Prices

November 17, 2022

HR Futures: Shifting Expectations in Forward Curve Prices

Written by Jack Marshall

The following article on the hot-rolled coil (HRC), scrap and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Hot Rolled

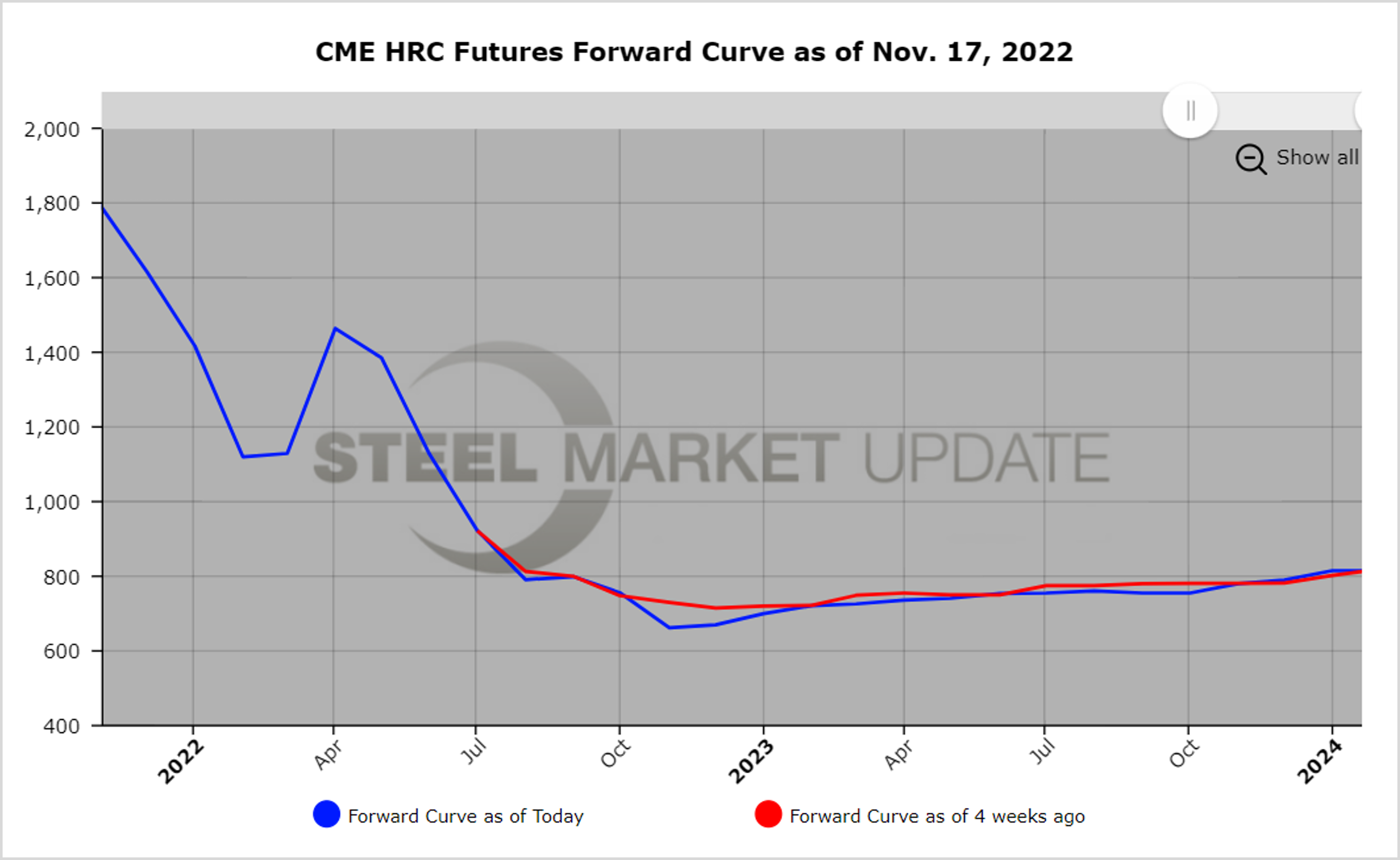

The indicated value of HR spot has declined roughly $31 per short ton ($687/ST to $656/ST) this month. For comparison purposes, in October over the same three Wednesday period the value of HR declined by $8/ST ($769 to $761).

Both months saw spot HR fall but at different rates. In contrast, the forward values in the October period declined for the Cal’23 average price by about $31.5/ST versus the values in November period, which have increased for the Cal’23 average price by $28/ST.

Interestingly, even as participants expect the spot to continue to move lower in the near term, they have buoyed the forward curve in Cal’23. The first half of 2023 months are up an average of $40/ST over the last three Wednesdays. Open interest rose to approximately 25,100 lots in October and is about 700 lots shy so far this month. Not only has the forward curve shifted higher but the contango in Cal’23 is steeper:

• October example: the Jan’23 to Dec’23 +$61/ST (720/781)

• November example: the Jan’23 to Dec’23 +96/ST (704/800).

