Analysis

October 14, 2021

Final Thoughts

Written by Michael Cowden

When the books are written on a historic year for steel prices, we will probably look back at August and September as the months when things started falling apart.

Why? Because that’s when the extraordinay gaps – between U.S. steel prices and those abroad, between steel prices and scrap prices, and between market senitment and reality (as measured by lead times) – started closing.

![]() Recall that over the summer prices continued to soar upward, and consensus seemed to be not whether hot-rolled coil prices would breach $2,000 per ton ($100 per cwt) but when. The new consensus, according to SMU survey respondents, is that prices already have peaked or will peak before the year is out.

Recall that over the summer prices continued to soar upward, and consensus seemed to be not whether hot-rolled coil prices would breach $2,000 per ton ($100 per cwt) but when. The new consensus, according to SMU survey respondents, is that prices already have peaked or will peak before the year is out.

SMU’s average hot-rolled coil price was at $1,920 per ton when I filed this column, down $35 per ton from a month earlier.

The declines started in September, which saw prices hit a new record of $1,955 per ton and then fall for three consecutive weeks – the first time that had happened since the market buckled under the weight of the pandemic in the spring and summer of 2020.

I don’t want to toot SMU’s horn too much. But we called this one back in August. (Check out Final Thoughts on Aug. 20.) Prices were still moving higher then. But the writing was on the wall.

The gaps mentioned above had to close. Because such unprecedented spreads could not hold unless a new precedent was established – and to date, one hasn’t been.

Let’s take the gaps in order. First, imports.

The U.S.-Import Price Gap

The spread between import prices – notably EU HRC prices – and domestic HRC prices had reached its widest point ever by the end of September. And now the spread has continued to balloon into October.

That initially enticed people near coastal areas, where imports are always a bigger part of the mix. Transportation is expensive and ports congested. But with discounts of hundreds of dollars per ton, many buyers calculated that gap between foreign and domestic prices made imports worth the risk.

And it wasn’t just coastal buyers. We’ve contacted people in the Ohio Valley more recently who were buying foreign material, shipping it upriver and still seeing significantly lower prices on a delivered basis compared with what domestic mills were offering on fob terms.

I wrote in a prior Final Thoughts the U.S. has been importing at least a steel mill’s worth of extra production every month. That was too conservative.

Let’s assume a sheet mill with annual capacity of 3 million tons per year – or 250,000 tons per month. Flat rolled imports have totaled one million short tons or more every month since May, according to Commerce Department figures. And in August, they were closer to 1.3 million tons. That’s about 500,000 tons – or two mills – more than the monthly average of approximately 800,000 tons over the last two years.

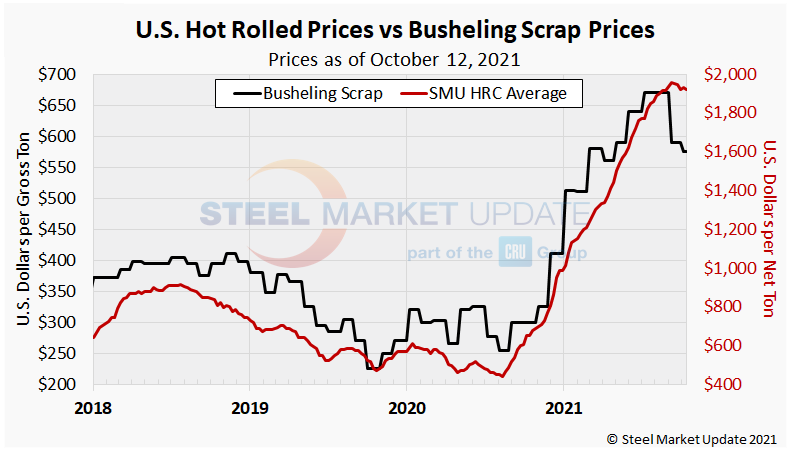

The Steel-Scrap Gap

Another gap that needs to close is the one between hot-rolled coil and busheling scrap. I’ve in previous articles displayed a chart from SMU’s interactive pricing tool.

Here is another way to look at it:

The red line is HRC prices, and the black line is busheling scrap prices.

I know some market participants have said that the correlation between scrap and coil has broken down. But that’s actually not been the case, not even during this historic price runup. Until more recently, that is, when you can see that scrap and coil are clearly out of whack.

And that gap will close. How can we be sure? Because we’ve seen this movie before.

Think back to the second quarter of 2018, when Section 232 tariffs were unexpectedly rolled out not only on U.S. adversaries but also on trading partners and allies like Canada, Mexico and the EU. Steel prices shot upward even as scrap prices stayed comparatively steady. But steel prices fell in 2019 when tariffs were removed from Canada and Mexico.

It now appears likely that Section 232 tariffs on the EU will be replaced with a tariff rate quota (TRQ) – a mechanism under which imports below a certain volume would not face tariffs. A TRQ would have an impact given the price differential between EU and U.S. HRC mentioned above.

Domestic mills have talked a lot about discipline over the last year. But discipline is easy when the market is going up. It will be tested as prices move lower.

U.S. mills might undercut one another to attract business. Or they might try to undercut imports. U.S. EAFs are very low cost – and some EAF steelmakers have explicitly stated that their new capacity is intended to displace imports. They will be able to do that – but only if they become price competitive with foreign steel and if they narrow the steel-scrap gap.

The Lead Times-Sentiment Gap

Another gap that seems unsustainable is the one between lead times and market sentiment.

Lead times are typically an advance indicator of pricing direction. When lead times are stretching out, it typically means prices are going up or soon will. The opposite is also true. When lead times are getting shorter, it typically means prices are falling or soon will.

And lead times have been getting shorter for months now. Our latest survey data is no exception to that rule.

In contrast, SMU’s Steel Buyers Sentiment Index – a measurement how North American flat-rolled steel market participants feel about their companies’ prospects – has been at or near record highs even as steel prices and lead times have fallen. Sentiment last dropped into pessimistic territory following the COVID-19 outbreak. It has been solidly optimistic ever since.

It’s unusual to see record high sentiment and shorter lead times. The two indicators typically trend together. But I’m hoping this particular gap doesn’t close.

The spreads between domestic prices and import prices need to close for the U.S. steel market to remain competitive. And that necessarily implies a narrower spread between steel and scrap prices.

What I’m hoping is that the strong readings we’ve had on sentiment mean that demand, unlike price, is still on stable footing and will remain so even as prices normalize.

Momentum

In the meantime, keep an eye on our price momentum indicators. They will have to adjust downward If the gaps discussed above close.

The last time our sheet momentum indicator was lower was on July 21, 2020. And the last time our plate momentum indicator was lower was on May 12, 2020.

That was following the outbreak of the COVID-19 pandemic. They have been neutral or up ever since. But nothing is forever in a cyclical market like steel, not this historic price upswing and not the momentum it has created.

In Memoriam

Doug Bernd, recently retired Senior Vice President of Purchasing for Steel Technologies, died from a heart attack on Tuesday. He was 70 years old. Doug and John Packard worked together at Pacesetter Steel early in their careers. Doug and John were part of the dynamic sales team at Pacesetter Steel back in the 1980s. He and John worked closely together for a number of years and remained friends as they both pursued their steel careers at other companies. John related to us that Doug was one of the best golfers he ever knew (also one of the best dressed), and that he was with John in Jamaica for what became one of John’s personal favorite golf stories of all time. (You will have to call John and ask him for the details.) Doug Bernd was an honest, honorable, decent gentleman and he will be sorely missed.

By Michael Cowden, Michael@SteelMarketUpdate.com