Prices

June 9, 2022

Hot Rolled Futures: You May Be Wrong, You May Be Right

Editor’s note: SMU contributor Bryan Tice is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and the firm design and execute risk management strategies for clients along with providing process and analytical support. Prior to Metal Edge Partners, Bryan held a variety of commercial leadership roles involving purchasing, sales, and risk management for Feralloy Corporation, Cargill Steel Service Centers, and Plateplus Inc. You can learn more about Metal Edge at www.metaledgepartners.com. Bryan can be reached at Bryan@MetalEdgePartners.com for queries/comments/questions.

As I was driving into the office this morning, the Billy Joel song from the Glass Houses album “You May Be Right” played on the radio, and I chuckled to myself that the chorus so perfectly defines the dilemma of the steel price “forecaster”. For those born after 1978 who don’t know who Billy Joel is or this specific song, it opens with the sound of breaking glass. And shortly thereafter Joel breaks into a chorus that goes, “You may be wrong for all I know, but you may be right.” Seemed like a good analogy for the steel/futures market.

It’s been a while since I last contributed an article to SMU (March 17th to be exact), but I have enjoyed the futures articles and the perspectives of my colleagues and peers who’ve contributed weekly since then. We have clearly seen an epic rally and meltdown in steel prices that has been well documented. Given my last article was 3-4 weeks into the Ukraine/Russian conflict, it makes total sense why the market has changed so markedly since I last contributed.

I appreciate those who publish forecasts, whether they are for steel prices, oil prices, or equity prices. The issue with forecasts is that they are predicting a future outcome at that specific moment of time. As time progresses and more information becomes available, those forecasts (if done responsibly) should be adjusted or revised to reflect new information and expected outcomes. The downside to forecasting is that it often lives in a vacuum in the eye of the beholder, beyond the period it was developed. I would guess that many of you reading this article may have placed a wager back in February 2022 on where the steel price would be at the end of first quarter. Those of you who forecasted a $950 per ton HRC price begrudgingly paid their $20 to the office pool and likely lost out to the “contrarian” who suggested HRC would be $1,200 per ton. Did the contrarian have better insight, or was it just luck?

Despite rampant inflation in the economy, it is hard to find many contrarians now predicting a steel pricing upswing. Global prices continue to grind lower. European prices continue to decline, though some have suggested we are quickly approaching the cost of production that could lead to further output cuts. China could begin producing/consuming at a higher rate, providing some support for raw materials and finding a floor on steel pricing. In the US, we continue to hear that big buyers’ expectations are for three-digit HRC and that we may also challenge the cost of production, especially during the ramp up of new domestic flat rolled capacity.

You may be right.

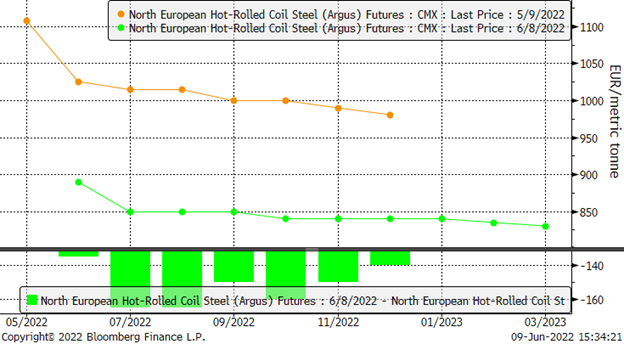

European HRC Futures Prices

European futures have moved down €150/t month over month in the July-November ’22 timeframe and now reflect a very flat forward curve in around the €850/t range in the second half of ’22 through q1 ’23.

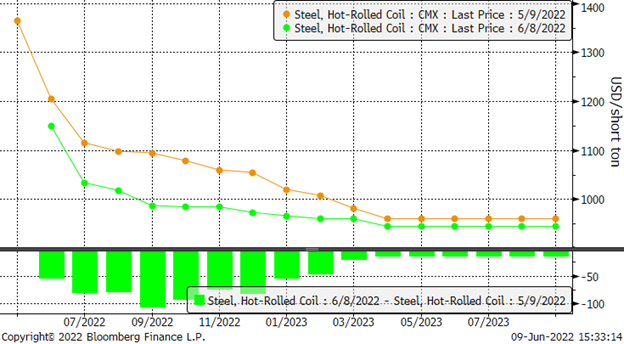

US HRC Futures

US futures have also experienced a meaningful downward correction into Q1 ’23 as compared to the early May timeframe, with prices into 2023 averaging in the mid $900s per ton.

