Prices

December 19, 2019

Hot Rolled Futures: Steel Futures Stalling?

Written by Gaurav Chhibbar

SMU contributor Gaurav Chhibbar is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Gaurav’s previous role, he was a trader at Cargill spending time in Metal and Freight markets in Singapore before moving to the U.S. You can learn more about Metal Edge at www.metaledgepartners.com. Gaurav can be reached at gaurav@metaledgepartners.com for queries/comments/questions.

The steel markets have seen some lack of belief show up in the past few days. The best term to describe it is one that I borrow from a friend—stalling. The green line (curve as of 12/5) has pushed lower towards the orange line (12/18 curve). This recalibration of expectations is an outcome of a lower than expected pace of increases in the HRC index, as well as confusion around actual HRC lead times. As buyers of physical steel report a mix bag of availability of HRC from mills, paper traders adjusted their price targets lower. Despite positive bias to raw material pricing and weaker import pressures, the front of the curve finds it hard to break and stay above $600.

The U.S. traders are possibly still reeling from the impact of the two dead cat bounce scenarios they grappled with earlier in 2019.

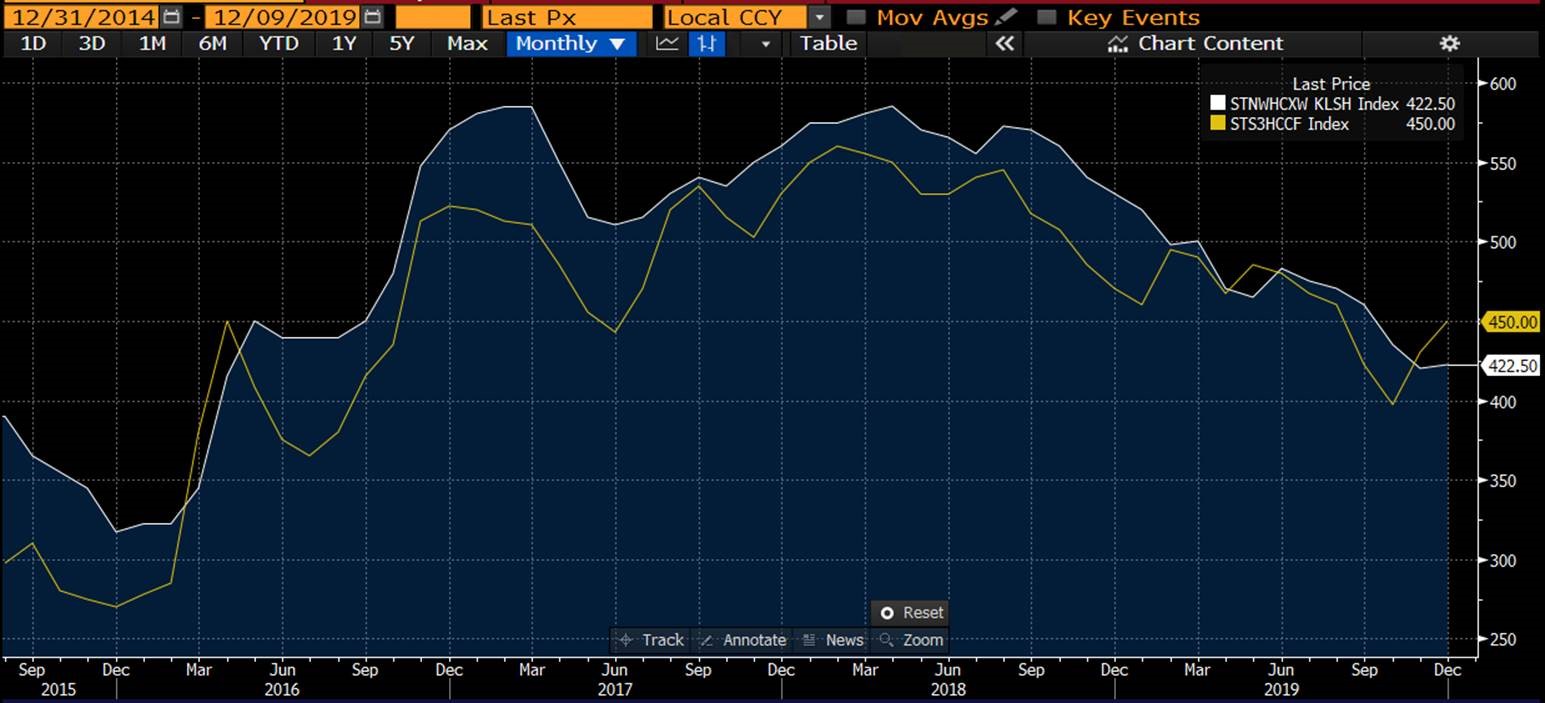

The market back in Feb/Mar and well as in Jul/Aug (timing of those short-lived uptrends) was plagued with pressure in raw materials and international (especially European) markets. If trends in Europe (chart below) were to be observed, it appears that mills in the EU are trying quite hard to push the levels higher. The southern European levels (yellow line) are up over 50 euros from their bottom levels in October.

