Plate

August 11, 2022

Plate Market Report: Prices Slip Again, Direction Still Not Clear

Written by David Schollaert

US plate prices edged down again this week after seeing their largest decline in nearly five years the week prior.

The latest declines are not exactly a surprise given plate prices had been holding an unsustainable premium over coil and buying has been largely hand-to-mouth. But the straw that broke the camel’s back might just be Nucor’s announced plate price decrease last week.

Sources told Steel Market Update this week that further price softening is imminent and mills have started to negotiate when it comes to October shipments. But there’s still a major impasse, as demand is still steady and there are no signs pointing to improved demand for the remainder of the year.

“We are seeing some softening on plate pricing,” said a buyer. “Right now, it’s around $78–80/cwt for Q4… we’re pressing hard to try and get it down further.”

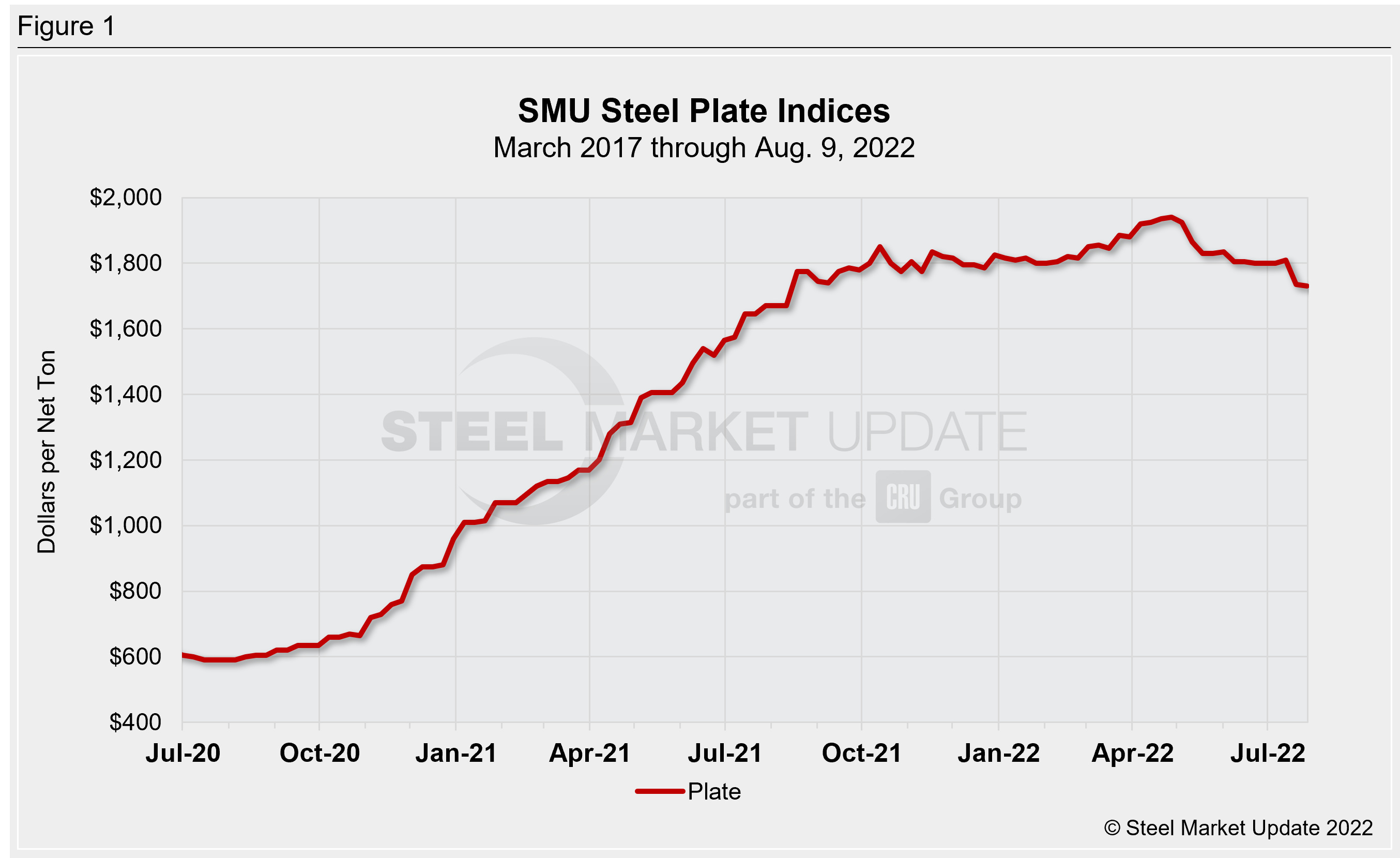

SMU’s most recent check of the market on Aug. 9 places plate prices between $1,700–1,760 per net ton ($85-88/cwt) with an average of $1,730 per ton ($86.5/cwt) FOB mill, according to our interactive pricing tool (Figure 1).

With buying patterns still largely limited to gap-filling and project-specific needs, there are others that anticipate plate price declines to be sparse and unlikely to mirror the fall seen across the rest of the sheet market.

“The premium over coil is too high to sustain but I am still amazed how resilient plate prices are,” another source said. “There’s not a whole lot going on though, so it wouldn’t surprise me if prices held here for a bit.”

