Prices

July 21, 2022

Hot Rolled Futures: Could Everyone Please Settle Down

Written by Tim Stevenson

SMU contributor Tim Stevenson is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Tim’s previous role, he was a director at Cargill Risk Management, and prior to that he led the derivative trading efforts within the North American Cargill Metals business. You can learn more about Metal Edge at www.metaledgepartners.com. Tim can be reached at Tim@metaledgepartners.com for queries/comments/questions.

Unexpected events are always coming at us. We often have people ask us: “What is the next Black Swan event”? But the definition of a Black Swan is that they are not predictable—that’s why they call them Black Swans!

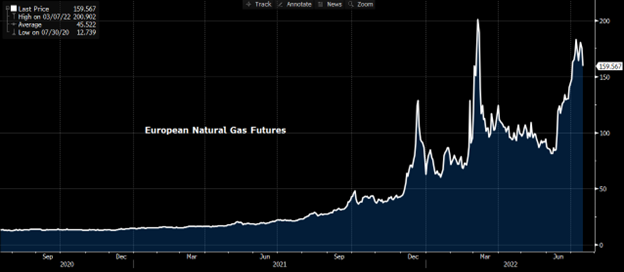

Looking at the chart below of European natural gas futures, you can see some crazy—and I do mean crazy—volatility. If you approached any major consumer of European natural gas in mid-2020 and asked them what their forecast was for gas in 2021 and 2022, they’d probably have given you some number roughly around €12–14 per megawatt hour or maybe a range of €11–15 per megawatt hour if they were expecting significant volatility.

Fast forward to 2022, and we are seeing price levels that are 10-times those prices and are causing all sorts of worries about industrial plant closures (including steel mills), and even worse, the inability to supply enough heat to homes in the coming winter.

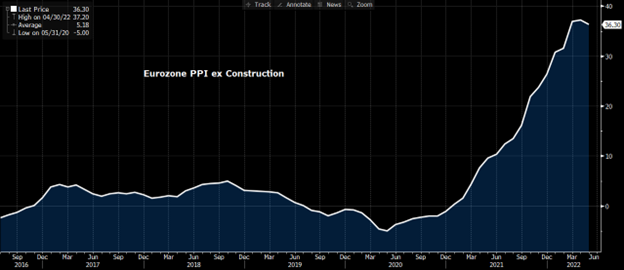

We are at unprecedented levels of volatility and price on this contract due to the unpredictability of Russian supplies. And the Russian Federation continues to play politics with its commodity flows to demonstrate the amount of leverage it has over many European countries. Imagine if you were running a company in Europe and had to deal with this kind of price inflation. The chart below displays the Eurozone Producer Price Index.

Costs are out of control and there is uncertainty as to whether they will be able to secure enough natural gas or other commodities to produce goods. We realize that we are biased towards encouraging companies to hedge their commodity exposures, but we have had many events in the past few years that have demonstrated the unpredictability of markets. Whether it was Section 232 tariffs in 2018, the Covid collapse and then massive reflation just after the worst of the pandemic, and now the Russian aggression that is wreaking havoc in commodity markets. The lesson is that most any forecast is likely to be wrong, and by using futures it does bring SOME certainty into your business in a very uncertain world.

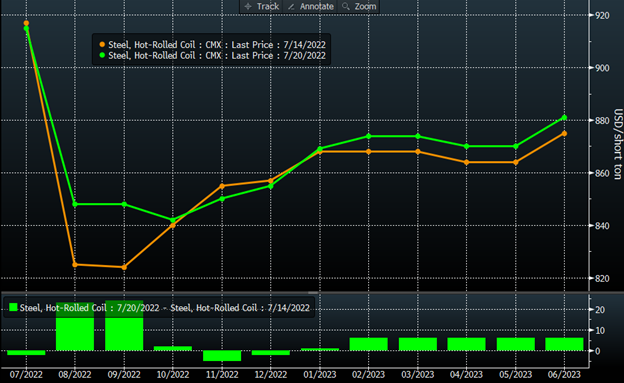

The chart below is of US HRC futures, and there really wasn’t much of a move week-on-week, but that is after a huge drop in the nearby months over the past 30 days, where prices moved down by as much as $140–160/ton in some nearby months. If you are running a service center and holding inventory, this is very painful if you are not hedged! The slight move up is interesting—perhaps some traders are speculating on a potential mill price increase.

Busheling futures (below) also haven’t moved much in the past week, but again, the fireworks really took place last month, when June busheling prices fell by more than in any month since 2008. Busheling prices have been awfully hard to predict. One would think that with auto production still lagging, supply would be impacted, and with new mills starting up, demand would be strong, but we just have not seen that play out so far.

Lastly, a word on China is worth adding. The Covid shutdowns in that country have had a negative impact on the economy and are still causing supply chain woes around the world. The government is trying to kick start the economy by announcing a huge infrastructure package ($220 billion), but to be honest, the commodity prices and inventory levels in China aren’t showing much resurgence. In the case of ore, prices have been under intense pressure:

Property markets are in disarray in China, with many home buyers boycotting their mortgages, as projects go unfinished. These mortgage boycotts have now spread to over 300 projects in 91 cities, according to Bloomberg News. While infrastructure spending will help, the property markets are not healthy, and commodity markets aren’t feeling the love from a new Chinese economic upcycle. So, with that, we will close for this week. The world and markets remain highly volatile and unpredictable, but futures markets continue to offer some help in being able to plan in uncertain times. Putin will continue to play his hand as he sees fit, and China will do what China does. While it may be illogical and unlikely, we hope that at some point, everyone just settles down a bit. Have a good weekend!

Disclaimer: The information in this write-up does not constitute “investment service”, “investment advice”, or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information.