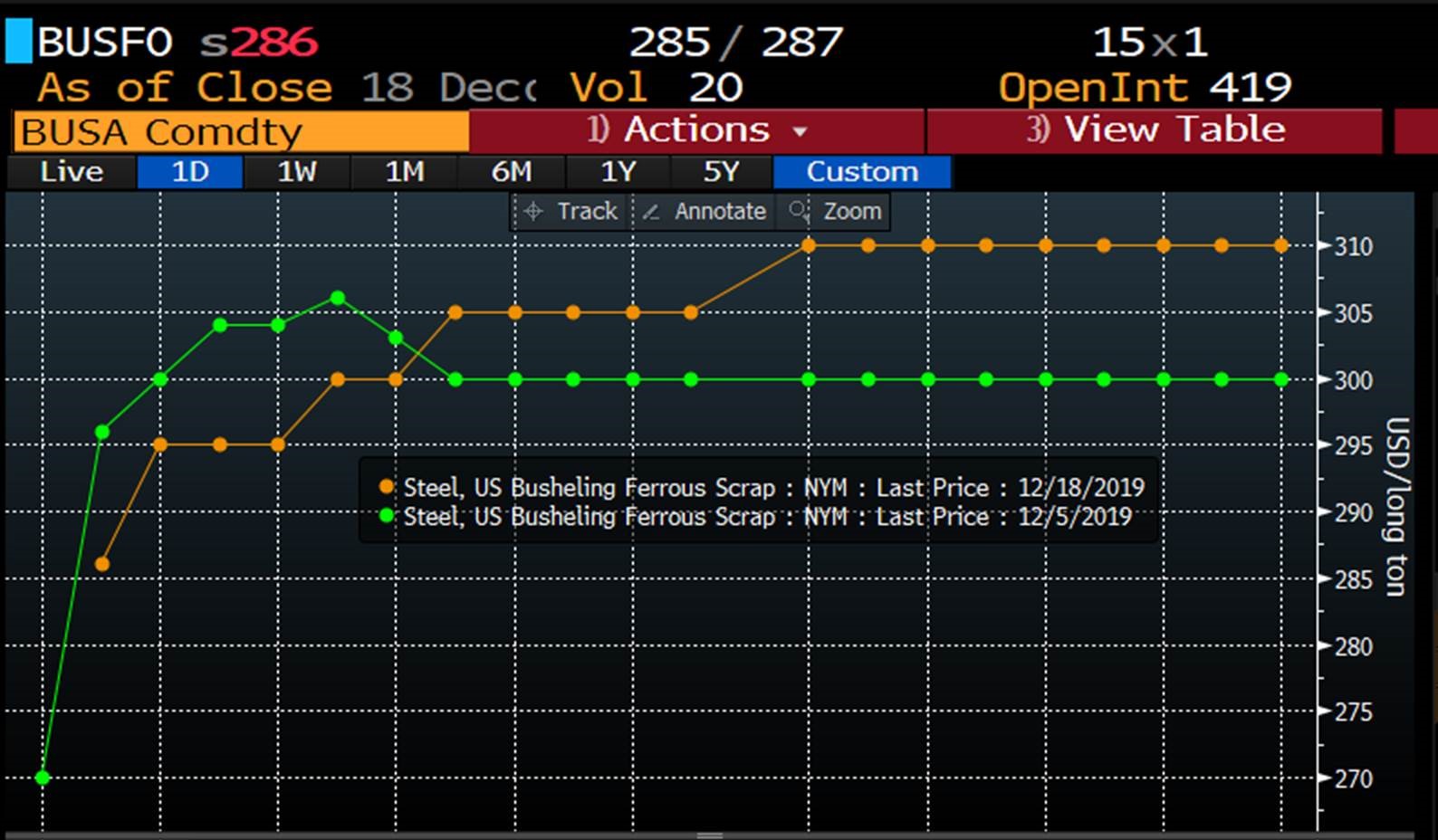

Raw materials, too, are seeing a stronger forward projection. The steeper contango is indicative of buyers’ optimism with regards to scrap pricing. This optimism is reflected in Turkish scrap prices, as well.