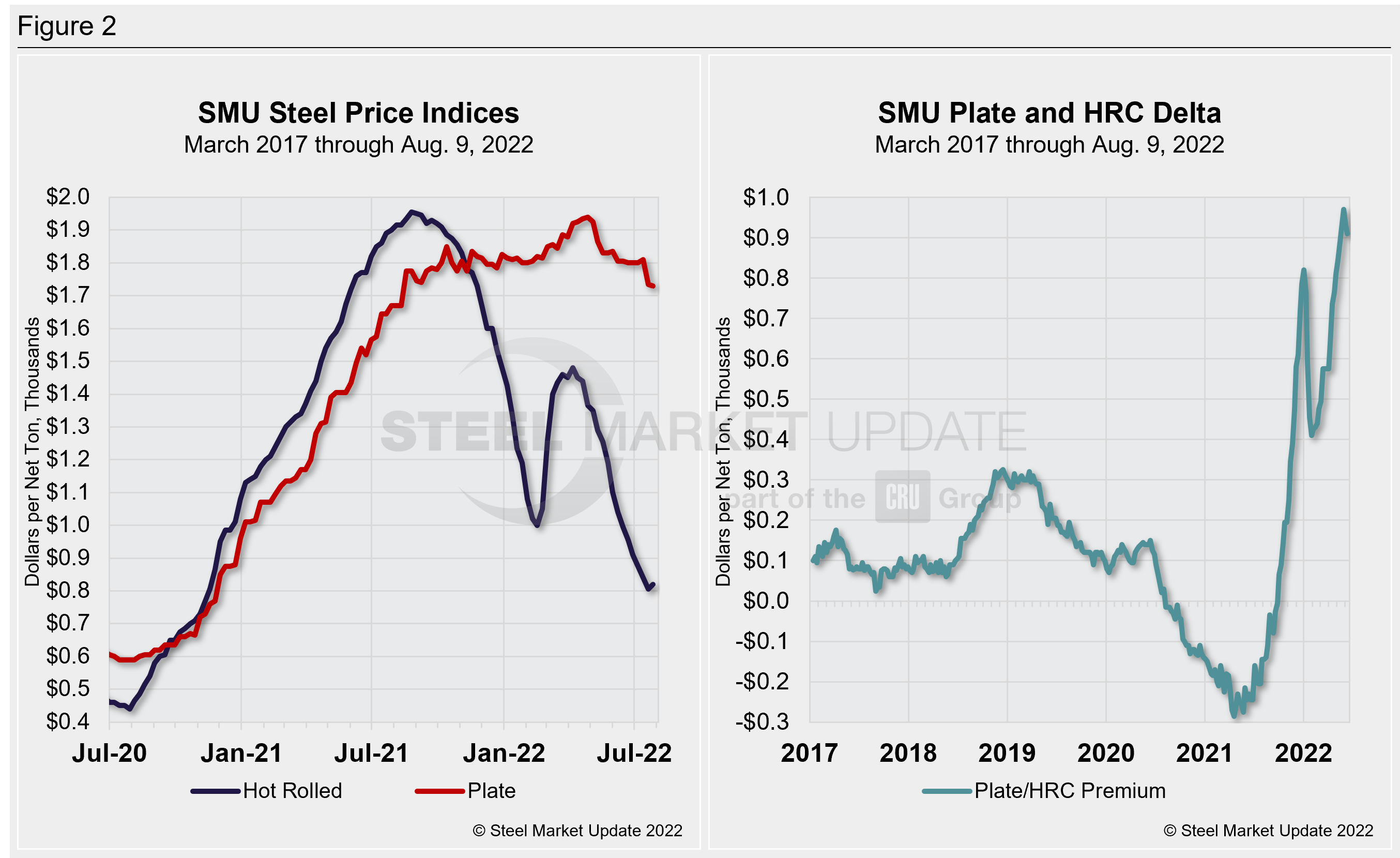

That trend has been evident for much of this year. Plate prices, unlike sheet prices, have been relatively stable year-to-date, despite massive swings in sheet prices before and since Russia’s war in Ukraine began.

This week’s decline was well short of the roughly 4% decline prices saw after Nucor’s plate announcement two weeks ago. And if you are watching the delta between plate and hot band, there’s still a long way to go regardless of how resilient plate prices have been.

Plate prices remain more than double hot-rolled coil prices. And while sheet and plate markets have different underlying dynamics, the delta between the two is not likely sustainable. But if plate prices won’t fall, could the delta shrink simply because HRC prices begin to rebound?

We saw Nucor announce a sheet price hike on Monday, potentially to set a price floor. There was a slight shift higher in HRC prices, the first of its kind since early Q2. But it’s too early to say if it’s the start of a trend or whether it will stick, but Nucor’s $50 per ton certainly caught everyone’s eye.

SMU’s HRC price inched up this week to an average of $820 per ton ($41/cwt), FOB mill. The move was a 1.9% gain over the week prior.

If the delta remains at such historic levels, more imports could find their way to US ports.

Foreign plate with November arrival is priced between $1,620–1,660 per ton ($81–84/cwt). According to SMU sources, offers for South Korean plate with November ship dates are $1,480 per ton ($74/cwt), DDP Los Angeles area ports, and Q1 2023 arrival offers should be out next month.

“The market is still pretty good because inventories are so low,” said a source. “Import volumes could inch up, but I figure that would only really impact the West Coast.”

The bulk of plate transactions were at the mid-point of SMU’s range, in line with published and ‘unofficial’ prices from the three major US mills. But with sources noting that some mills are starting to negotiate, further erosion could be in the cards.

Cut-to-length and discrete plate lead times are running between 4–7 weeks. But in many cases, material is arriving closer to 3–4 weeks. This is another indicator that fundamental steel plate demand is slowing down.

The market consensus remains that plate prices could make another correction this month, though probably not as large as the last reduction.

By David Schollaert, David@SteelMarketUpdate.com