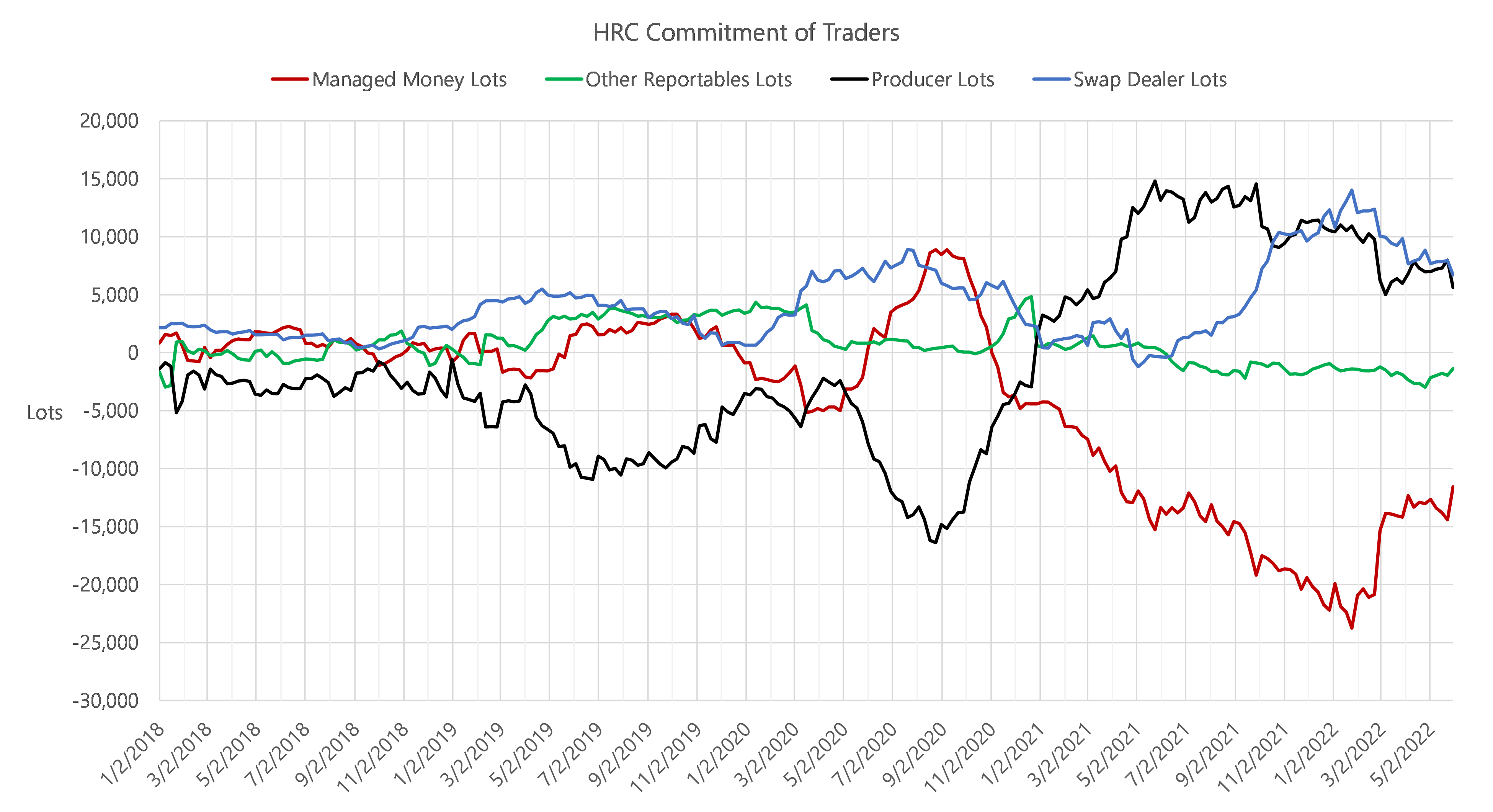

Commitment of Traders Report

The chart above shows how managed money (red line) has been reducing their HRC short positions, although most of the short covering occurred as the war in Ukraine sent prices spiking. Producers (black line) and swap dealers have also been gradually reducing their long positions. Each group remains modestly long or short, so one must wonder if we are approaching a period where we’re waiting to see whether either side blinks. Either managed money starts taking profits, or producers/swap dealers scramble to get into short position to protect against further downside pricing moves and changes the momentum of the forward curve.

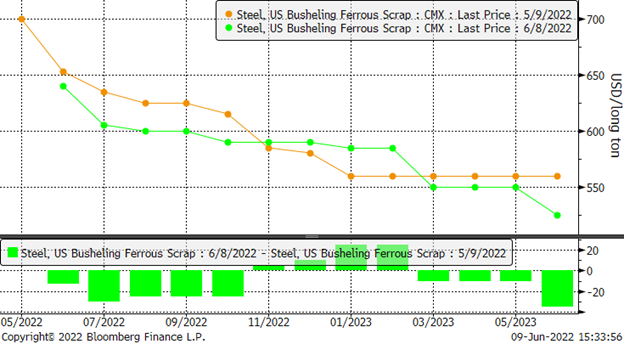

Busheling Scrap Futures

Scrap prices continue to retreat from their post-war highs, and we’ve heard some suggest scrap prices may flatten in July. The above forward curve has moved lower month on month through early Q4 ’22, with slightly higher scrap prices expected in the Nov22-Feb23 timeframe. HMS prices are now $20 per gross ton lower than they were in November 2021, yet busheling prices are $130/gt higher than that same period. Much has been written about the elevated spreads between grades of scrap and the new EAF mills’ appetite for scrap. This month, we have begun to see those spreads narrow from the $245/gt peak in April/May to $220/gt in June. Given the mix shift of EAF mills to try and blend more lower grade scrap into their melt, it seems plausible that HMS grades may have found a floor but busheling scrap may still have some room to the downside to get those spreads back in historical ranges – although iron ore remained mostly stable throughout China’s Covid lockdowns. Most look to the busheling prices as a clue to the cost impact for flat rolled suppliers and thus sheet pricing, so we will continue to keep a close eye on the scrap side and on these spreads.

Coming full circle back to the Billy Joel song reference “you may be wrong for all I know, but you be right,” one step you can take to provide some certainty in uncertain times is to utilize risk management tools to take a few variables off the table. That could be to lock in a steel cost or margin for some period in the future, or it could be protecting your company from a portion of the inventory writedowns you may be experiencing now.

Have a great rest of your week and thanks for reading.

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice,” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information.