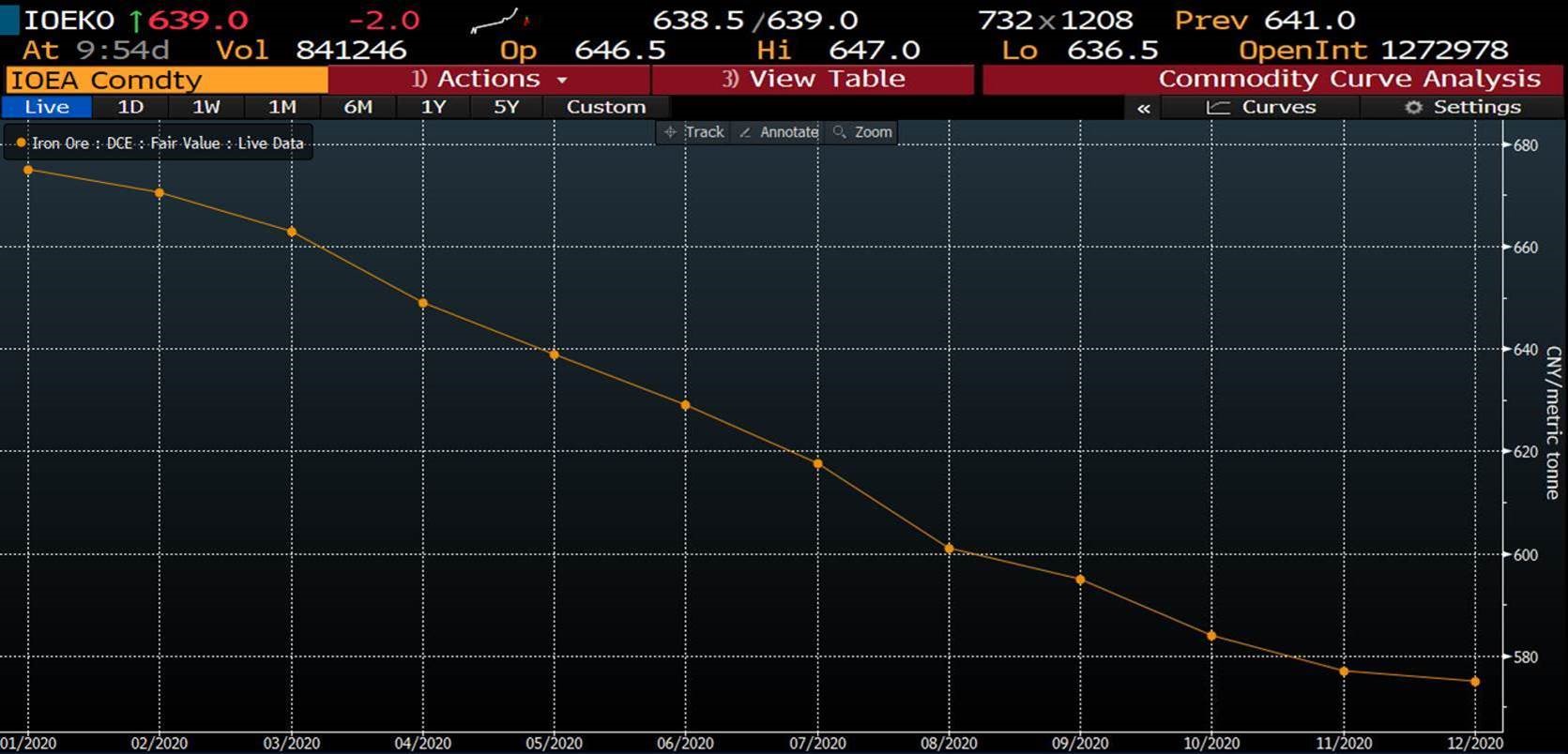

Chinese demand is being supported by government stimulus and keeping the front of the curve above $90/mt for onshore iron ore. This has resulted in a decent backwardation. The prices below are quoted in renminbi and reflect the strong price expectations for the nearby.

As we close 2019, it is quite likely that this market will remain susceptible to volatility. As the story goes, buyers sitting on low inventory levels wait for the mills to give in to their hopes of lower prices, while mills hold off on selling anything cheap in an environment of rising price levels. The resulting chaos never allows for easy supply chain management.

Good luck to you all for 2020. Happy holidays!

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information