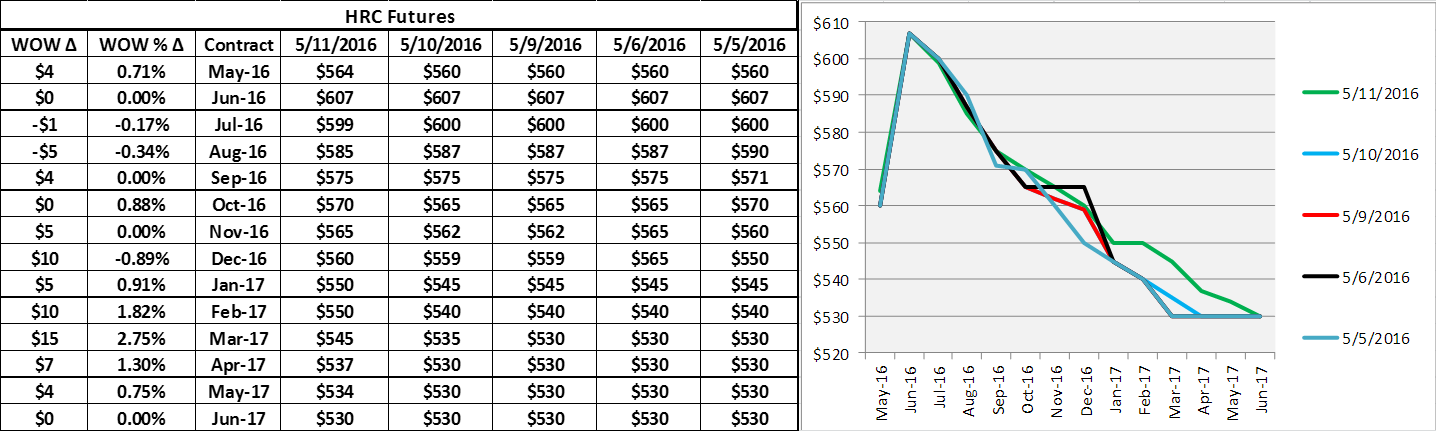

Hot Rolled Futures: Backwardation Spread Increasing

Written by David Feldstein

The following article on the hot rolled coil (HRC), busheling scrap (BUS), and financial futures markets was written by Dave Feldstein. As Flack Steel’s director of risk management, Dave is an active participant in the hot rolled coil (HRC) futures market and we believe he will provide insightful commentary and trading ideas to our readers. Besides writing Futures articles for Steel Market Update, Dave produces articles that our readers may find interesting under the heading “The Feldstein” on the Flack Steel website www.FlackSteel.com.

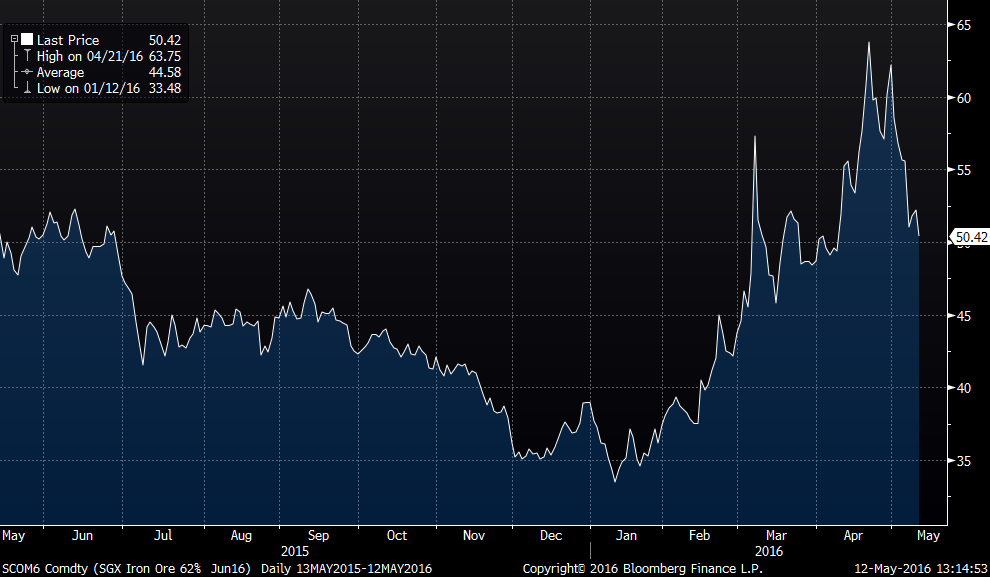

Iron ore futures continue to come off following restrictions placed on Chinese futures exchanges to limit speculation. The June iron ore futures price is down 21 percent to $50.42/t from $63.75/t on April 21st.