The shift in the forward curve is noteworthy given recent modest trading volumes from the hedgers of physical transactions. The latest chatter highlights how the current opaque nature of demand is limiting transactions as the futures forecast horizons are getting shorter.

Below is a graph showing the history of the CME Group HR futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

Scrap

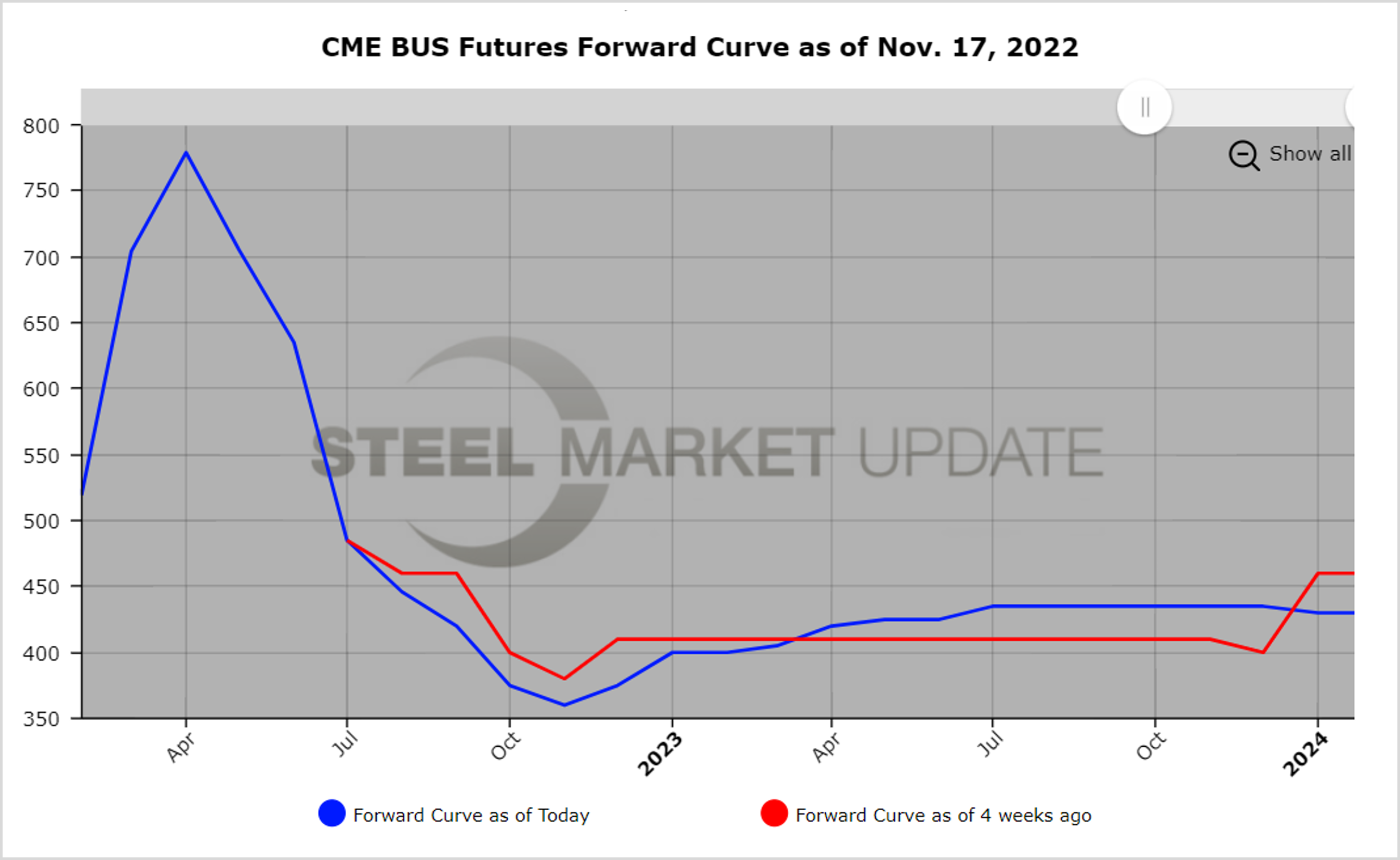

Regional differences have muddied the picture around expectations for BUS going forward. Pig iron price increases with simultaneous price drops in export scrap, along with decreasing production and the onset of winter weather, will keep forecasters busy.

Strong volume and a pickup in BUS open interest have focused a lot of attention on scrap. Open interest hit about 180,000 GT, marking a new record since our last publication. Recent transactions in Cal’23 BUS months have helped push up the average price of futures BUS by about $15/GT on average. (Cal’23 average value $420/GT). The latest Q1’23 BUS market sits around $400/GT.

Markets are waiting to see if the Dec’22 BUS settle will break the downward price trend. Will the new year changeover and scrap cycle offset the continuing decline in mill capacity utilization?

Metal margins in the 1H’23 have moved higher this month, with Q1’23 increasing from $280/ton to $317/ton (+$37/ton) and Q2’23 increasing from $301/ton to $328/ton (+$27/ton).

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here.

By Jack Marshall of Crunch Risk LLC