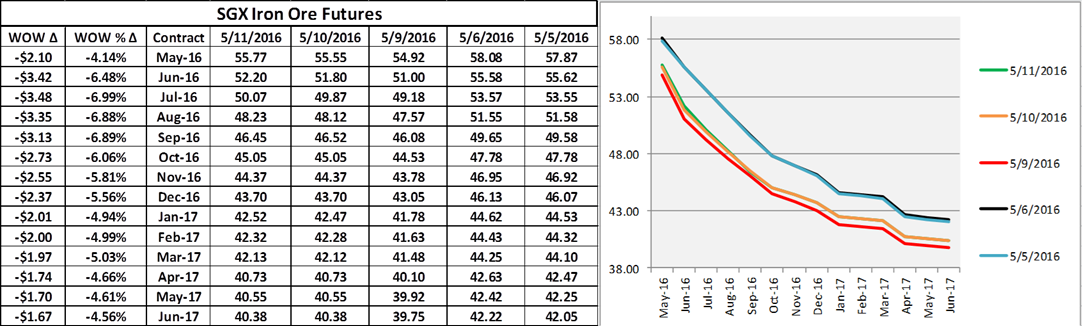

The iron ore curve remains in steep backwardation.

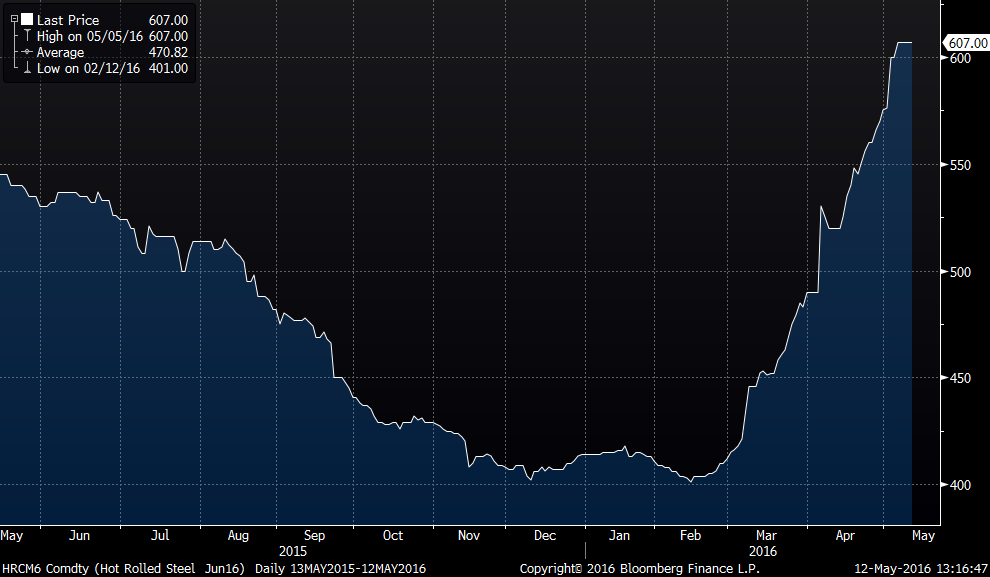

On the other hand, US Midwest HRC futures continue to rip higher.

However, the curve is increasing the steepness of its backwardation with a $20 spread between Q3 and Q4 and a $35 spread between Q3 and Q1 2017 showing the lack of confidence that prices will remain at these levels.

Futures trading volume has slowed since last week as physical prices have consolidated in the low $600s. Only 14,140 st were traded in the past five days. Current open interest is 441,260 st.

The most obvious bear case would come from China where HRC prices, raw materials and other finished steel prices have fallen dramatically from their highs over the past few weeks. While the Chinese wouldn’t be able to export tons to the US, they could have a dramatic effect on global steel prices and pressure ore and scrap prices lower. Global differentials (ie the US Midwest price vs. other countries) have expanded to excessive levels, but the limitations due to the trade cases put the market in unforeseen territory. Regardless, even if a flood of import orders were to hit the market tomorrow, it still will take months for the steel to hit the ports.

For the bull case, supply reductions by domestic mills and the sharp decline of imported tons has left producers in a very strong position. Many buyers have been slow to react to the abrupt price increase and look to be caught short steel (further perpetuating a move higher). The backwardated futures curve is telling us those attitudes persist.

Based on the mills flat rolled lead times and pricing strength, lets speculate that domestic flat rolled capacity utilization is above 90 percent if not flat out. In the past month, North Star and CSN suffered explosions limiting their production while US Steel has seen their monster No. 14 blast furnace hampered. Are these random incidents? Or does the likelihood of an accident increase with higher capacity utilization i.e. running the equipment harder? The last time we saw a number of accidents like this was in early 2014 when the mills were also running at a high utilization rate with relatively long lead times. Handicapping the probability of supply disruptions is impossible, but current market dynamics clearly have an asymmetry of risk skewed to the upside.

Next Monday brings the final DOC determination for antidumping and countervailing duties for Chinese CRC and antidumping duties for Japanese CRC. MSCI service center shipment and inventory data is also released.